Over the last 7 days, the United States market has risen by 1.6%, contributing to a substantial 28% increase over the past year, with earnings expected to grow by 17% annually in the coming years. In this favorable environment, growth companies with high insider ownership can be particularly appealing as insiders often have unique insights into their company’s potential and are willing to invest alongside other shareholders.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Uxin (UXIN) | 34.4% | 74.1% |

| Upstart Holdings (UPST) | 14.1% | 58.1% |

| QT Imaging Holdings (QTI) | 23.9% | 104.2% |

| Karman Holdings (KRMN) | 15.6% | 52.6% |

| Forum Markets (FRMM) | 31.8% | 127.7% |

| Figure Technology Solutions (FIGR) | 26.8% | 54.1% |

| Corcept Therapeutics (CORT) | 11.7% | 48.9% |

| Astera Labs (ALAB) | 10.3% | 31.5% |

| AppLovin (APP) | 27.4% | 21.7% |

| Abeona Therapeutics (ABEO) | 16.7% | 32.9% |

Let’s uncover some gems from our specialized screener.

Simply Wall St Growth Rating: ★★★★☆☆

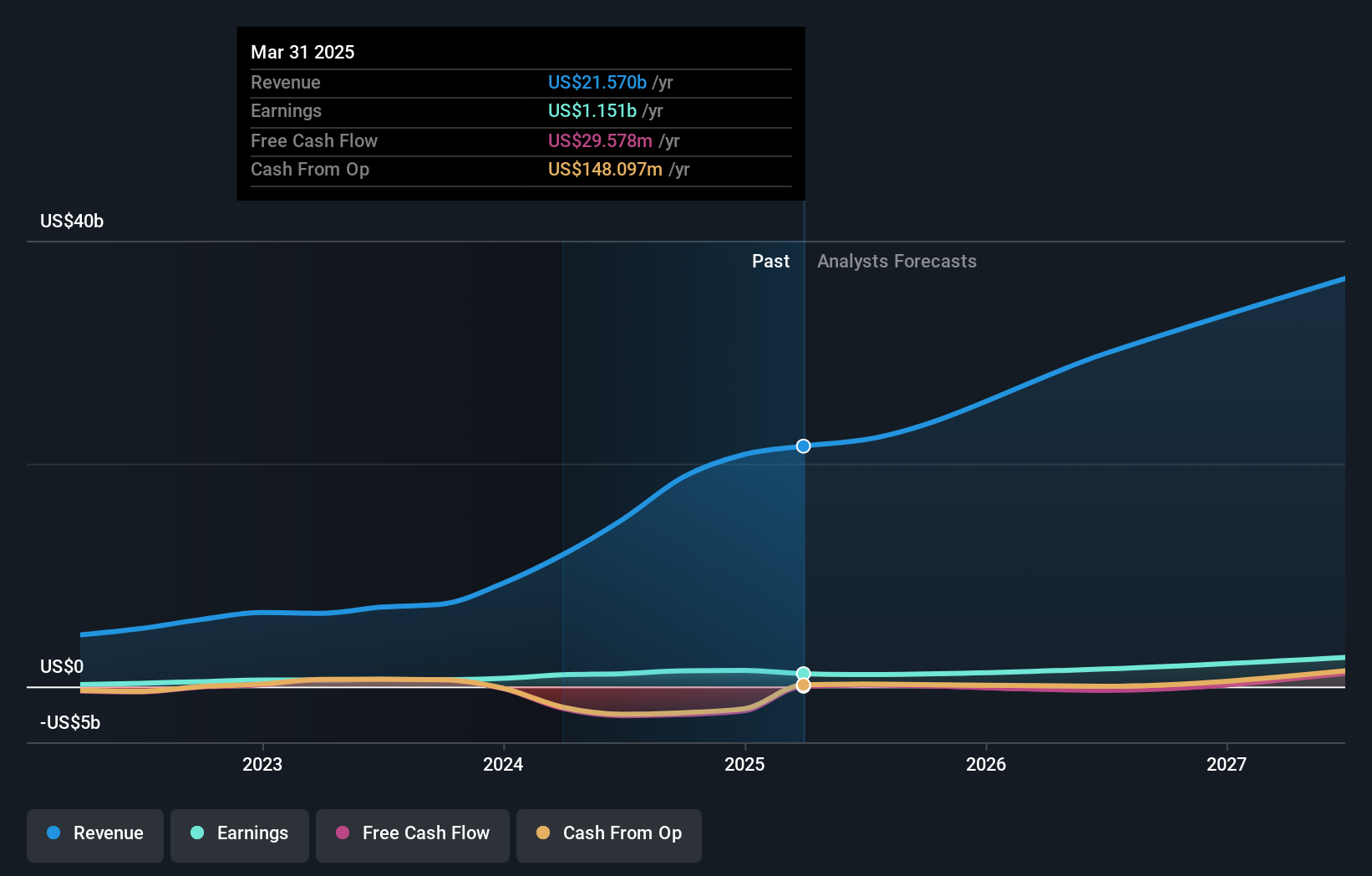

Overview: Super Micro Computer, Inc. develops and sells server and storage solutions based on modular and open-standard architecture across the United States, Asia, Europe, and internationally, with a market cap of approximately $27.72 billion.

Operations: The company’s revenue primarily comes from developing and providing high-performance server solutions, totaling approximately $33.70 billion.

Insider Ownership: 13.7%

Earnings Growth Forecast: 19.1% p.a.

Super Micro Computer, Inc. demonstrates characteristics of a growth company with high insider ownership, evidenced by its strategic collaborations and product innovations in AI infrastructure. Recent partnerships with Verda and Nano Nuclear Energy highlight its role in sustainable AI solutions. However, legal challenges regarding alleged export violations could impact investor sentiment. Despite volatility, the company’s revenue is forecast to grow significantly faster than the US market average, although profit margins have declined from last year.

