What happened?

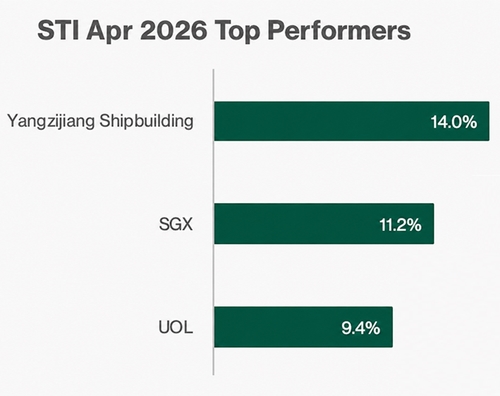

Singapore blue chips rebounded in April 2026.

After the volatility in March, the Straits Times Index remained resilient for much of April.

We have seen OCBC’s share price hit an all-time high in April, while DBS has also gained after announcing their latest 1Q 2026 results.

At the same time, Singapore REITs have also bounced back from their recent lows.

This came as Singapore blue chip stocks continued to attract investor interest, with more investors looking at whether Singapore stocks may still offer growth and income opportunities in 2026.

In this article, we examine the 3 best-performing Singapore blue chip stocks in April 2026, and whether their latest results, business momentum and dividend outlook are strong enough to support the rally.

3 best-performing Singapore blue chip stocks in April

#1 -Yangzijiang Shipbuilding Holdings Ltd (SGX: BS6)

Yangzijiang Shipbuilding is one of Asia’s leading shipbuilders.

The group focuses mainly on commercial vessels such as containerships, bulk carriers, tankers and other specialised vessels.

Yangzijiang Shipbuilding’s share price closed at S$4.31 on 30 April 2026, up from S$3.78 at the end of March. This represents a gain of about 14.0% in April.

Yangzijiang Shipbuilding has also been one of the strongest performing blue chips in February 2026.

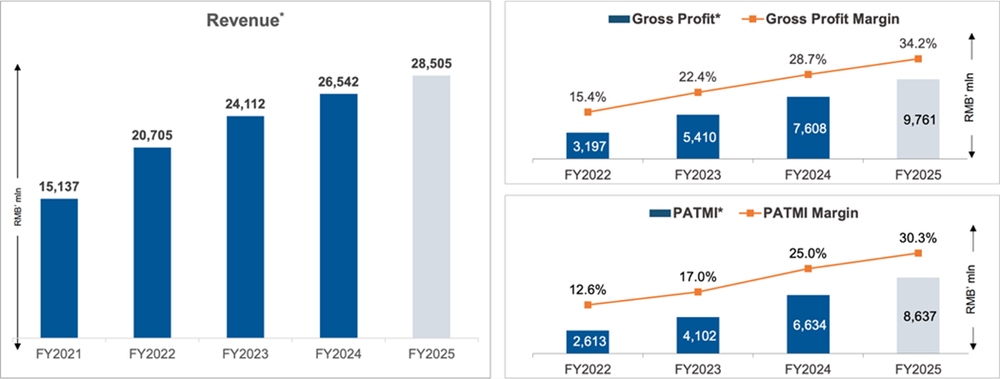

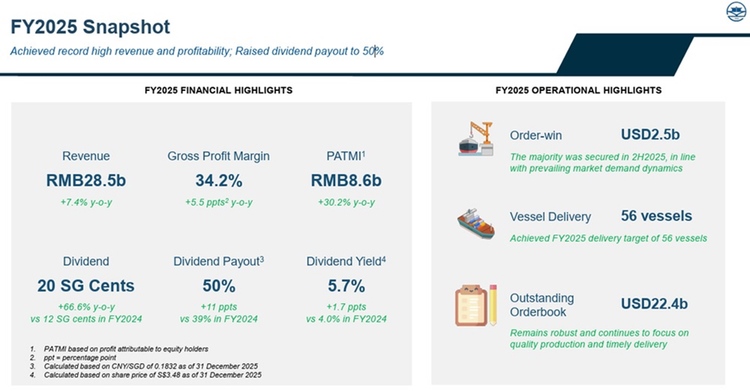

For FY2025, revenue rose 7.4% year on year to RMB28.5 billion. Profit attributable to shareholders increased 30.2% to RMB8.6 billion. Gross profit margin also improved to 34.2%, helped by lower steel costs and better pricing for newbuild contracts.

Profitability also improved meaningfully.

Management said gross margin expanded on the back of lower steel costs and better pricing for newbuild contracts. Gross margins of around 35% are exceptionally high by historical standards, and management described this as a rare upcycle.

