Interest rates for Japan’s popular Flat 35 long-term fixed-rate mortgage rose to 3.21% in June, raising the hurdles to homeownership.

Interest Rates Rise Amid Inflation Concerns

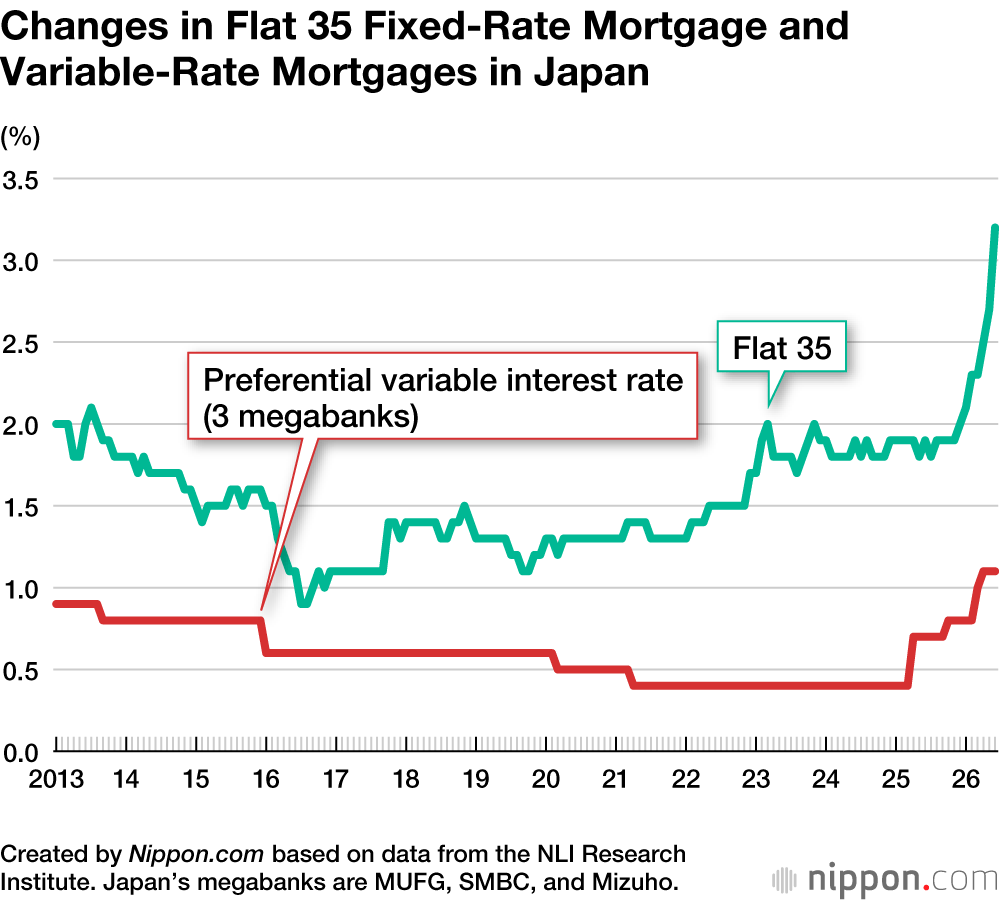

Flat 35 is a commonly used long-term fixed-rate mortgage loan in Japan with a maximum term of 35 years, offered through a partnership between private financial institutions and the Japan Housing Finance Agency. In June, the minimum interest rate for Flat 35 rose to 3.21%, surpassing the 3% level for the first time in 17 years.

The main factor behind the increase is rising inflation. Interest rates on Flat 35 are influenced by long-term interest rates, particularly the yield on 10-year Japanese government bonds. In addition to concerns about Japan’s fiscal health, markets have recently been anticipating intensified inflation due to the worsening situation in the Middle East and soaring oil prices. As a result, long-term interest rates have continued to rise.

