What happened?

Markets turned more volatile in the first quarter of 2026.

Earlier last month, we discussed what we would be doing with our portfolios with this Middle East conflict.

Higher oil prices, renewed inflation concerns and uncertainty around interest rates created a more uneven backdrop for Singapore equities.

Despite the broader market weakness, there were still pockets of strength. We found three Singapore blue chip stocks that gained more than 8% in March.

Beyond the blue chips, several iEdge Singapore Next 50 Index constituents also rallied, with some gaining more than 30% in the first quarter.

In this article, we take a closer look at the five best-performing iEdge Singapore Next 50 stocks in 1Q26, what may have driven the move, whether their dividend yields remain attractive, and if there could still be room for further upside.

#1 – Frencken Group (SGX: E28)

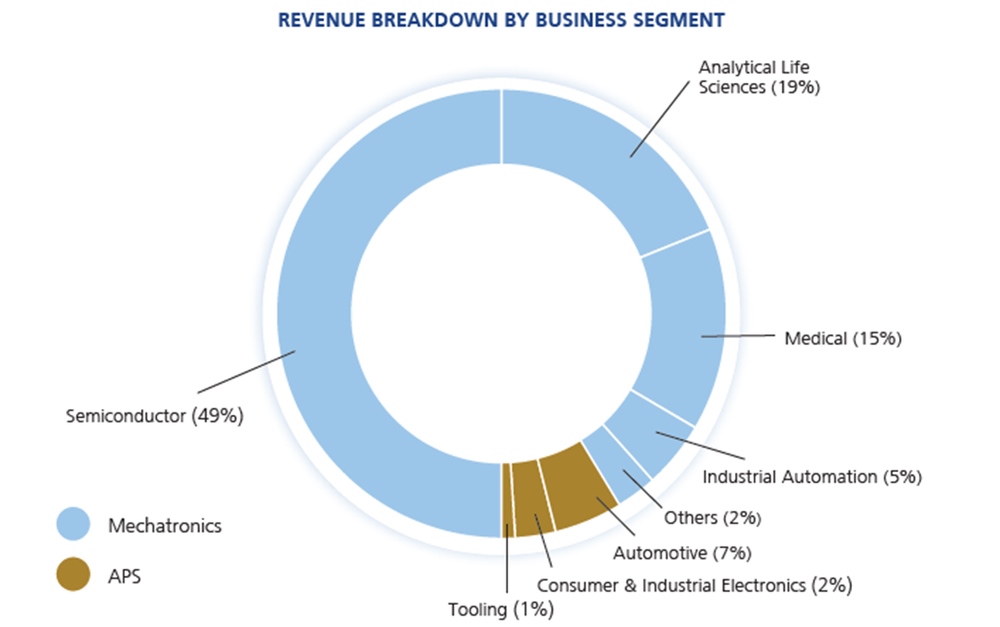

Frencken Group is a global technology solutions company that provides design, manufacturing and engineering services to multinational customers across semiconductor, medical, analytical life sciences, automotive and industrial segments.

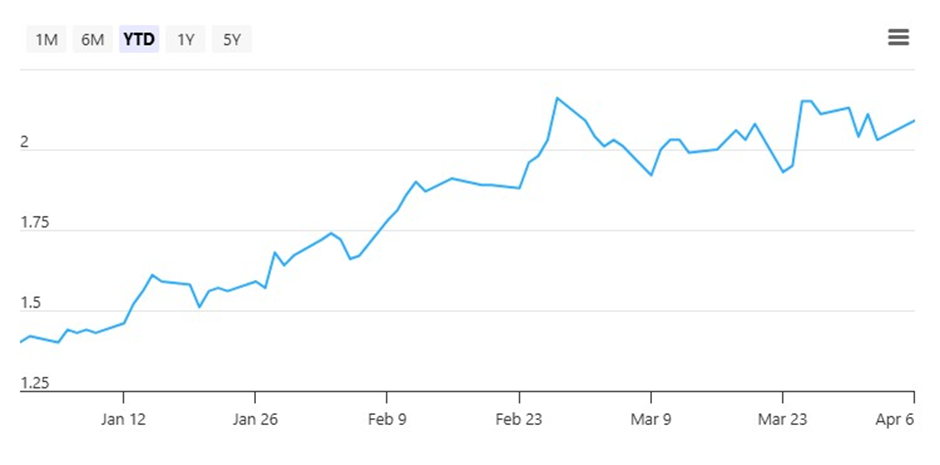

Frencken Group was the best-performing Next 50 stock in the quarter, with a total return of 47.8% from 31 December 2025 to 31 March 2026.

The rally was driven by stronger confidence in the semiconductor recovery, with investors seeing Frencken as a way to gain exposure without relying on just one end market.