For now, it expects margins at this level to be sustained through 2026 and 2027, barring any major swings in steel prices or the US dollar against the renminbi.

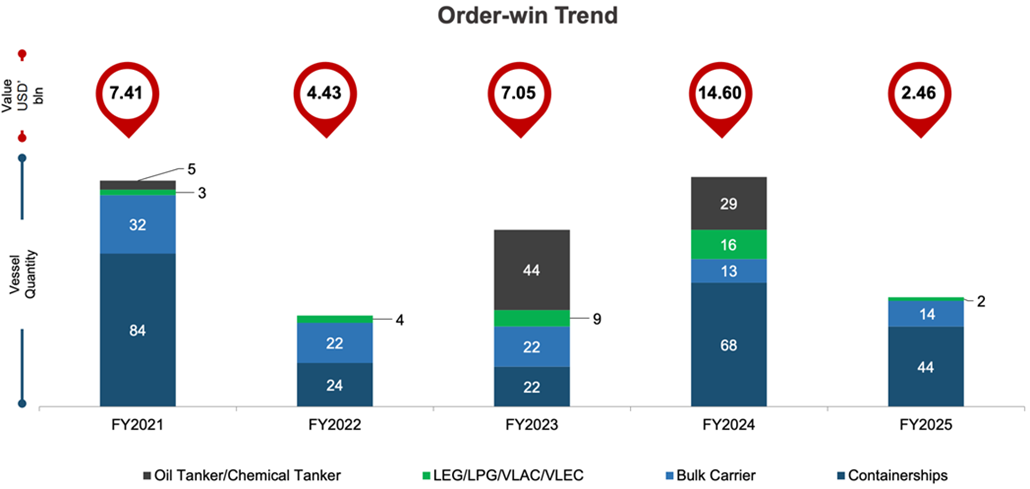

Operationally, the group delivered 56 vessels in FY2025, meeting its delivery target for the year. It also ended FY2025 with an outstanding order book of US$22.4 billion across 245 vessels, giving it revenue visibility into 2029 and beyond.

Green vessels accounted for about 71% of the outstanding order book by value, while containerships remained the dominant vessel type.

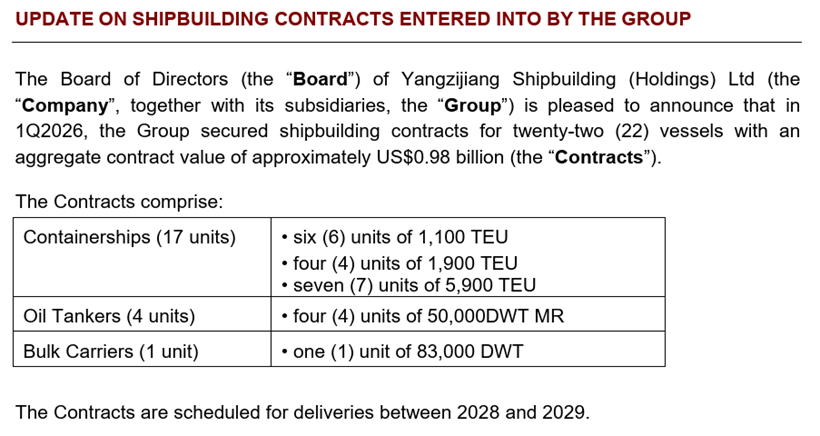

The order momentum has continued into 2026.

In the first quarter of 2026, Yangzijiang secured contracts for 22 vessels worth about US$980 million.

These orders included 17 container ships, four oil tankers and one bulk carrier, with deliveries scheduled between 2028 and 2029. After factoring in these contracts and deliveries, its outstanding order book stood at about US$22.8 billion for 256 vessels.

Yangzijiang has also moved to deepen its relationship with Seaspan Corporation, one of its long-standing customers.

In March, the group announced that it would acquire a 10% stake in Poseidon Corp, the indirect parent company of Seaspan Corporation.The acquisition consideration is US$825.7 million and will be funded by internal cash resources.

The company said the transaction would strengthen its strategic relationship with Seaspan and improve alignment between vessel demand, production planning and yard development.

This could improve Yangzijiang’s visibility over future vessel demand.

