Savers have lost money in real terms over the past decade.

The average saver using Premium Bonds has lost money in real terms over the past decade, according to research by Fidelity. Had they invested in a global equity tracker, they could have had a cash pot worth £15,900.

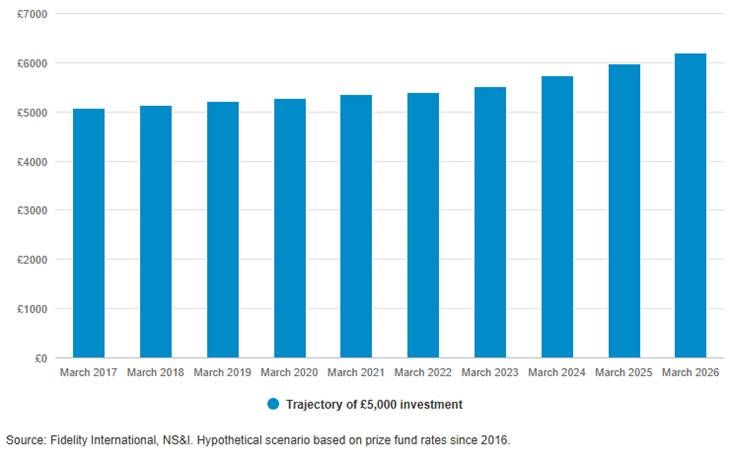

On average, £5,000 put into Premium Bonds in 2016 would now be worth £6,190 based on historic prize rates. However, inflation over this time means the initial £5,000 would have needed to grow to £6,992 to keep pace.

It is worth noting that some will have made significantly more, while others will have made significantly less, depending on the luck of the draw each month.

Average Premium Bond returns over 5yrs

Premium Bonds remain one of the UK’s most popular savings products, held by around a third of the population. Some like Premium Bonds because the money is 100% backed by the Treasury, willingly forgoing higher rates for this peace of mind.

However, it is worth noting that the Financial Services Compensation Scheme (FSCS) covers savings of up to £120,000 per person per bank or building society. The maximum that can be put into Premium Bonds is £50,000.

Others appreciate the chance to win big, with the top prize of £1m life-changing for many.

Jemma Slingo, pensions and investment specialist at Fidelity International, said: “Premium Bonds can play a useful role in a balanced financial plan. They offer capital security and tax-free prizes, making them a good option for short-term savings or an emergency fund.

“Where savers need to be careful is over longer time horizons. While your money is safe in cash terms, inflation can steadily erode its real value and returns from Premium Bonds are uncertain as they depend on prize draws. Over time, that can add up to a significant opportunity cost compared to investing.”

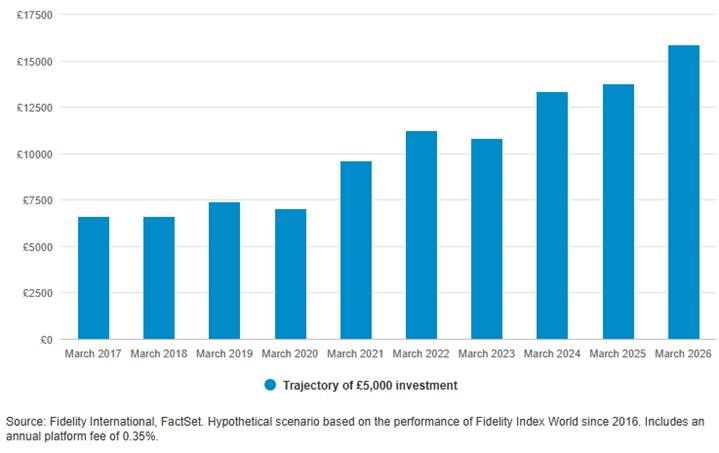

Indeed, by investing in the Fidelity Index World fund – a global equity tracker – a decade ago, the cash pot would now be worth £15,900.

Returns of fund over 5yrs

Slingo said this is particularly pertinent when investing for children, who typically have a long time before needing the money. Premium Bonds are a popular gift, but will not achieve the returns of the stock market for most.

The research comes after National Savings & Investments (NS&I) increased the number of prizes on offer, potentially drawing more savers to the product.

From July, there will be 322,000 extra prizes compared with this month’s results, including 12 additional £100,000 prizes, 24 more £50,000 prizes and an extra 49 £25,000 prizes.

This will push up the prize fund rate (think of this as the average interest on the bonds) to 3.8%, with chances of winning dropping from 23,000 to one to 22,000 to one.

Rachel Springall, finance expert at Moneyfactscompare, said savers would be “delighted” by the news, but noted that the average implied rate remains lower than some easy-access bank accounts, which currently offer 4% interest. Fixing can offer even greater interest payments of 4.5% a year or higher.

“This move from NS&I comes at a time where there are expectations for interest to stay higher for longer, so it is important that it remains in a somewhat middle ground space to offer a fair rate, but not lead the market outright,” she said.

While it is a “positive signal” that the number of prizes has increased, Springall said the implied rate of interest (3.8%) is the same as it was a year ago.

Savers should note that the rate rises and falls depending on interest rates as well as the government’s net financing targets, with more attractive rates on offer when they need to raise more cash.