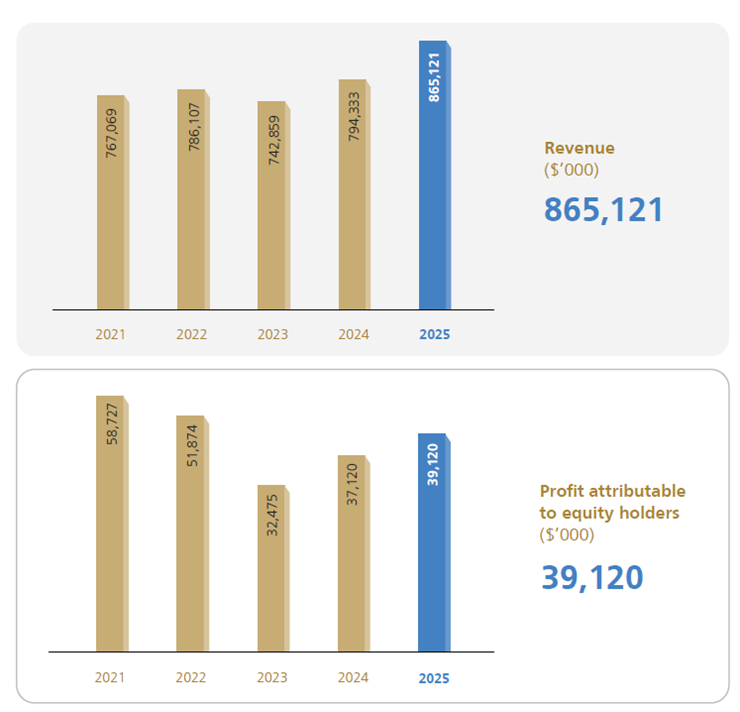

Sentiment improved further after the company reported FY2025 results in late February, helped by margins that came in ahead of expectations.

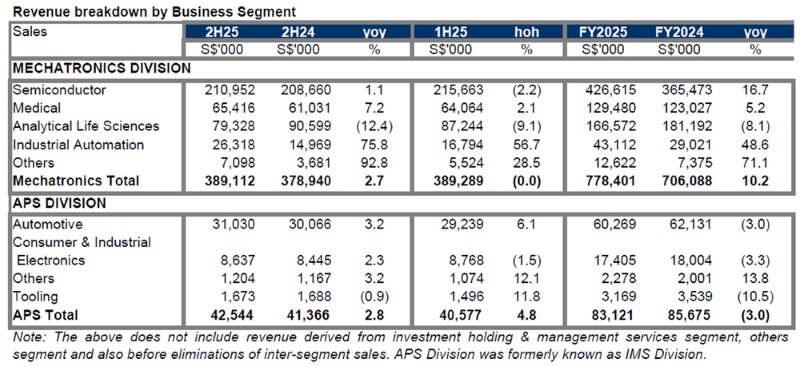

The main driver was the Mechatronics division, where semiconductor revenue grew 16.7% to S$426.6 million and industrial automation revenue jumped 48.6% to S$43.1 million.

One softer area was analytical life sciences, where revenue fell 8.1% due to slower orders from European customers and lower US research funding.

Looking ahead, management remains positive on FY2026.

It expects continued recovery in Asia, a possible rebound in European semiconductor orders, and contributions from ongoing capacity expansion projects, including a new US facility, a new Singapore facility targeted for completion in the first quarter of 2027, and added production space in Malaysia.

The successful delivery of a complex semiconductor equipment prototype for a leading European customer also suggests Frencken is moving further into higher-value work.