Simply Wall St Growth Rating: ★★★★★☆

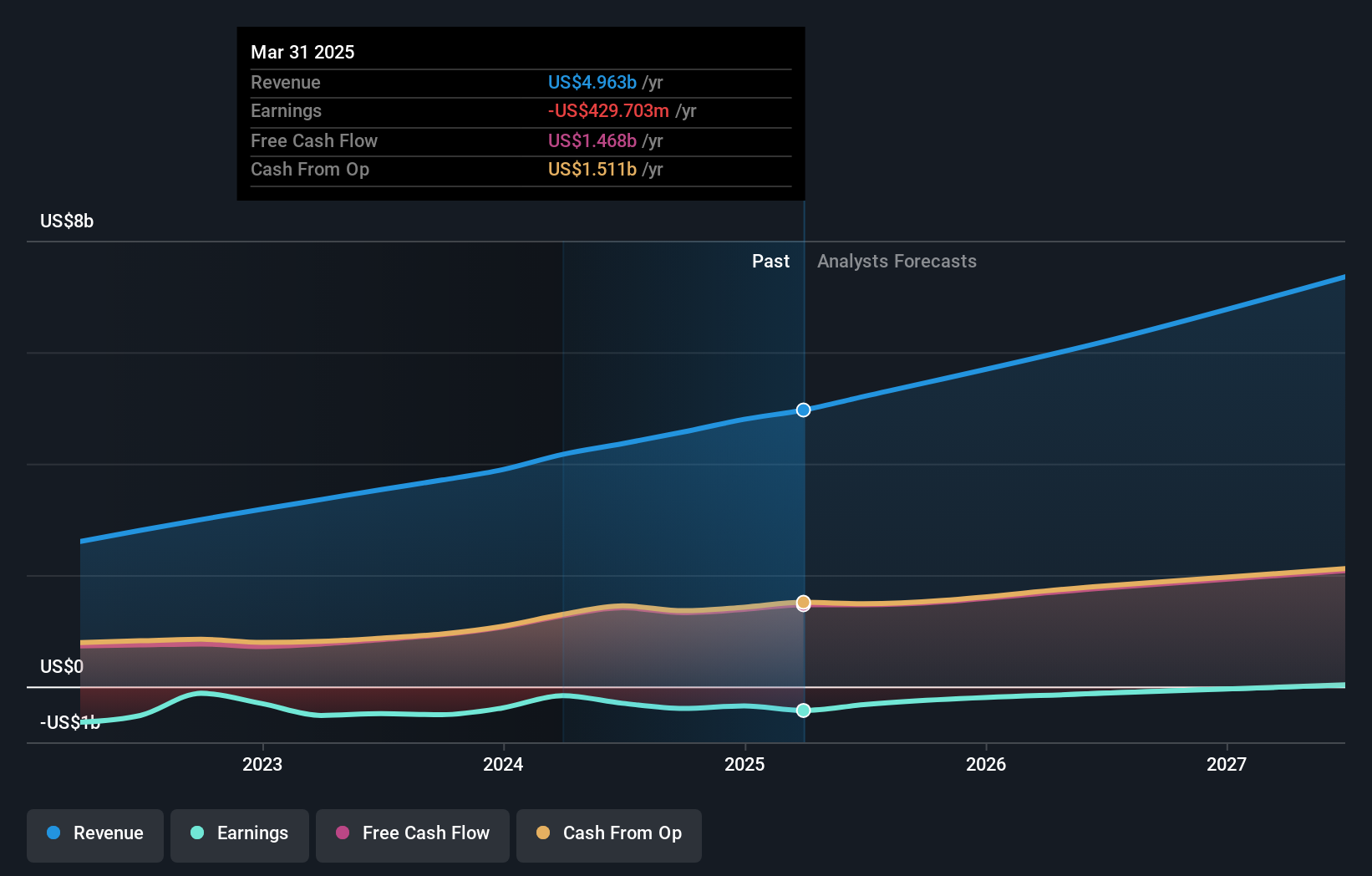

Overview: Atlassian Corporation offers collaboration software designed to enhance productivity across organizations globally, with a market cap of approximately $27.31 billion.

Operations: The company’s revenue primarily comes from its Software & Programming segment, which generated $6.19 billion.

Insider Ownership: 36.4%

Earnings Growth Forecast: 62.9% p.a.

Atlassian exemplifies growth potential with high insider ownership, driven by innovative AI-powered product offerings like Flex and Rovo. Despite a recent net loss of US$98.39 million, revenue rose to US$1.79 billion in Q3 2026 from US$1.36 billion the previous year, showcasing strong demand for its cloud platform used by over 300,000 customers including Fortune 500 companies. However, the company’s removal from the NASDAQ-100 Index may affect market perception despite its strategic advancements and partnerships with Google Cloud enhancing AI capabilities.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Sea Limited is a technology company operating through its subsidiaries in Southeast Asia, Latin America, and globally, with a market cap of $55.45 billion.

Operations: The company’s revenue is primarily derived from its E-commerce segment (Shopee) at $18.15 billion, followed by Digital Financial Services (Monee) at $4.25 billion, and Digital Entertainment (Garena) at $2.61 billion.

Insider Ownership: 14.1%

Earnings Growth Forecast: 24% p.a.

Sea Limited demonstrates significant growth potential, with recent Q1 2026 earnings showing a revenue increase to US$7.10 billion from US$4.84 billion the previous year and net income rising to US$427.94 million. Despite trading below its estimated fair value, Sea’s earnings are projected to grow significantly at 24% annually, outpacing the broader U.S. market’s forecasted growth of 17%. The completion of a share buyback program underscores management’s confidence in its future trajectory.

Summing It All Up

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders.

It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities.

All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com