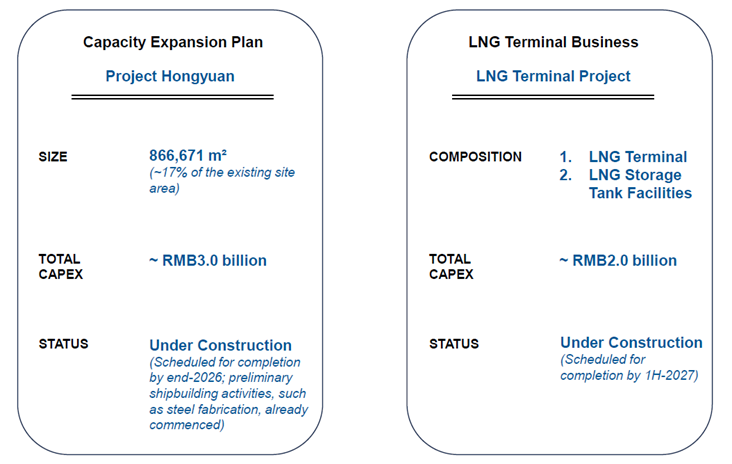

In terms of future growth, Yangzijiang is also investing in capacity expansion and LNG-related infrastructure.

Project Hongyuan is under construction and scheduled for completion by end-2026, with preliminary shipbuilding activities such as steel fabrication already started. The project covers about 866,671 square metres, equivalent to about 17% of the existing site area.

Separately, its LNG Terminal Project, which includes an LNG terminal and LNG storage tank facilities, is also under construction and scheduled for completion by 1H 2027. Together, these projects show how Yangzijiang is preparing for longer-term demand from higher-value and greener vessels.

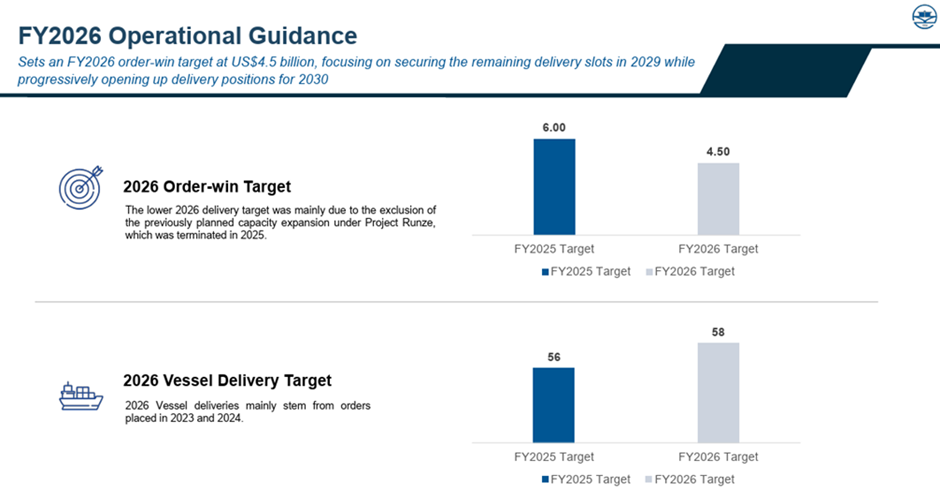

At the same time, management appears to be taking a more measured approach to new orders.

Its FY2026 order win target of 4.5 billion yuan suggests that profitability and execution are being prioritised over chasing volume.

On dividends, Yangzijiang proposed a dividend of 20 Singapore cents per share for FY2025, up from 12 Singapore cents in FY2024. This raised its dividend payout ratio to 50%.

Based on the share price of S$4.28, the consensus dividend of 21.5 cents implies a forward dividend yield of about 5.1%.

Find out how much dividends you would have received as a shareholder of Yangzijiang Shipbuilding (Holdings) Ltd in the past 12 months with the calculator below.

Related Links:

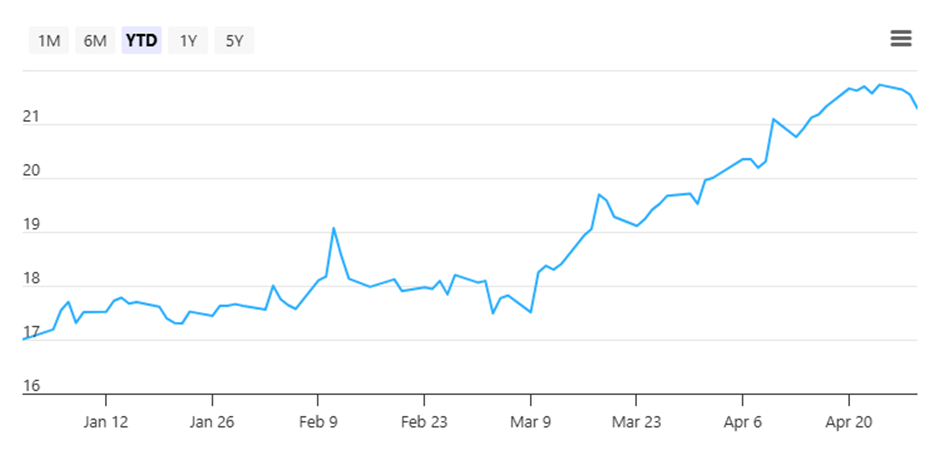

#2 – SGX: Singapore Exchange Limited (SGX: S68)

Singapore Exchange is Singapore’s main stock exchange and runs a multi-asset platform spanning equities, derivatives, fixed income, currencies, data and index services.