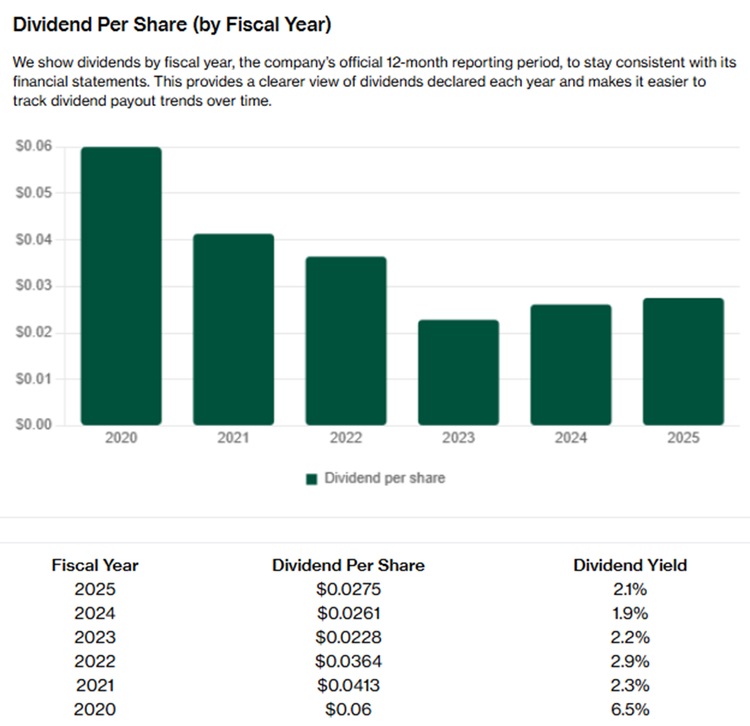

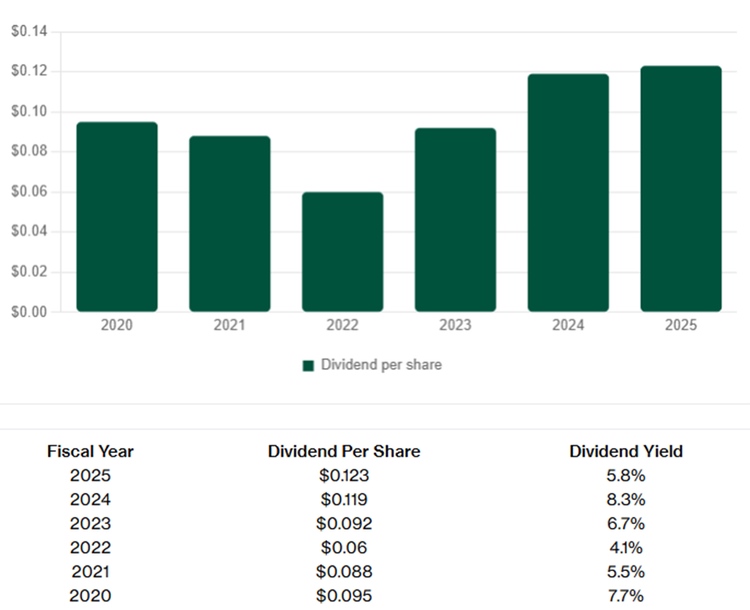

On dividends, Frencken proposed a final dividend of 2.75 cents per share for FY2025, up from 2.61 cents a year ago.

Based on its 31 March 2026 share price of S$2.04, that works out to a trailing yield of about 1.3%.

Consensus is forecasting a dividend per share of S$0.031 for 2026, translating to a forward dividend yield of 1.5%. Based on the consensus target price of S$2.41, this also implies around 18% upside.

Frencken has consistently paid out at least 30% of annual earnings since listing, and it ended FY2025 with net cash of S$139.6 million.

Overall, Frencken stands out for its move into higher-value semiconductor equipment work. Together with its capacity expansion across Singapore, Malaysia and the US, this could position it as a second-order beneficiary of AI-related demand.

Related links:

#2 – First Resources (SGX: EB5)

First Resources is one of the leading palm oil producers in the region, with more than 270,000 hectares of oil palm plantations across Indonesia.

Beyond plantations and palm oil mills, it also has downstream refining, biodiesel and kernel crushing operations, which allow it to capture more value across the palm oil chain.

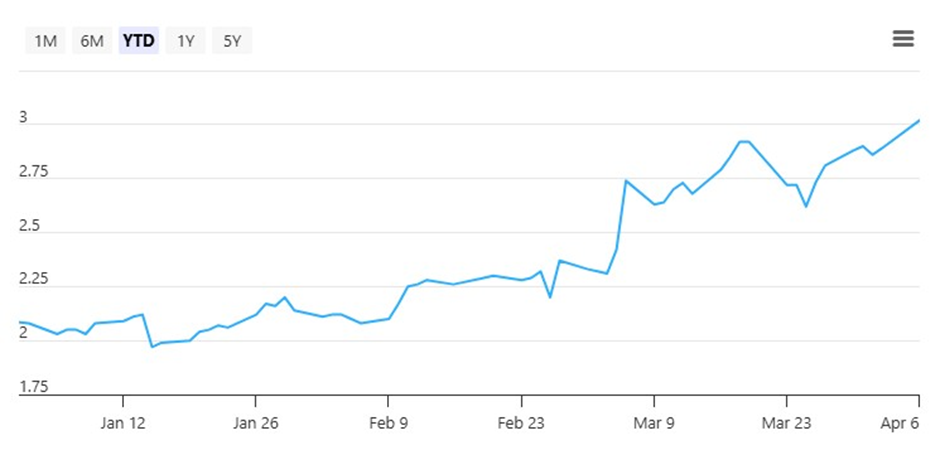

First Resources was another strong performer in the quarter, with its share price rising 38.8% to S$2.90 as of 31 March 2026.

The palm oil producer benefited from both strong FY2025 results and renewed investor interest in alternative fuels as oil prices climbed.

Higher energy prices tend to support demand for palm-based biodiesel, which helped lift sentiment towards the sector

First Resources’ FY2025 results were also especially strong.

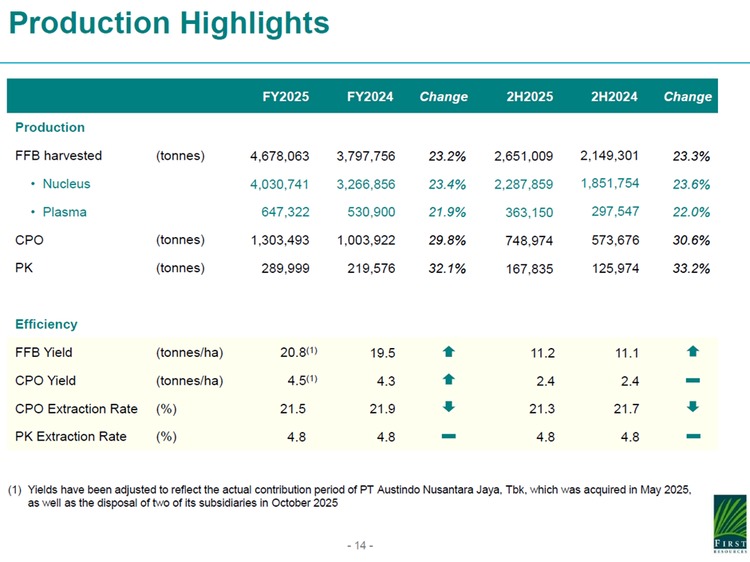

Revenue surged 59.9% year on year to US$1.66 billion, EBITDA rose 54.1% to US$614.9 million, and net profit increased 44.0% to US$353.9 million.

