Over the past six months, Lincoln Financial Group’s stock price fell to $37.38. Shareholders have lost 6.8% of their capital, which is disappointing considering the S&P 500 has climbed by 3.9%. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Lincoln Financial Group, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is Lincoln Financial Group Not Exciting?

Despite the more favorable entry price, we’re cautious about Lincoln Financial Group. Here are three reasons why LNC doesn’t excite us and a stock we’d rather own.

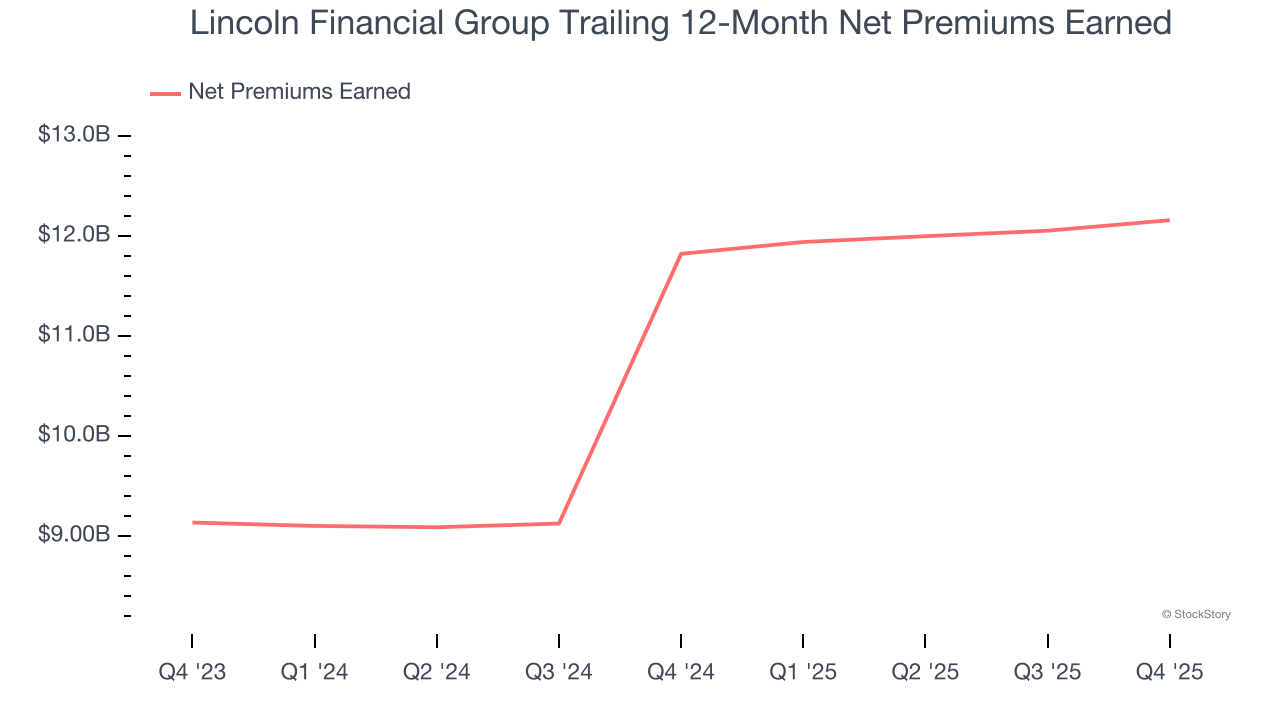

1. Net Premiums Earned Hit a Plateau

When insurers sell policies, they protect themselves from extremely large losses or an outsized accumulation of losses with reinsurance (insurance for insurance companies). Net premiums earned are therefore net of what’s ceded to reinsurers as a risk mitigation and transfer strategy.

Lincoln Financial Group’s net premiums earned was flat over the last five years, much worse than the broader insurance industry and in line with its total revenue.

