On the radar

- S&P affirmed Romania’s ratting and sustained negative outlook.

- Today, Romania’s central bank hold a rate setting meeting and no change is expected.

- In Czechia at 9 AM CET inflation in March, retail sales growth in February and trade balance will be released.

- At noon CET Serbia releases producer prices.

Economic developments

Today we take a closer look at the recent dynamics in the CEE8 Consumer Confidence and Economic Sentiment indicators, both of which have shown signs of stabilization rather than renewed acceleration in early 2026. The latest reading of the regional Economic Sentiment Indicator (ESI) shows only a marginal downtick in March, slipping to 97.7 from 97.8 in February. While the decline is modest, it reinforces the view that sentiment has broadly plateaued. In contrast, consumer confidence weakened more noticeably in March and the upward trajectory has flattened out. Households across the region continue to face elevated uncertainty, stemming from price dynamics driven mostly by global risk factors. Higher uncertainty translates into restrained willingness to increase discretionary spending, even as real wage growth remains positive in most CEE countries. Moreover, consumers still have not fully recovered from inflation shock in 2022 and 2023. All in all, the transition back to the sentiment levels of the pre war, pre inflation shock era remains incomplete and increasingly dependent on global rather than local developments.

Market movements

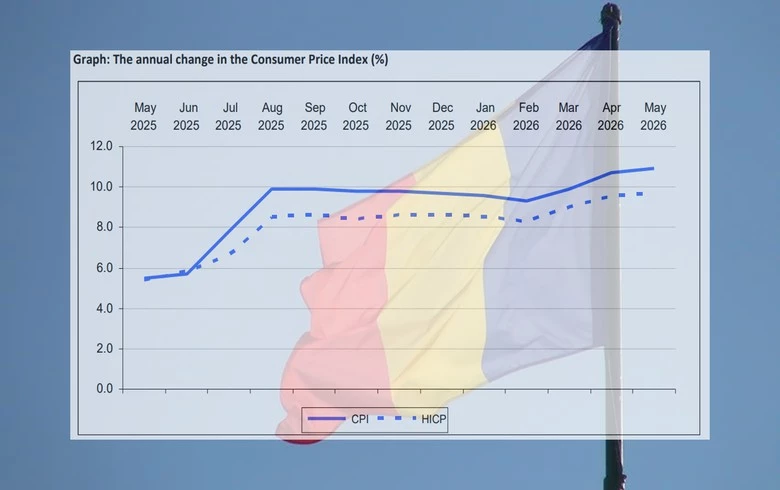

As Romania’s four-party coalition government is continuing to take steps to consolidate large budgetary deficits–via tax hikes and wage and pension freezes, S&P did not change Romania’s rating but sustained negative outlook. Today, Romania’s central bank holds a rate setting meeting. The central bank is caught between global inflationary forces and domestic disinflationary trends. While key rate is broadly expected to remain on hold, heightened external uncertainty should prompt a hawkish tone. Except for the mention of an upward inflation forecast revision, the press release is unlikely to offer additional forward guidance. This week, there are two other central banks’ meetings in the region (Poland and Serbia) and stability of rates is also broadly expected. Over last week, long term yields have declined in all CEE countries. On the FX market, we have seen appreciation of the Hungarian forint that we mostly associated with the expectations on the outcome of upcoming Parliamentary elections that will be held during upcoming weekend (April 12).