Operationally, fresh fruit bunch harvest rose 23.2% to 4.7 million tonnes, crude palm oil production increased 29.8%, and CPO yield improved to 4.5 tonnes per hectare.

Management remains constructive on 2026. Indonesia’s move from B35 to B40 biodiesel blending is expected to remain a key source of demand for palm oil.

On the production side, yield improvements from maturing replanted areas, together with the full year contribution from ANJ, which was acquired in May 2025, should provide further support.

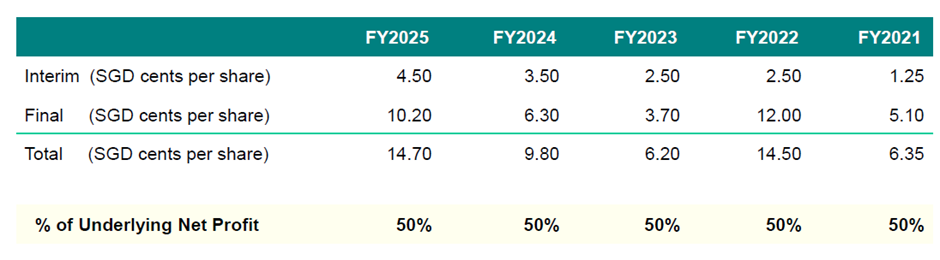

First Resources has also raised its dividend payout policy to up to 60% of underlying net profit, from 50% previously.

On dividends, First Resources proposed a final dividend of 10.2 Singapore cents per share.

Together with the interim dividend of 4.5 cents, this brings its full-year ordinary dividend to 14.7 cents per share.

Based on the 31 March 2026 share price of S$2.90, that implies a trailing yield of about 5.1%.

Consensus is forecasting FY2026 dividend per share of S$0.170, which would translate to a forward dividend yield of 5.9%.

For food security exposure, First Resources is a less obvious fit in a Singapore-focused portfolio, but could be worth watching.

Palm oil remains a strategically important commodity for Southeast Asia, especially as the region balances both food and energy security. Indonesia’s push towards higher biodiesel blending mandates such as B40 reinforces that long-term policy direction.

What stands out to me is that First Resources combines that structural theme with fairly strong operating momentum.

Its FY2025 results were solid, and the higher dividend policy makes it the most income-supportive name on this list, with a trailing yield of around 5.1%

I also like its integrated business model, the policy-backed demand floor from Indonesia’s biodiesel mandates, and its demonstrated ability to manage margins across the value chain.

Those qualities give it a stronger strategic footing than a pure commodity producer. That said, First Resources’ balance sheet is not as strong or as cash-rich as before following the ANJ acquisition, and earnings remain exposed to CPO price movements.

Related links:

#3 – UMS Integration Limited (SGX: 558)

UMS Integration is a precision engineering and manufacturing group whose main earnings driver is its semiconductor business.

It also has aerospace and other smaller operations, but the semiconductor segment remains the biggest part of the story.

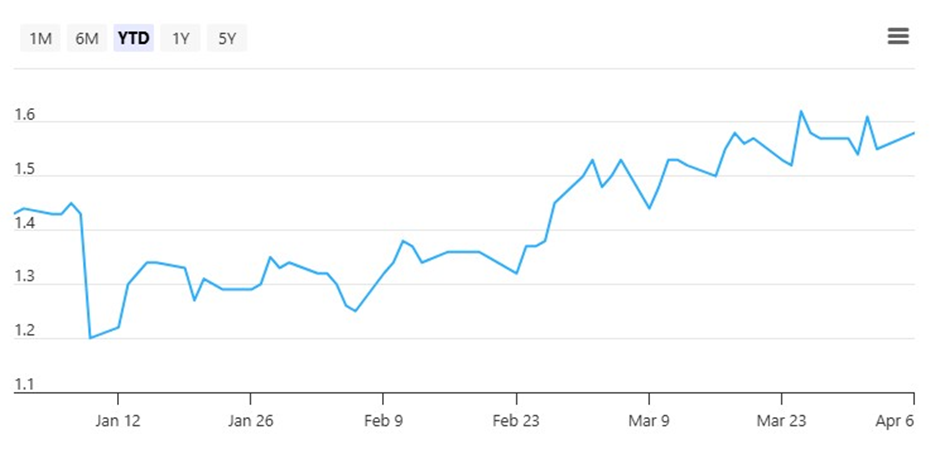

As of 31 March 2026, UMS’ share price stood at S$1.54, and rallied 35.6% in 1Q26.

The rally reflected continued investor interest in semiconductor names with exposure to AI driven demand and advanced packaging.