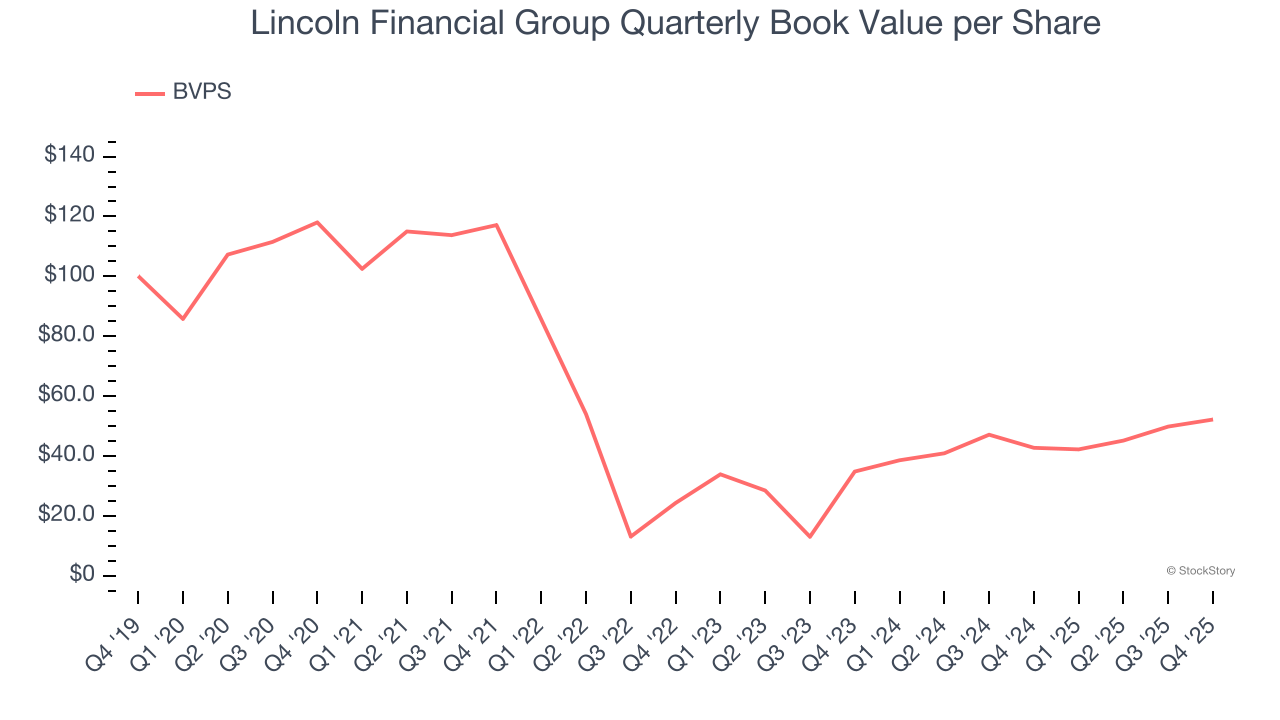

2. Growing BVPS Reflects Strong Asset Base

In the insurance industry, book value per share (BVPS) provides a clear picture of shareholder value, as it represents the total equity backing a company’s insurance operations and growth initiatives.

Although Lincoln Financial Group’s BVPS declined at a 15.1% annual clip over the last five years. the good news is that its growth inflected positive over the past two years as BVPS grew at an excellent 22.4% annual clip (from $34.82 to $52.20 per share).

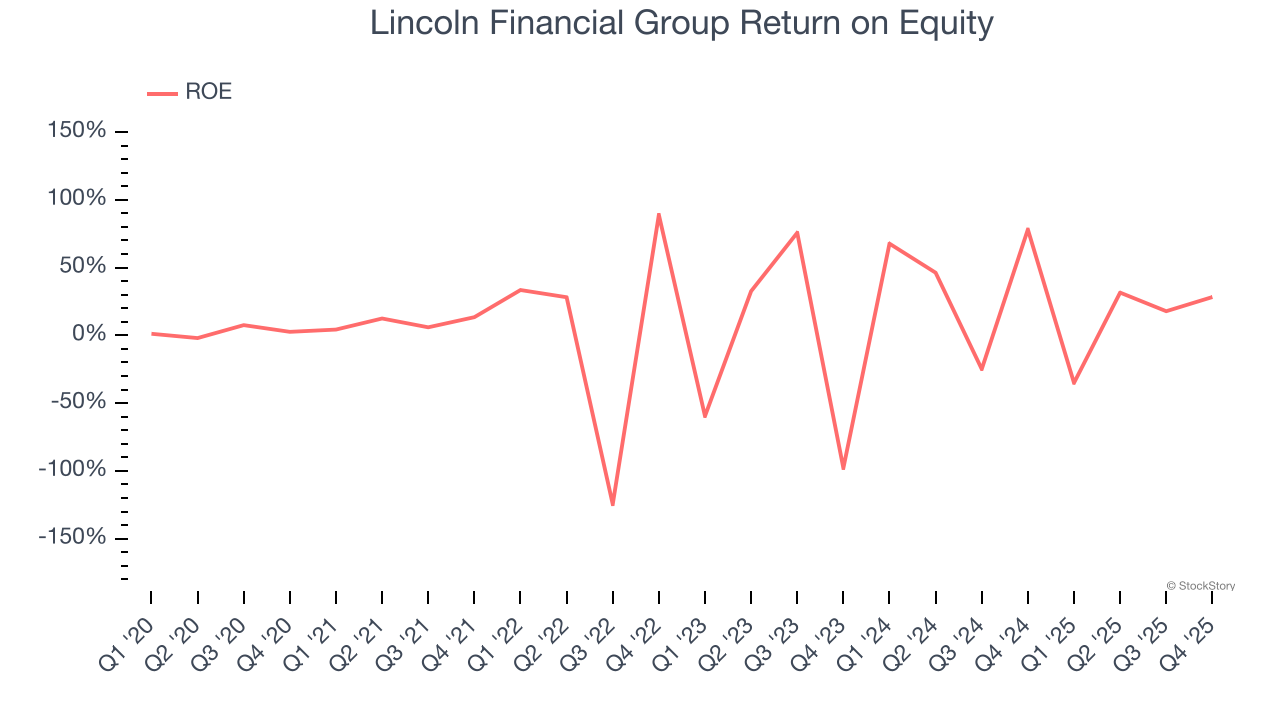

3. Previous Growth Initiatives Haven’t Impressed

Return on equity, or ROE, represents the ultimate measure of an insurer’s effectiveness, quantifying how well it transforms shareholder investments into profits. Over the long term, insurance companies with robust ROE metrics typically deliver superior shareholder returns through a balanced approach to capital management.

Over the last five years, Lincoln Financial Group has averaged an ROE of 11.1%, uninspiring for a company operating in a sector where the average shakes out around 12.5%.

Final Judgment

Lincoln Financial Group isn’t a terrible business, but it doesn’t pass our quality test. After the recent drawdown, the stock trades at 0.7× forward P/B (or $37.38 per share). While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We’re fairly confident there are better stocks to buy right now. We’d recommend looking at one of Charlie Munger’s all-time favorite businesses.

Stocks We Would Buy Instead of Lincoln Financial Group

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.