Tenable (TENB +2.50%) is a cybersecurity company with a market capitalization of just $2.4 billion, so it’s much smaller than some of the industry leaders, including CrowdStrike and Palo Alto Networks, which are worth more than $100 billion each.

However, Tenable specializes in a niche called exposure management, which is a proactive form of cybersecurity designed to identify vulnerabilities in corporate networks before they can be exploited by malicious actors. This is a valuable segment of the industry, but it means Tenable has a smaller addressable market than its peers that offer more holistic solutions.

Tenable stock is down 65% from its 2022 record high, but its business is growing nicely, and so Wall Street thinks the dip might be an opportunity. The analysts tracked by The Wall Street Journal have a consensus overweight (bullish) weighting on the stock, and their average price target points to solid upside over the next 12 months.

Image source: Getty Images.

Artificial intelligence is enhancing Tenable’s capabilities

Tenable owns the Nessus platform, which is one of the cybersecurity industry’s most accurate and most widely deployed vulnerability management solutions. It constantly scans devices, networks, and operating systems for weak points, so businesses can patch them before they are exploited. But over the past few years, Nessus has become an important onramp into Tenable’s growing portfolio of other products.

In 2022, the company launched Tenable One, which is a more comprehensive platform for exposure management. It now uses artificial intelligence (AI) to automate workflows, from mapping potential attack paths to remediating vulnerabilities, shifting these critical tasks away from humans who simply can’t respond to threats as fast as algorithms can.

In March, Tenable introduced Hexa AI, which is Tenable One’s new agentic engine. It’s an all-powerful digital assistant that coordinates AI agents to automate even more cybersecurity workflows, and it’s capable of taking action in certain situations. In simple terms, Tenable One used to uncover vulnerabilities for a business and suggest ways to rectify them, whereas Hexa AI can go ahead and fix them autonomously without any human intervention.

Today’s Change

(2.50%) $0.53

Current Price

$21.69

Key Data Points

Market Cap

$2.4B

Day’s Range

$21.66 – $22.05

52wk Range

$15.72 – $35.69

Volume

57K

Avg Vol

3.2M

Gross Margin

78.17%

Tenable has more than 40,000 enterprise customers, making it the world’s leading player in the market for exposure management. During the first quarter of 2026 (ended March 31), a record 2,204 of those customers had annual contract values of more than $100,000, which was up by 8% from the year-ago period. Therefore, it’s clear that large organizations are recognizing the importance of advanced exposure management software.

Steady revenue growth, with an improving bottom line

Tenable generated $262.1 million in revenue during the first quarter, a 9.6% increase over the year-ago period, and it also topped the company’s forecast range of $257 million to $260 million. The strong result prompted management to increase its full-year revenue guidance for 2026 by $3 million to $1.073 billion at the midpoint of the range.

Tenable also spent money more conservatively during the quarter to improve its bottom line, with its total operating expenses shrinking by 4% year over year. As a result, the company eked out a net profit of $1.4 million. That might not sound like much, but it was a huge positive swing from the $22.9 million loss it generated in the same quarter last year.

After excluding one-off and non-cash expenses such as stock-based compensation, Tenable delivered an adjusted (non-GAAP) profit of $55.5 million, which increased by 25% from the year-ago period.

Wall Street is bullish on Tenable stock

The Wall Street Journal tracks 26 analysts who cover Tenable stock, and 11 have given it a buy rating. One other is in the overweight camp, while the remaining 14 recommend holding. None recommend selling. The analysts have an average price target of $27.26, which suggests the stock could climb by 31% over the next 12 months or so. But the Street-high target of $38 implies an even greater potential upside of 82%.

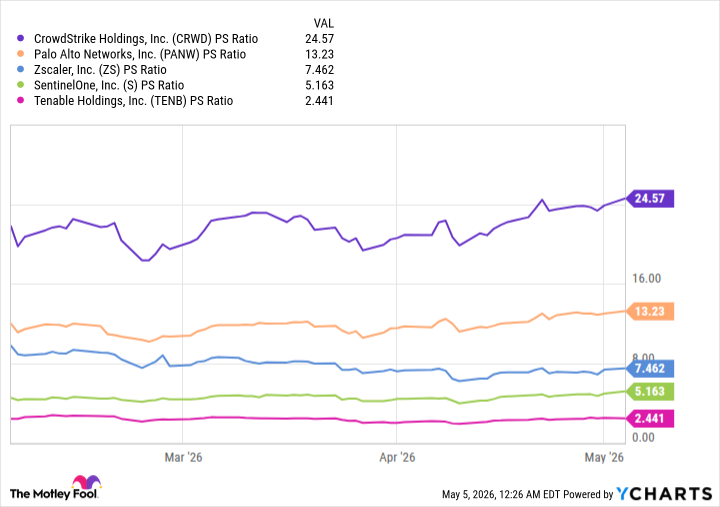

I think both targets are achievable because of Tenable’s valuation. Its stock is trading at a price-to-sales (P/S) ratio of just 2.4 as I write this, making it one of the cheapest names in the entire cybersecurity industry.

CRWD PS Ratio data by YCharts

Tenable stock would have to soar by 422% just to trade in line with the average P/S ratio of the other four cybersecurity stocks in the preceding chart, which is 12.5. I’m not suggesting a gain of that magnitude is on the table, because Tenable is sacrificing some revenue growth right now to focus on profitability, which will affect the P/S ratio investors are willing to pay for its stock. However, it certainly makes Wall Street’s price targets look realistic.