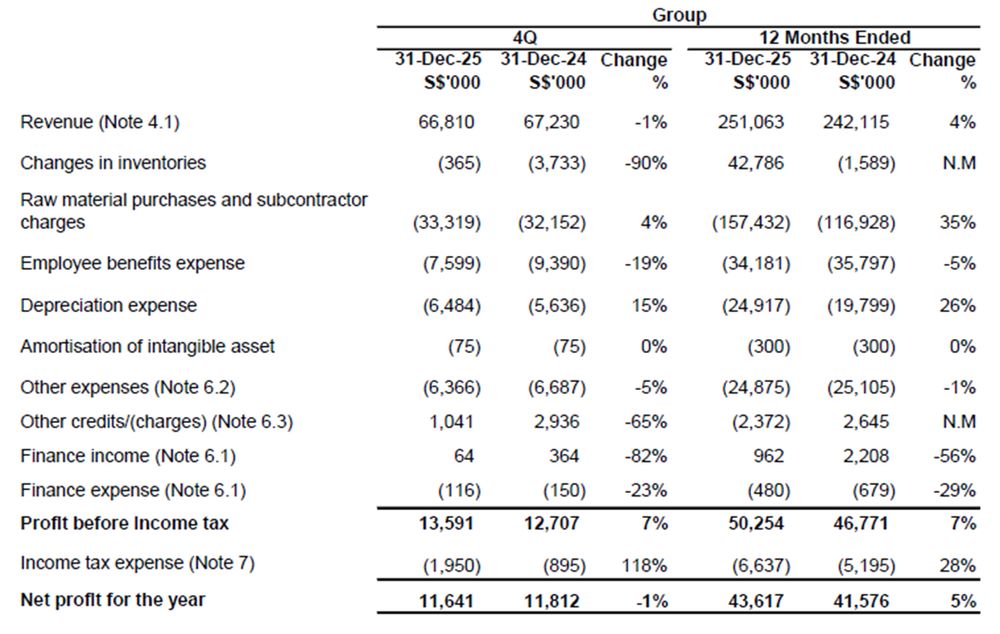

For FY2025, revenue rose 4% to S$251.1 million and net attributable profit increased 2% to S$41.6 million.

In 4QFY2025, revenue was broadly stable at S$66.8 million, down 1% year on year, while net attributable profit rose 5.7% quarter on quarter to S$11.1 million.

Within the quarter, semiconductor sales slipped 1% year on year to S$56.8 million, while aerospace revenue fell 11% to S$6.8 million. However, all business segments improved sequentially from 3QFY2025, suggesting momentum picked up towards the end of the year.

Sentiment was also supported by management’s positive outlook, as both of UMS’s key global customers are forecasting strong demand growth in 2026 and 2027.

The group also successfully renewed its Integrated System contract with a key customer for another three years.

UMS has been investing heavily to prepare for the next growth cycle.

Over the past four years, it has invested more than S$155 million to expand its manufacturing capabilities, particularly in smaller and more complex semiconductor devices as well as advanced packaging.

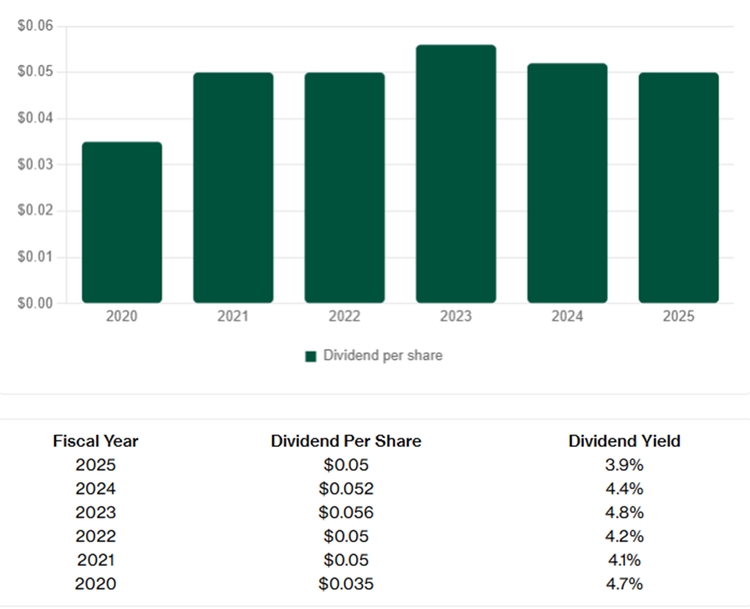

On dividends, UMS proposed a final dividend of 2.0 cents per share for FY2025. This comes on top of three interim dividends of 1.0 cent each declared during FY2025.

That brings FY2025’s total dividend to 5.0 cents per share on an unadjusted basis.

Adjusting for the company’s 1-for-4 bonus issue completed in January 2026, the post-bonus equivalent full-year dividend is about 4.4 cents per share.

Based on UMS’s share price of S$1.54 on 31 March 2026, this translates to a trailing dividend yield of about 2.9%.

While this remains attractive, further dividend growth may depend on how strongly the semiconductor cycle continues to recover.

UMS generated positive operating cash flow in FY2025, although free cash flow fell as the group continued to invest in expansion.

Consensus is forecasting FY2026 dividend per share of S$0.048, implying a forward dividend yield of 3.1%.

Overall, UMS has exposure to advanced packaging, while its recent contract renewal and new customer ramp-up suggest that its next phase of growth may be strengthening.