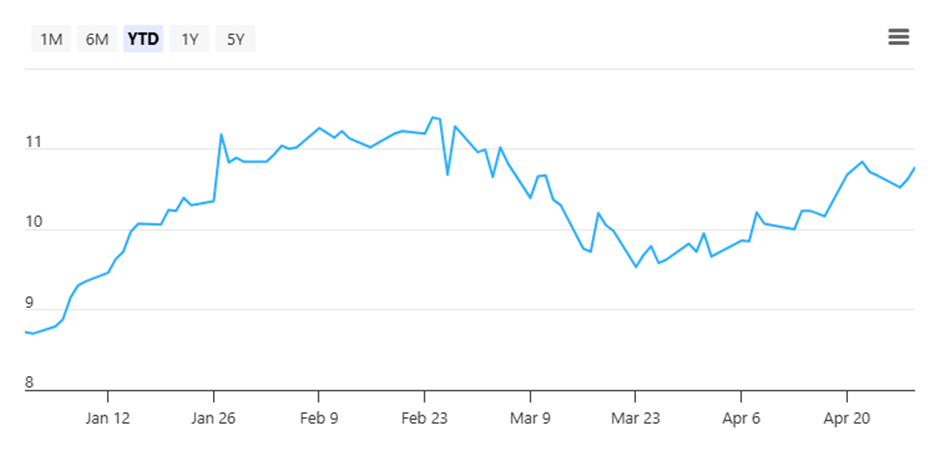

As of 30 April 2026 closing, SGX’s share price stood at S$21.70, representing a gain of about 11.2% over the past 1 month.

The rally continued to be supported by stronger trading activity across Singapore’s capital markets.

[1] In March, securities market turnover rose 78% year on year to S$52.8 billion, while securities daily average value rose 62% year on year to S$2.4 billion. This was the highest securities daily average value since October 2007.

The improvement was not limited to large-cap stocks.

Retail participation reached a fresh 13-year high, while institutions continued to net buy small- and mid-cap stocks for the third consecutive month. This suggests that trading interest in Singapore stocks has broadened beyond the biggest blue chips.

Activity also picked up across SGX’s other asset classes.

SGX-listed exchange-traded funds (ETFs) attracted S$1.3 billion of net inflows in the January-to-March quarter, with assets under management rising to S$19 billion across 53 ETFs.

Derivatives traded volume rose 40% year on year in March to a record 38.3 million contracts, while FX futures volume also reached an all-time high.

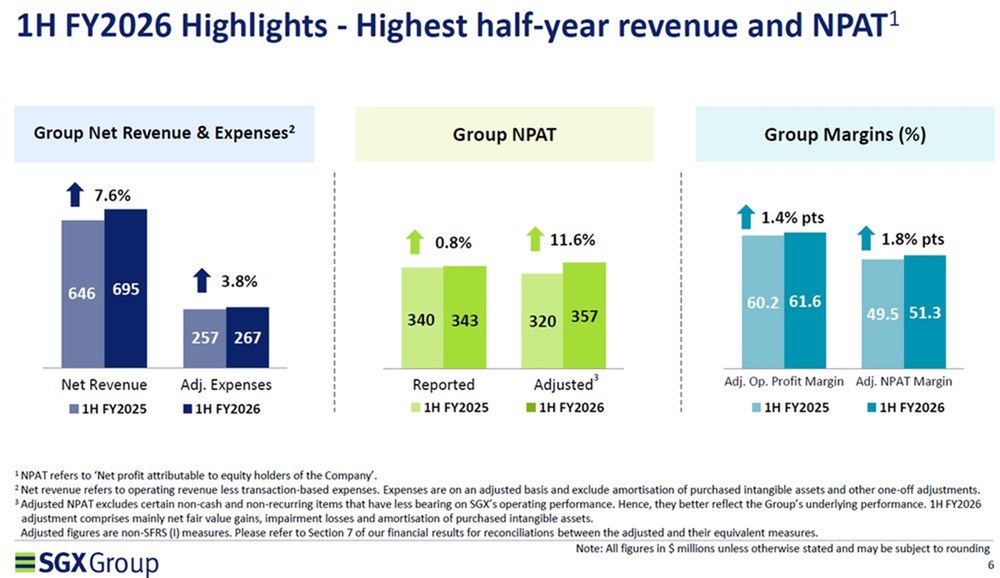

Earlier, we have seen how the improvement in trading activity has helped to boost SGX’s revenue and net profit.

