Global markets started H2 2026 with investors in a more cautious mood, as profit-taking hit parts of the AI trade ahead of today’s key US jobs report.

Technology stocks remained under pressure, oil extended its slide on signs of progress in US-Iran talks, and traders debated whether the pullback in chipmakers is a healthy reset or the start of a wider rotation away from high-growth stocks.

Key Themes Across Global Markets

- Technology and semiconductor stocks stay under pressure after a strong quarter

- Oil prices fall to four-month lows as US-Iran talks show progress

- US jobs report becomes the week’s main market event

- US Dollar eases while yen rebounds on intervention speculation

- Gold recovers as softer labour data cools inflation fears

- Markets question whether AI valuations have run too far

- Investors rotate into defensive sectors before fresh economic data

After one of the strongest quarters for global equities in years, markets are finally taking a breather.

The AI-led rally that powered the Nasdaq, South Korea’s KOSPI and Taiwan’s stock market to record gains has given way to profit-taking, with investors becoming more selective after months of almost uninterrupted gains.

Quarter-end rebalancing has added to the pressure, while doubts over the sustainability of AI spending have cooled sentiment across the semiconductor sector.

Technology stocks remain at the centre of the move.

Asian markets led the declines overnight after heavy selling in major chipmakers, with South Korea’s KOSPI hit as investors took profits in SK Hynix and Samsung following sharp gains during the second quarter.

That weakness also spread into US and European technology names, underlining how dependent global markets have become on the AI investment theme.

This has not been a classic growth scare.

Instead, investors are questioning whether the huge capital spending plans from hyperscale technology companies can continue at the same pace.

Microsoft, Amazon, Alphabet and other AI leaders are expected to spend heavily again this year on AI infrastructure, leaving markets increasingly focused on whether those investments will generate strong enough returns.

There are also signs that market leadership is beginning to broaden.

While technology shares have stumbled, defensive sectors such as healthcare, consumer staples and utilities have held up better in Europe, helping the STOXX 600 remain close to record highs despite weakness in AI-linked stocks.

Some strategists see that as a healthy rotation, reducing the market’s reliance on a narrow group of large technology companies.