Related links:

#4 – Pan-United Corporation (SGX: P52)

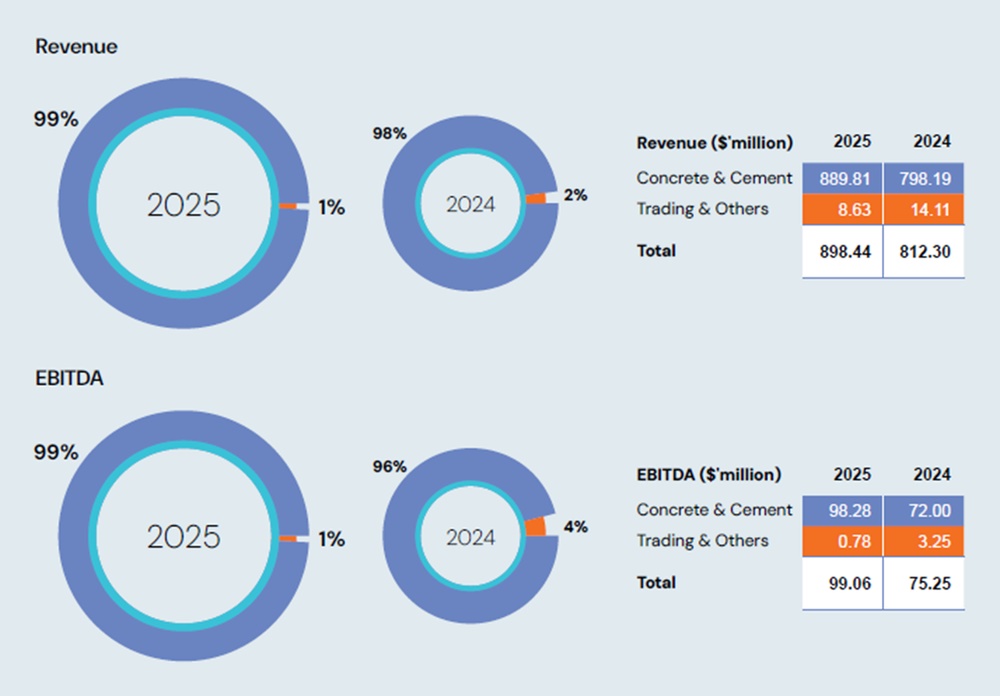

Pan-United Corporation is Singapore’s largest supplier of ready-mix concrete and cement, with around 40 per cent share of the local ready-mix concrete market.

As the market leader, it is focused on developing more sustainable, high-performance concrete solutions while also digitalising logistics across the built environment.

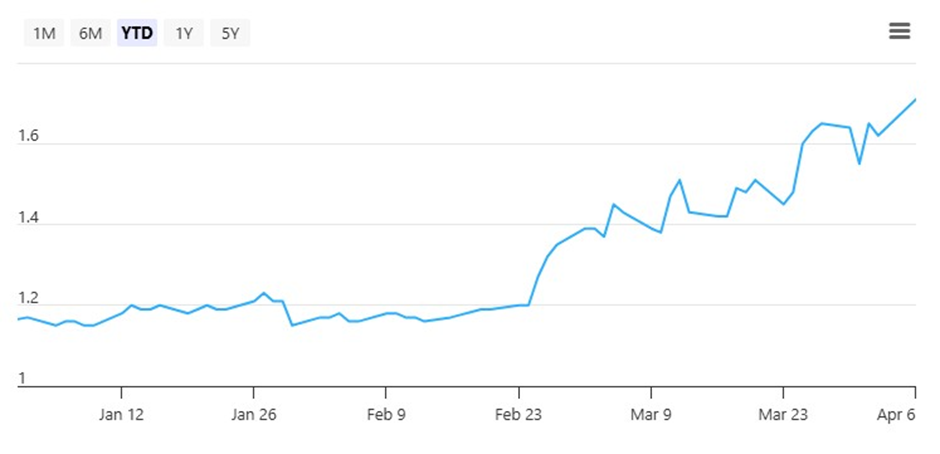

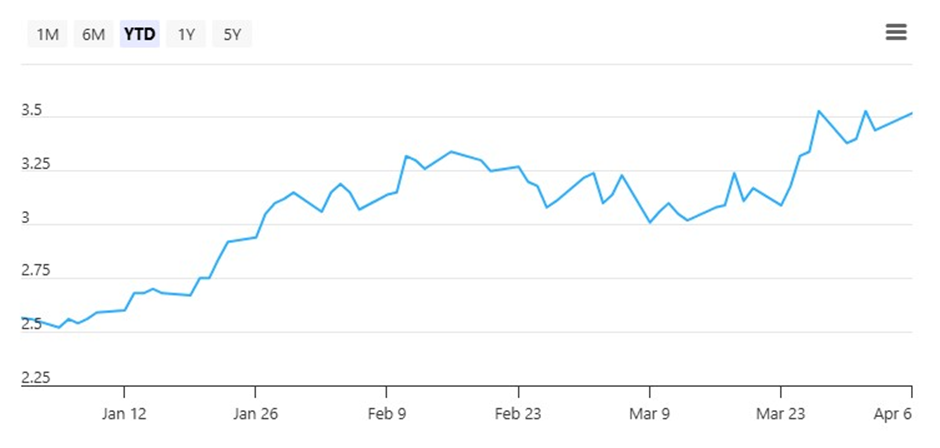

As of 31 March 2026, Pan-United’s share price stood at S$1.55, with a total gain of 33.6% in 1Q26.