For 1H FY2026 (six months ending December 2025), net revenue rose 7.6% year on year to S$695.4 million, while adjusted net profit increased 11.6% to S$357.1 million. Adjusted operating profit margin also improved to 61.6% from 60.2%.

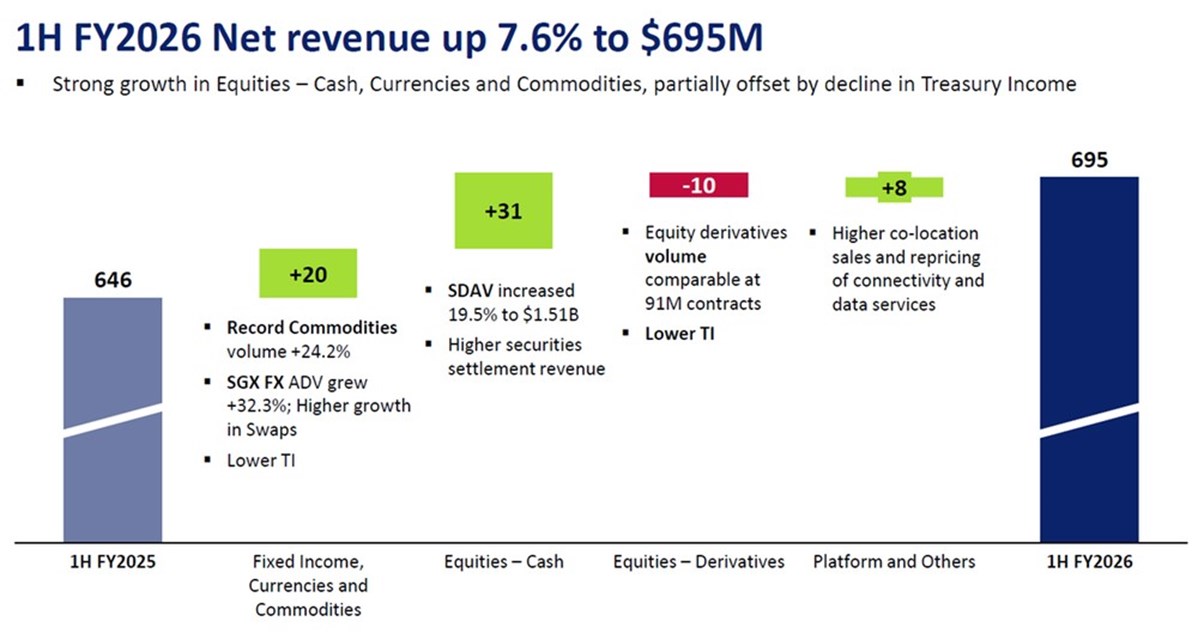

The improvement was broad-based across the business.

In cash equities, securities daily average traded value rose 19.5% to S$1.51 billion, supporting a 16% increase in Equities-Cash net revenue.

In derivatives and currencies, SGX recorded record commodities volume growth of 24.2%, while SGX FX average daily volume climbed 32.3% to a record US$180 billion.

Equity derivatives volume was broadly stable at 91 million contracts.

Taken together, this suggests that the stronger earnings were supported by higher activity across several of SGX’s key business lines rather than by a single one-off boost.

Management also continued to highlight execution discipline.

Adjusted expenses rose by 3.8%, with SGX continuing to invest in sales and product capabilities as well as platform modernisation, while maintaining its FY2026 expense and capital expenditure guidance.

