IPO, early trading moves and why Apotex Health is suddenly in focus

Apotex Health (TSX:APTX) has quickly drawn investor attention after completing a roughly CA$1.5b IPO at CA$24 per share, with early trading marked by share price swings and debate over what the new listing is worth.

The offering combined a treasury sale of new shares with a secondary sale by existing holders. This structure put fresh capital on the company’s balance sheet while giving SK Capital Partners and other shareholders a chance to reduce their stakes.

Since listing, Apotex Health has seen both gains and single day declines of around 3% to 4.5%. This pattern reflects a market that is still working through competing views on growth prospects, leverage and competitive pressures.

At a recent close of CA$30.01, the stock has moved above its IPO level, and user interest has risen as investors weigh the approved IHEEZO product, balance sheet risks and the company’s mix of generic, biosimilar and branded revenues.

See our latest analysis for Apotex Health.

For context, Apotex Health’s 1 day share price return of 2.28%, 7 day share price return of 3.52% and year to date share price return of 11.15% point to building short term momentum as investors react to the IPO, IHEEZO approval and the ongoing debate around earnings strength versus balance sheet risk.

If Apotex Health has caught your attention, it can also be useful to see how other healthcare related opportunities compare. A good place to start is 6 healthcare AI stocks

So with Apotex Health trading above its CA$24 IPO price, a P/E of 17.5x, and an internal model suggesting the shares sit at a large discount to intrinsic value, is there still a buying opportunity here, or is the market already pricing in future growth?

Preferred P/E of 18.3x for Apotex Health: Is it justified?

Apotex Health is trading at a P/E of 18.3x, which sits above the North American pharmaceuticals industry average of 14.4x but below a peer average of 48.5x. This places the company between a more typical sector valuation and much higher peer multiples.

The P/E ratio compares the current share price to earnings per share and is often used for profitable companies like Apotex Health, where earnings are a key part of the story. A higher P/E can sometimes reflect expectations for stronger or more resilient earnings, while a lower P/E can indicate more muted expectations or perceived risk.

On that P/E of 18.3x, Apotex Health screens as more expensive than the wider North American pharmaceuticals industry, which trades at 14.4x. This suggests investors are willing to pay a premium relative to the broader group. However, compared with a peer average P/E of 48.5x, the stock sits well below some closely watched comparables, which points to a more conservative multiple than the highest valued peers.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-earnings of 18.3x (ABOUT RIGHT)

However, Apotex Health still faces risks related to its leverage position and competitive pressures in generics and biosimilars, which could challenge margins and investor confidence.

Find out about the key risks to this Apotex Health narrative.

Another view on Apotex Health’s value

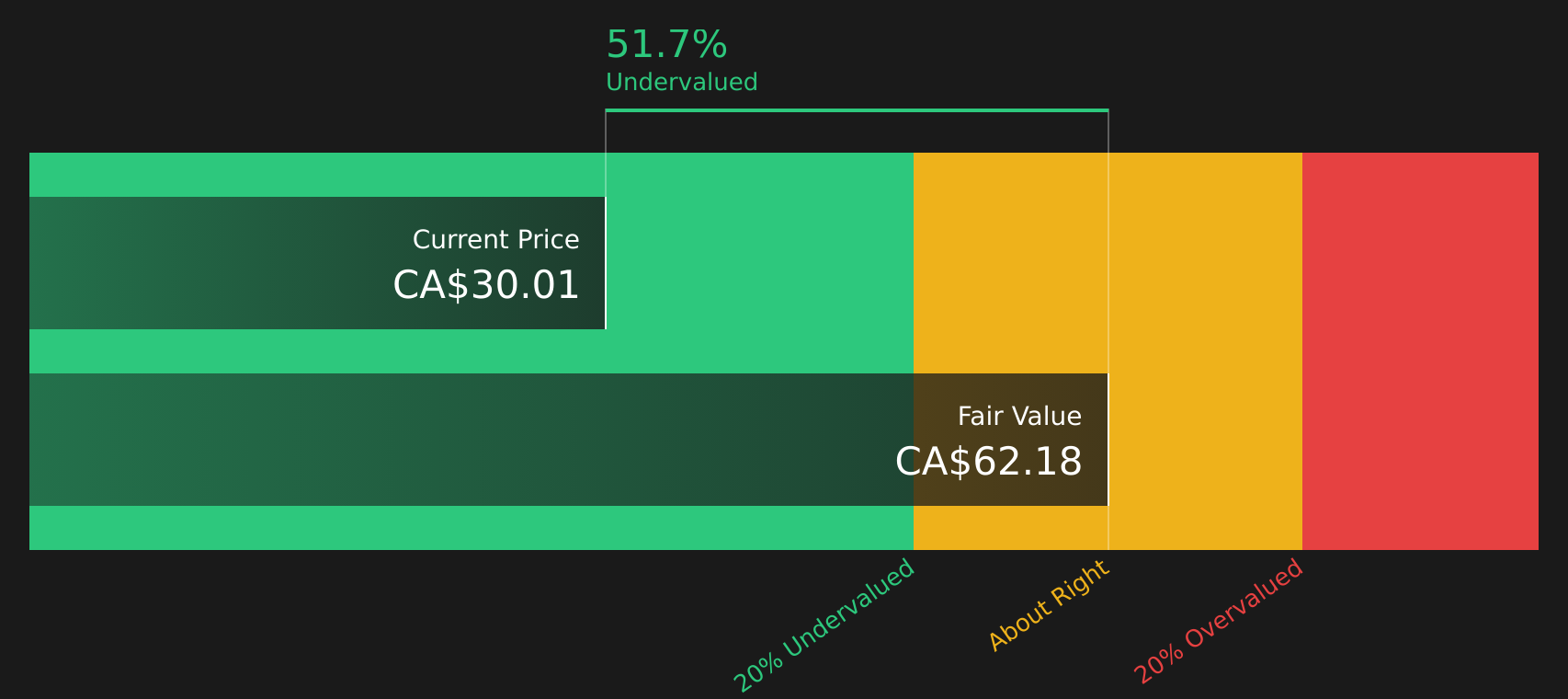

The earlier P/E comparison suggests Apotex Health sits between typical sector pricing and higher rated peers, but the SWS DCF model points in a different direction. At CA$30.01, the stock trades at a 51.7% discount to an estimated future cash flow value of CA$62.18, which raises a different question about what the market is missing.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Apotex Health for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 8 high quality undervalued stocks. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Next Steps

With mixed signals around Apotex Health’s valuation and outlook, the key is to move quickly from headline impressions to your own conclusion using the 2 key rewards and 4 important warning signs.

Looking for more investment ideas beyond Apotex Health?

If Apotex Health has sharpened your focus on where to put fresh capital, do not stop here. The right watchlist can be built before the crowd pays attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com