As Asian markets navigate the complexities of energy market volatility and geopolitical tensions, investors are increasingly focused on companies that demonstrate resilience and potential for growth. In this context, stocks with high insider ownership can be particularly appealing, as they often indicate strong confidence from those closest to the company’s operations.

We’ll examine a selection from our screener results.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Foosung Co., Ltd., along with its subsidiaries, manufactures and sells chemical products for various industries including automotive, iron and steel, semiconductor, construction, and environmental sectors in South Korea, with a market cap of ₩1.06 trillion.

Operations: Foosung Co., Ltd. generates revenue through its production and distribution of chemical products across diverse sectors such as automotive, iron and steel, semiconductor, construction, and environmental industries in South Korea.

Insider Ownership: 32.9%

Revenue Growth Forecast: 18.6% p.a.

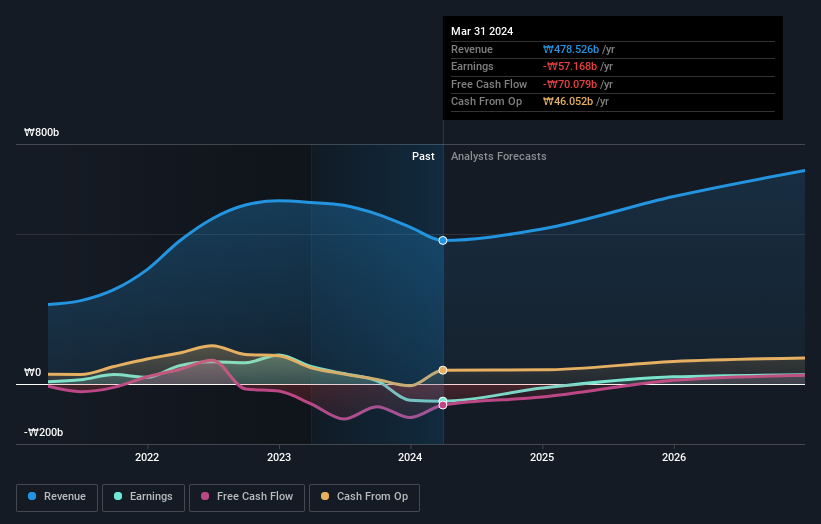

Foosung Co., Ltd. has demonstrated a remarkable turnaround with a net income of KRW 5.31 billion for 2025, compared to a significant loss the previous year. Despite high share price volatility and interest payments not being well covered by earnings, its forecasted annual profit growth of 78.6% surpasses the Korean market average, indicating strong growth potential. However, insider trading activity has been minimal over recent months, suggesting cautious investor sentiment internally.

KOSE:A093370 Earnings and Revenue Growth as at Apr 2026

Simply Wall St Growth Rating: ★★★★★☆

Overview: Jiangsu Sidike New Materials Science & Technology Co., Ltd. (SZSE:300806) specializes in the production and development of advanced polymer materials, with a market cap of approximately CN¥20.68 billion.

Operations: Jiangsu Sidike New Materials Science & Technology Co., Ltd. focuses on producing and developing advanced polymer materials, with a market cap of around CN¥20.68 billion.

Insider Ownership: 38.1%

Revenue Growth Forecast: 29.1% p.a.

Jiangsu Sidike New Materials Science & Technology is experiencing robust growth, with earnings rising by 81.9% over the past year and forecasted annual profit growth of 74.3%, outpacing the Chinese market average. Revenue is projected to increase at 29.1% annually, exceeding both market expectations and a 20% benchmark. However, its financial position shows interest payments aren’t well covered by earnings, and recent insider trading activity has been minimal amidst share price volatility.

SZSE:300806 Ownership Breakdown as at Apr 2026

Simply Wall St Growth Rating: ★★★★★☆

Overview: Micronics Japan Co., Ltd. develops, manufactures, and sells body measuring equipment as well as semiconductor and liquid crystal display inspection equipment globally, with a market cap of ¥411.68 billion.

Operations: Micronics Japan’s revenue is primarily derived from its global operations in body measuring equipment and semiconductor and liquid crystal display inspection equipment.

Insider Ownership: 15.3%

Revenue Growth Forecast: 14.6% p.a.

Micronics Japan is experiencing significant earnings growth, forecasted at 21.1% annually, surpassing the Japanese market average of 9.9%. Despite a volatile share price recently, the company’s Return on Equity is expected to reach 24.7% in three years. Recent financial results show net income of ¥12.06 billion for 2025 and an increased dividend proposal from ¥70 to ¥95 per share, pending approval at their upcoming Annual General Meeting on March 26, 2026.

TSE:6871 Earnings and Revenue Growth as at Apr 2026

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include KOSE:A093370 SZSE:300806 and TSE:6871.