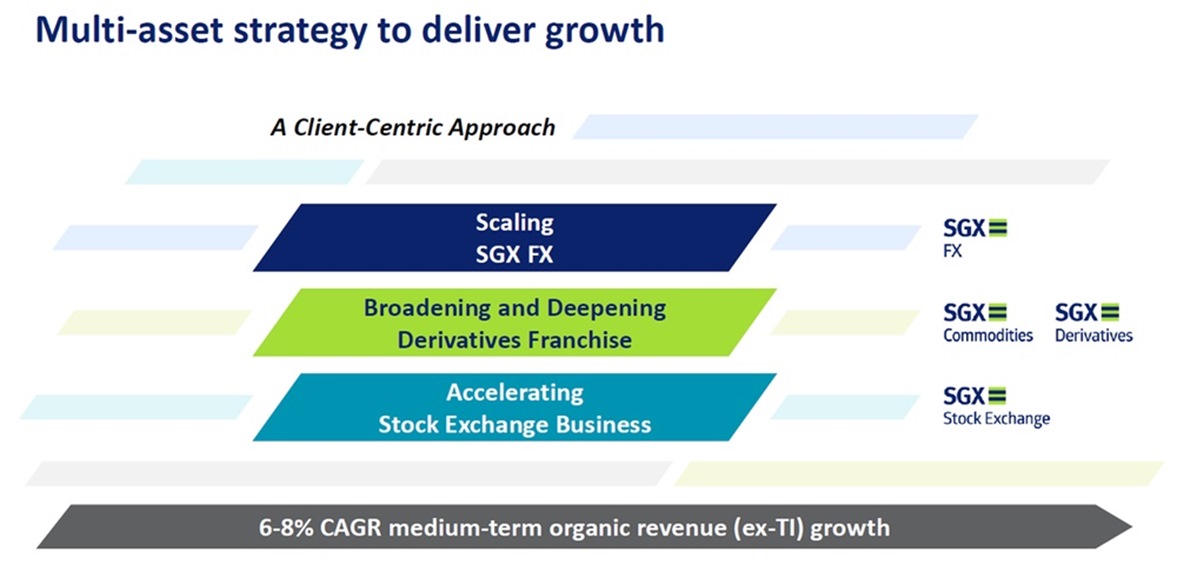

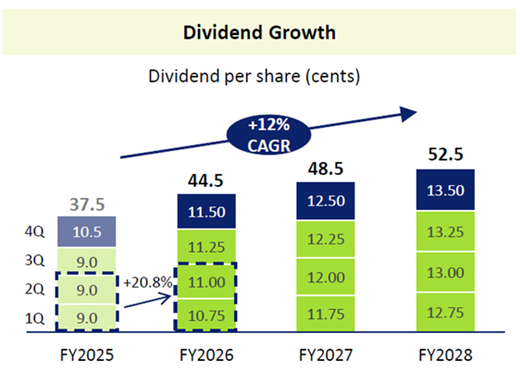

At the same time, it reiterated that its multi-asset strategy remains on track to deliver medium-term organic revenue growth of 6% to 8%, and that it remains committed to increasing its quarterly dividend by 0.25 cents through FY2028.

SGX declared an interim quarterly dividend of 11.0 cents per share in the recent quarter.

If SGX maintains its current 1H FY2026 dividend run rate and guidance, that would imply about 44.5 cents per share for a full year. Based on the share price of S$21.70, that works out to a forward yield of about 2.1%.

Find out how much dividends you would have received as a shareholder of Singapore Exchange in the past 12 months with the calculator below.

Related Links:

#3 – UOL Group Limited (SGX: U14)

UOL Group is a leading property and hospitality group with a portfolio of development and investment properties, hotels, and serviced suites.

It was also one of the top 3 performers among the blue chips in January 2026.

As of 30 April 2026, UOL’s share price closed at S$10.63, reflecting a month-to-date performance of +9.4%.

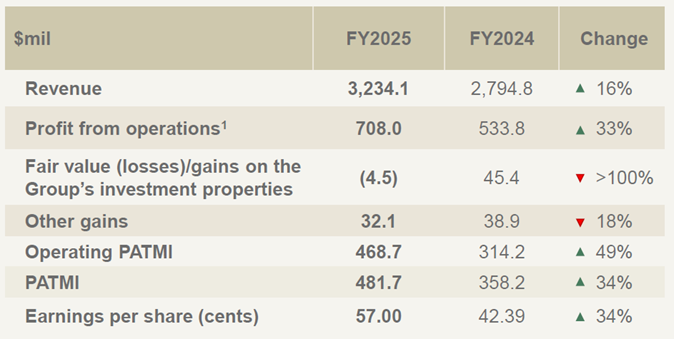

For FY2025, UOL’s operating Profit Attributable to the Minority Interest (PATMI) rose 49% to S$468.7 million. Group revenue increased 16% to S$3.23 billion, supported by higher contributions across most segments.

Net attributable profit also rose 34% to S$481.7 million.