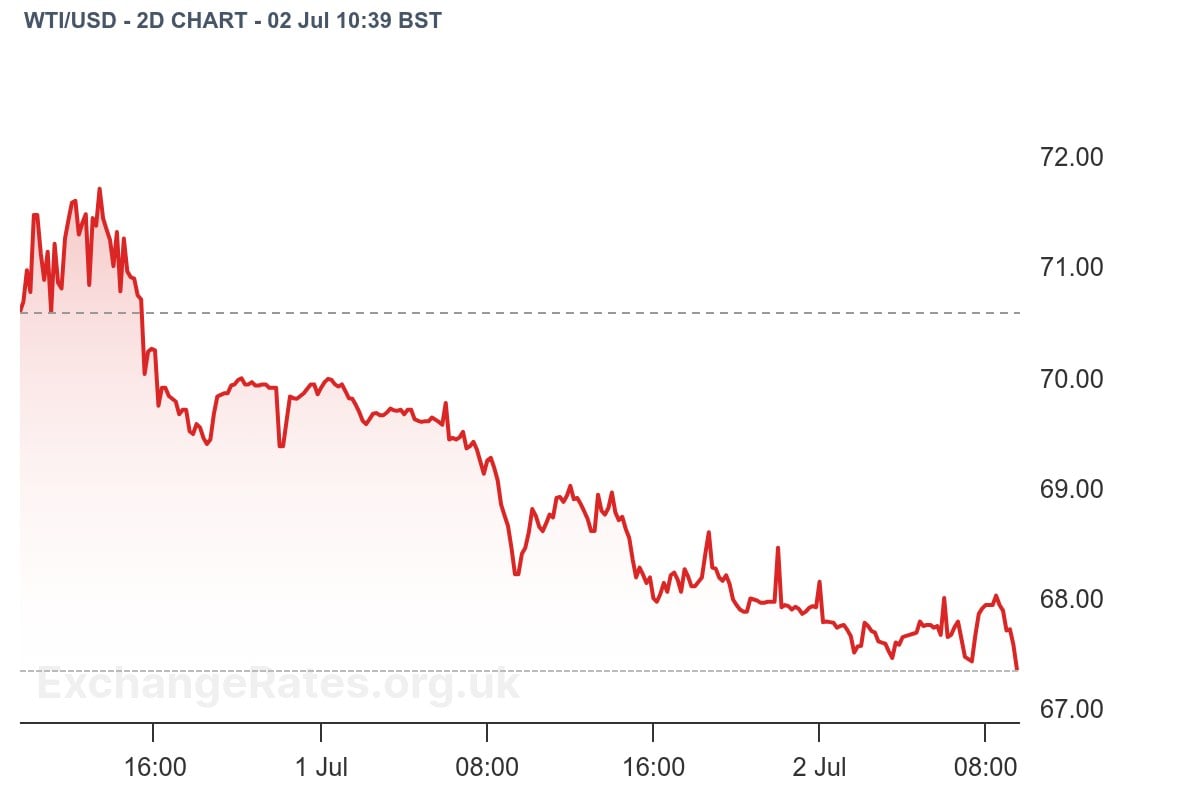

Oil markets are telling a different story.

Brent crude has fallen for three sessions in a row, touching its lowest level since late February after Qatar confirmed further progress in indirect talks between the United States and Iran.

The reopening of shipping through the Strait of Hormuz has increased available supply, while UBS has cut its Brent forecasts following the improvement in geopolitical conditions.

The drop in oil has helped ease some inflation concerns.

Lower energy costs give central banks more room to believe headline inflation can moderate through the second half of the year.

Even so, investors remain wary of ruling out further Federal Reserve tightening, especially before today’s labour market data.

Currency markets are highly sensitive to those expectations.

The US dollar has eased modestly before the payrolls report, while the Japanese yen has strengthened on renewed speculation that Tokyo could intervene again if currency weakness resumes.

The euro and sterling have also recovered slightly as traders trim defensive dollar positions before the data.

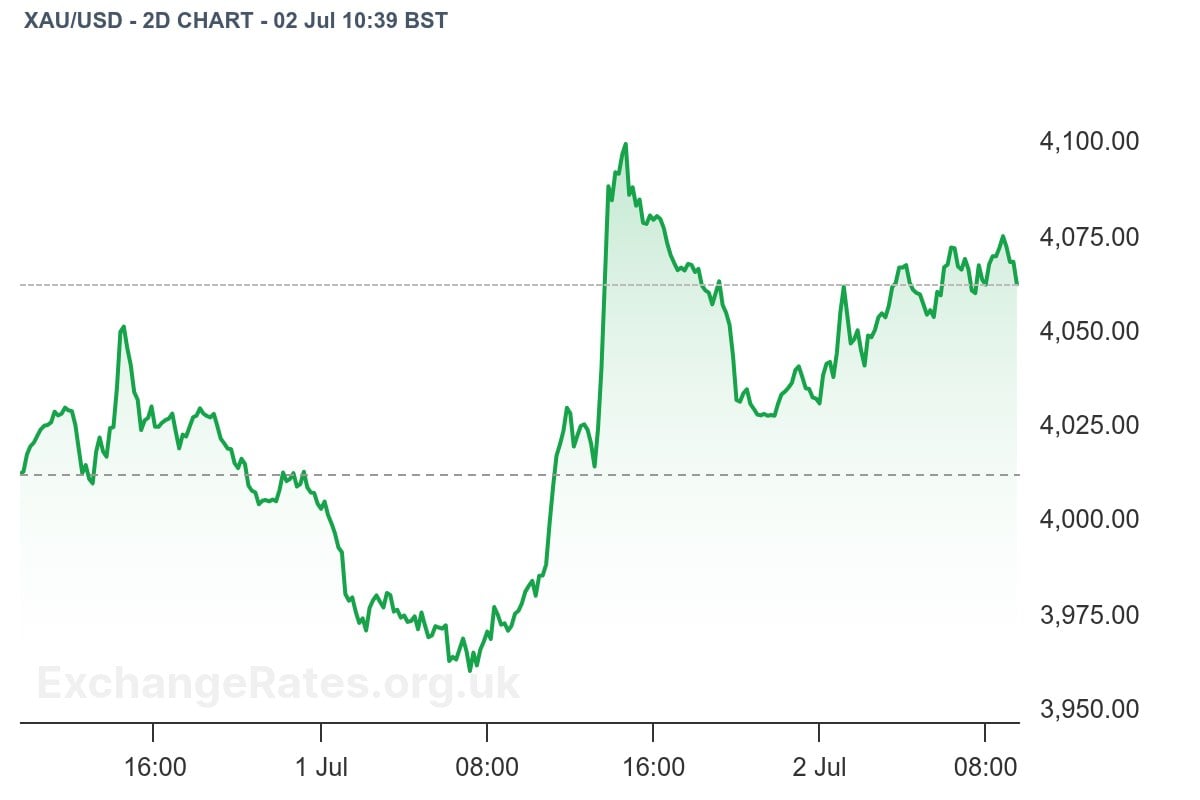

Gold has benefited from the more cautious tone.