The share price performance likely reflected growing confidence in Singapore’s construction pipeline and Pan-United’s ability to translate stronger activity into earnings growth.

Its FY2025 results were strong.

Revenue rose 11% year on year to S$898.4 million, EBITDA increased 32% to S$99.1 million, and net attributable profit climbed 24% to S$50.7 million.

Management attributed this to robust construction activity in Singapore as well as operating efficiencies from continued investment in technology.

The near term outlook also remains supportive.

Pan-United highlighted the Building and Construction Authority’s projection that total construction demand in Singapore could reach S$47 billion to S$53 billion in 2026, with ready-mix concrete volumes potentially rising to 15.0 million to 16.0 million cubic metres from 14.6 million in 2025.

Major projects such as Changi Airport Terminal 5, the Marina Bay Sands expansion and several MRT extensions should continue to underpin demand.

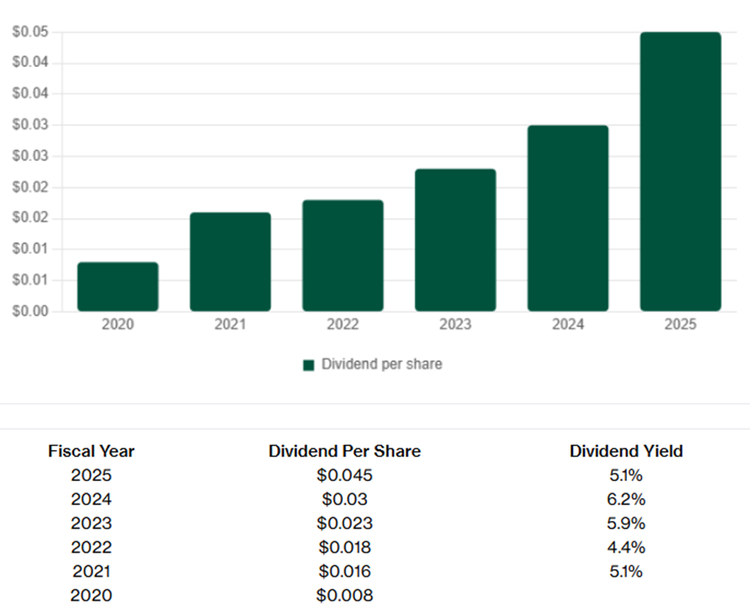

On dividends, Pan-United proposed a final dividend of 3.5 cents per share. Together with its 1 cent interim dividend, total FY2025 dividends came to 4.5 cents per share.

Based on its 31 March 2026 share price of S$1.55, that works out to a trailing yield of about 2.9%.

The dividend appears reasonably supported by stronger earnings and a net cash position, even after including lease liabilities.

Consensus is forecasting FY2026 dividend per share of S$0.055, implying a forward dividend yield of 3.5%.

For exposure to the government spending and infrastructure theme, Pan-United would be the clearest name on my watchlist.

It offers Singapore-centric demand resilience, improving margins and multi-year earnings visibility, supported by projects such as Changi Airport Terminal 5 and a constructive public construction pipeline.

Its balance sheet is another key strength. The group remains in a net cash position, with net cash to equity of 30.8 per cent.

To me, that matters because strong cash generation and low leverage give the company flexibility to sustain dividends, potentially raise shareholder returns, and continue investing in capacity and efficiency.

Related links:

#5 – UOB-Kay Hian Holdings (SGX: U10)

UOB-Kay Hian is a regional brokerage and financial services group. Its main businesses include stockbroking, futures broking, structured lending, investment trading, margin financing, and nominee and research services.

As of 31 March 2026, UOB-Kay Hian’s share price stood at S$3.40, representing a gain of 32.3% in 1Q26.

Among the five names here, UOB-Kay Hian is probably the clearest proxy for stronger investor participation.

When market trading activity picks up, broker earnings tend to respond quickly, and that was evident in its FY2025 results.

After-tax profit rose 7.0% year on year to S$239.4 million, while commission and trading income jumped 28.0% to S$471.9 million, supported by higher commission income from structured products and stronger trading volumes across Asian and US markets.

Momentum improved further in the second half of the year. After-tax profit rose 27.8% while total revenue increased 20.2%, highlighting the operating leverage that can kick in when market activity strengthens.

Management remains cautiously optimistic.

It noted encouraging investor participation in Singapore, Hong Kong and the US, while also flagging fee compression, digitalisation and broader macro conditions as factors to watch.

The group’s net asset value stood at S$2.3 billion at the end of 2025, providing solid balance sheet support.

The main risk is that expectations have moved higher after the sharp re-rating in the first quarter. Any softening in market volumes could weigh on earnings, while fee pressure from digital competition remains a longer term structural headwind.

On dividends, UOB-Kay Hian proposed a first and final dividend of 12.3 cents per share for FY2025, up from 11.9 cents a year earlier.

Based on the 31 March 2026 share price of S$3.40, that implies a trailing yield of about 3.6%.

The payout looks reasonably supported by its stronger earnings and healthy balance sheet, with group net asset value at S$2.3 billion at end-2025.

The trade-off is that dividend sustainability will still depend heavily on whether trading volumes remain healthy.

Consensus is forecasting a FY2026 dividend per share of S$0.143, which translates to a forward dividend yield of 4.2%.