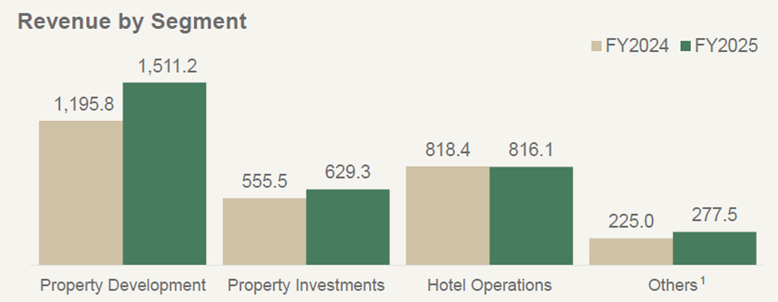

The improvement was driven mainly by property development and property investments.

Revenue from property development increased 26% to S$1.51 billion. This was due mainly to higher progressive revenue recognition from Pinetree Hill, Watten House and Meyer Blue, as well as new revenue recognition from UpperHouse at Orchard Boulevard.

Revenue from property investments rose 13% to S$629.3 million.

This was helped by revenue from UOL’s newly acquired interest in 388 George Street in Sydney, better performance from Singapore Land Tower after its asset enhancement works, and a full-year contribution from Odeon 333.

UOL’s residential sales momentum also remained healthy.

As of 22 February 2026, Skye at Holland was 99% sold, UpperHouse at Orchard Boulevard was 77% sold, and Parktown Residence was 94% sold. Watten House was 98% sold, Pinetree Hill was 97% sold, and Meyer Blue was 73% sold.

This helps to provide earnings visibility as revenue is recognised progressively.

UOL has also been replenishing its land bank.

Its upcoming pipeline includes Thomson View Condominium, Dorset Road and the Hougang Central integrated development. UOL’s FY2025 presentation indicated that these projects are targeted for launch between 4Q 2026 and 2H 2027.

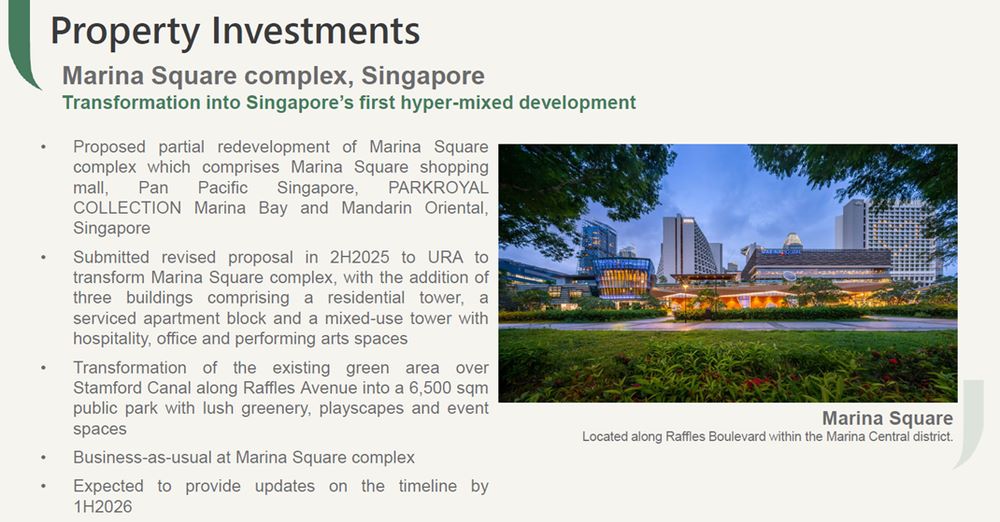

Another area investors are watching is Marina Square.

SingLand, UOL’s property arm, had submitted a revised proposal in 2H2025 to transform Marina Square into Singapore’s first “hyper-mixed” development. The plan includes a residential tower, a serviced apartment block and a mixed-use tower with hospitality, office and performing arts spaces.

Management shared that an update on the timeline for Marina Square’s redevelopment will be provided by 1H26. The project remains on track and is currently pending approval from Urban Redevelopment Authority (URA).

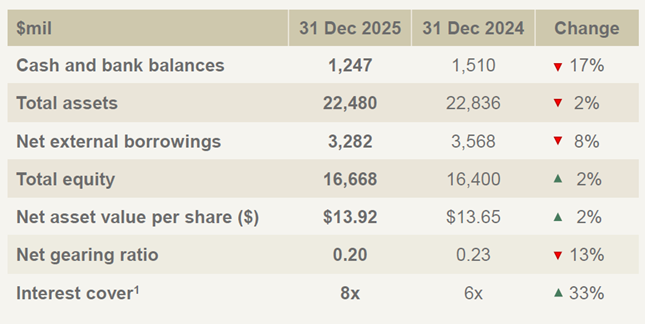

UOL’s balance sheet remains healthy.