The precious metal edged higher after weaker-than-expected US private-sector employment figures strengthened hopes that labour market momentum may be slowing.

Together with lower oil prices, the softer jobs data has taken some heat out of the inflation concerns that dominated markets in June.

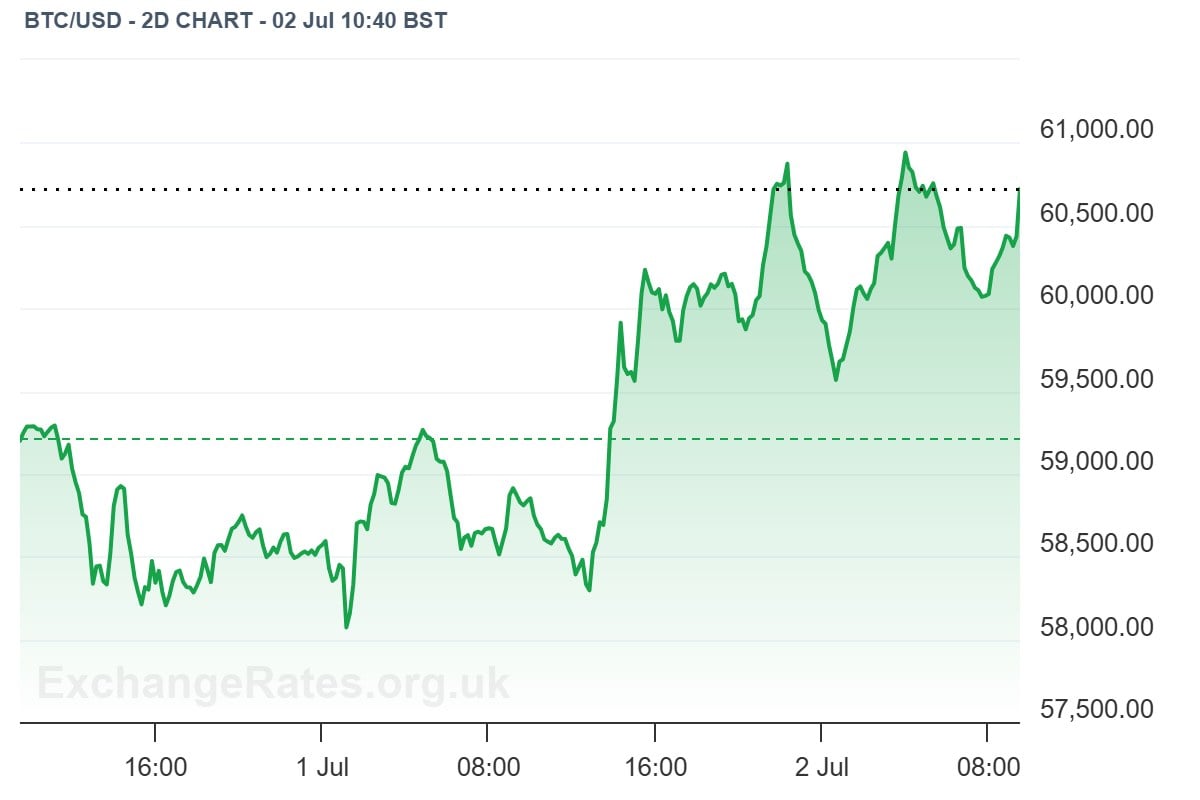

Crypto markets continue to lag.

Bitcoin remains under pressure despite the improvement in broader risk appetite, with investors still cautious toward speculative assets while the outlook for interest rates and global liquidity remains uncertain.

What Traders Are Watching

The immediate focus is today’s US non-farm payrolls report, now the week’s key macro event.

Economists expect the US economy to have added around 110,000 jobs in June, although forecasts remain unusually wide after mixed labour market signals earlier in the week.

A stronger report would reinforce expectations for another Federal Reserve rate hike, while weaker data could revive hopes that policymakers may eventually pause tightening.

Investors will also keep watching US-Iran negotiations after another round of talks in Doha produced signs of further cooperation.

A full agreement still appears some way off, but the progress so far has been enough to keep pressure on oil prices and remove one of the biggest inflation risks facing global markets.

For now, markets are entering the second half of the year with a more balanced outlook.

The AI story is still intact, but investors are becoming more demanding on valuations.

At the same time, lower oil prices are easing inflation concerns just as the US interest rate outlook reaches another critical point.

Today’s payrolls report could decide which of those narratives drives trading through the rest of July.