Overall, UOB-Kay Hian’s earnings may benefit when trading volumes pick up across markets like Singapore, Hong Kong and the US.

As wealth activity in Asia continues to grow, brokerages with regional reach like UOB-Kay Hian could continue to benefit.

While UOB-Kay Hian has a strong net asset value base and low financial leverage, its earnings are still closely tied to market turnover.

If investor sentiment weakens and trading activity slows, profitability could come under pressure quite quickly.

Related links:

What would Beansprout do?

Despite the weakness in the market in the first few months of 2026, the strong performance of these five Next 50 stocks show that there are still opportunities beyond Singapore blue chips.

In this environment, quality still matters. I would look for companies with exposure to structural growth themes, while also having strong balance sheets or net cash positions that can help them stay resilient if conditions turn more volatile.

By that measure, Frencken, UMS and Pan-United would stand out to me. Frencken and UMS offer exposure to longer term growth in semiconductors and the AI supply chain, while Pan-United provides exposure to infrastructure and public sector spending in Singapore.

What stands out to me about these three companies is also their balance sheet strength, which may allow them to better withstand short term economic volatility.

One final point I would keep in mind is that these stocks tend to be smaller and less liquid than Singapore blue chip stocks in the Straits Times Index (STI). That means potentially higher volatility and greater liquidity risk.

Because of that, position sizing matters more here than it does with blue chips.

If I were looking to own these names, I would add them selectively, and only when I had a clear view on the specific driver behind each stock continuing from here.

Looking for more stock ideas to capture market opportunities? Explore our high conviction ideas here.

| Stock | The good | Key risks |

| Frencken Group | ● Resilient FY2025 performance, with revenue up 8.9% and net profit up 5.4% y-o-y. ● Semiconductor and industrial automation growth, with new capacity coming online in Malaysia, Singapore and the US. ● Net cash balance helps support its dividend, even though the trailing yield is only about 1.3%. |

● Exposure to renewed trade tensions, tariffs and foreign exchange swings. ● Analytical life sciences demand remains weaker, especially in Europe and the US. ● Lower yield means the stock is relying more on growth execution than income support. |

| First Resources | ● Strong FY2025 earnings recovery, with revenue up 59.9% and net profit up 44.0% y-o-y on higher CPO prices and production. ● Higher production, better plantation yields and the full-year contribution from ANJ support the outlook. ● Trailing dividend yield is about 5.1%, with a higher dividend policy of up to 60% of underlying net profit going forward. |

● Earnings remain exposed to palm oil prices and broader commodity swings. ● Indonesia government policy, export levies and geopolitical shifts can affect realised margins with little warning. ● Borrowings increased after the ANJ acquisition, so balance sheet discipline still matters. |

| UMS Integration | ● FY2025 revenue and profit still grew despite a mixed semiconductor backdrop. ● Three-year contract renewal with a key customer secured; both key global customers guiding robust demand growth for 2026 and 2027. ● Quarterly dividend profile remains attractive, with a trailing yield of about 3.2%. |

● Business is closely tied to the semiconductor cycle and the capex decisions of a small number of key customers. ● Heavy expansion spending has compressed free cash flow. ● Aerospace remains a smaller, weaker segment; overall earnings concentration is still high. |

| Pan-United Corporation | ● Strong FY2025 results, with revenue up 11%, EBITDA up 32% and net profit up 24% y-o-y. ● Singapore’s healthy construction pipeline could continue to support demand for ready-mix concrete. ● Net cash position and higher FY2025 dividend provide some support, with a trailing yield of about 2.9%. |

● Earnings remain tied to construction demand and project execution in Singapore. ● Margin pressure could return if input costs rise or the competitive environment for ready-mix intensifies. ● Dividend yield is still moderate, so the investment case depends more on continued earnings growth than income alone. |

| UOB-Kay Hian Holdings | ● FY2025 results improved, helped by stronger commission and trading income. ● Stronger investor participation across Singapore, Hong Kong and the US drove operating leverage in 2H2025. ● Proposed FY2025 dividend implies a trailing yield of about 3.6%. |

● Earnings remain closely linked to market turnover and investor sentiment. ● Fee compression and digital competition from lower-cost platforms are longer-term structural headwinds. ● After the recent rerating, market expectations for trading volumes are now higher. |

If you prefer exposure to blue chips rather, you can also learn more about the Straits Times Index (STI).

Against the backdrop of the Middle East conflict, learn more about how Singapore blue chip stocks may be impacted by higher oil prices here. As interest rate cut expectations moderate, learn how Singapore blue chip stocks may be impacted here.

Is there a Singapore stock you are looking out for amid the market volatility? Share with us in the comments below or in our Telegram group!

[Beansprout Exclusive Longbridge Promotion] Get bonus S$50 FairPrice voucher within 5 working days, plus 5% p.a. interest boost coupon (worth ~S$100) when you sign up for a Longbridge account via Beansprout. Plus, stand a chance to win S$150 CapitaVoucher weekly, with S$600 in total up for grabs. Promo ends on 30 April 2026. T&Cs apply. Learn more about the Longbridge promotion here.

Planning to invest in Singapore stocks? Compare the best Singapore brokers to find the right trading platform, and see the latest promotions and sign-up rewards available.

Follow Beansprout on Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.