Its net gearing ratio fell to 0.20 times as of 31 December 2025, from 0.23 times a year earlier. This was due to lower borrowings and higher total equity from profits for the year.

UOL’s current price-to-book (P/B) ratio of 0.76x is higher than its historical average P/B ratio of 0.58x.

The group also benefited from lower finance expenses.

Finance expenses fell 14% to S$175.9 million in FY2025, while its effective weighted average interest rate on external borrowings declined to 3.29% from 3.73% a year earlier.

This matters because property stocks can be sensitive to interest rates.

Lower borrowing costs can help support earnings, while a strong balance sheet gives UOL more flexibility to pursue new projects or asset enhancement opportunities.

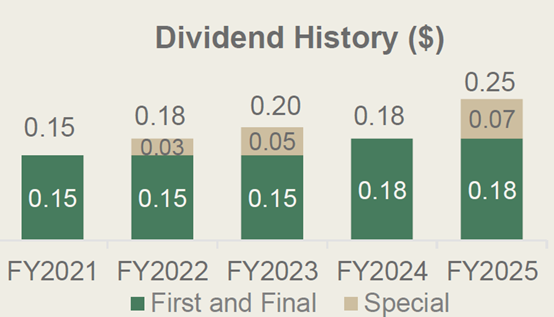

On dividends, UOL Group typically declares dividends annually at the rate of approximately 20-50% of the profit after tax and minority interest (PATMI).

UOL proposed a special dividend of 7 cents per share, on top of a first and final dividend of 18 cents per share. This brought its total FY2025 dividend to 25 cents per share, representing a payout ratio of 44%.

Based on the share price of S$10.63 as of 30 April 2026 closing, the FY2025 dividend implies a forward dividend yield of about 2.4%.

Find out how much dividends you would have received as a shareholder of UOL Group Limited in the past 12 months with the calculator below.

What would Beansprout do?

The strong performance of Yangzijiang Shipbuilding, SGX and UOL Group in April is a reminder that Singapore blue chips can still deliver meaningful gains, even after a volatile start to the year.

For blue chip names like these where liquidity is unlikely to be the main concern, I would focus instead on earnings quality, balance sheet strength and valuations.

SGX stands out for its more resilient earnings base and clearer dividend growth path through FY2028.

UOL’s balance sheet looks healthy, with net gearing falling to 0.20 times and lower finance costs supporting earnings.

Yangzijiang offers the highest forward dividend yield of about 5.1%, though its earnings remain more cyclical.

The main concern is valuation, as all three stocks appear less compelling after their strong April run.

Because of this, I would add these stocks to my watchlist and look for a good entry point, rather than to chase the recent momentum.

| Stock | The good | Key risks |

| Yangzijiang Shipbuilding | ● Record FY2025 earnings, with revenue and PATMI reaching new highs ● Large order book of about US$22.8 billion provides revenue visibility ● Highest dividend yield among the three at about 5.1% |

● Shipbuilding remains cyclical and exposed to global trade conditions ● Margins may be affected by steel prices and currency movements ● Large Poseidon investment means capital allocation should be watched |

| UOL Group | ● FY2025 operating PATMI rose 49%, supported by property development and property investments ● Healthy residential sales momentum provides earnings visibility ● Strong balance sheet, with net gearing of 0.20x |

● Dividend yield is lower if we exclude the special dividend ● Property stocks remain sensitive to interest rates and property market sentiment ● Future growth depends on project execution and new launch demand |

| Singapore Exchange | ● Strong 1H FY2026 results, with higher revenue and adjusted net profit ● Market activity has broadened across equities, derivatives, FX and ETFs ● Clearer dividend growth path, with forward dividend yield of about 2.1% |

● Lowest dividend yield among the three ● Earnings remain linked to trading volumes and broader market activity ● After the recent rally, expectations may be higher |

If you are looking for more stock ideas to capture market opportunities, you can explore our high conviction ideas here.

If you prefer broad exposure to blue chips without picking individual names, you can also learn more about the Straits Times Index (STI).

Is there a Singapore blue chip stock you are looking out for? Share with us in the comments below or in our Telegram group!

Planning to invest in Singapore blue chip stocks? Check out Beansprout’s guide to the best stock trading platforms in Singapore with the latest promotions to invest in the Singapore market and see the latest promotions and sign-up rewards available.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.