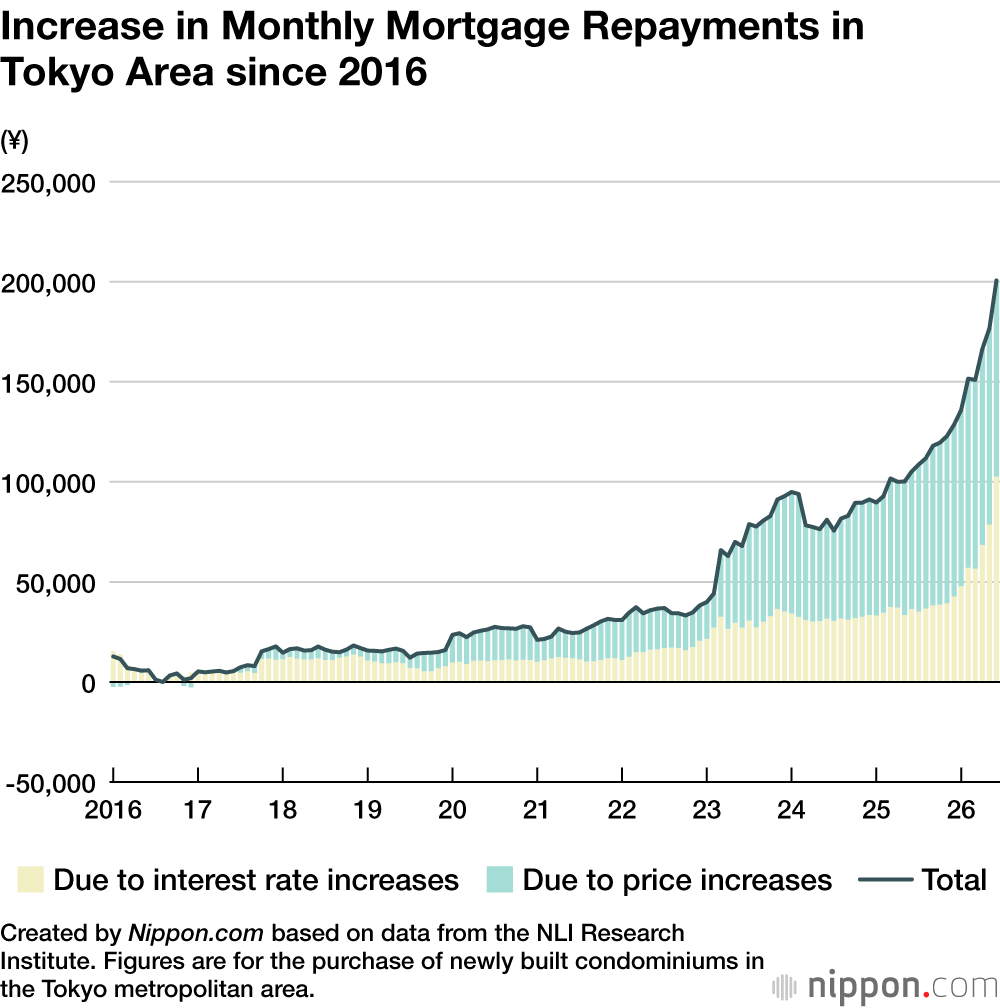

According to the NLI Research Institute, the lowest interest rate ever offered under the Flat 35 program was 0.9% in August 2016, before the system was revised the following year. Compared with that time, the average price of a newly built condominium in the Tokyo metropolitan area (based on a 12-month moving average) has risen by ¥39.2 million, reaching ¥95.9 million. Assuming a borrower finances 90% of a home price through a Flat 35 mortgage, the monthly payment would be ¥200,671 higher than in August 2016, as a result of the increase of ¥98,003 in the property price and ¥102,668 in interest rates.

In contrast to long-term fixed-rate mortgages such as Flat 35, variable-rate mortgages offered by private financial institutions remain at relatively low levels of around 1% (after preferential discounts). These rates are influenced by the Bank of Japan’s monetary policy, which is to raise the benchmark interest rate gradually. At present, variable-rate mortgages are roughly two percentage points lower than fixed-rate mortgages. About 80% of mortgage borrowers choose variable-rate mortgages.

However, Kobayashi Masahiro, a visiting researcher at the NLI Research Institute, notes that “it is difficult to know what lies ahead” with regard to short-term variable rates “now that long-term interest rates are on the rise ahead of other rates and inflation is expected to intensify, along with the uncertainty about the situation in Iran.” He adds: “If you have enough financial flexibility to withstand a rise in interest rates should it occur, a variable-rate mortgage may be a good choice. However, if you’re concerned about the possibility of rates increasing, opting for a fixed-rate mortgage to prioritize peace of mind is also an option.”

Data Sources

(Translated from Japanese. Banner image © IllustAC.)