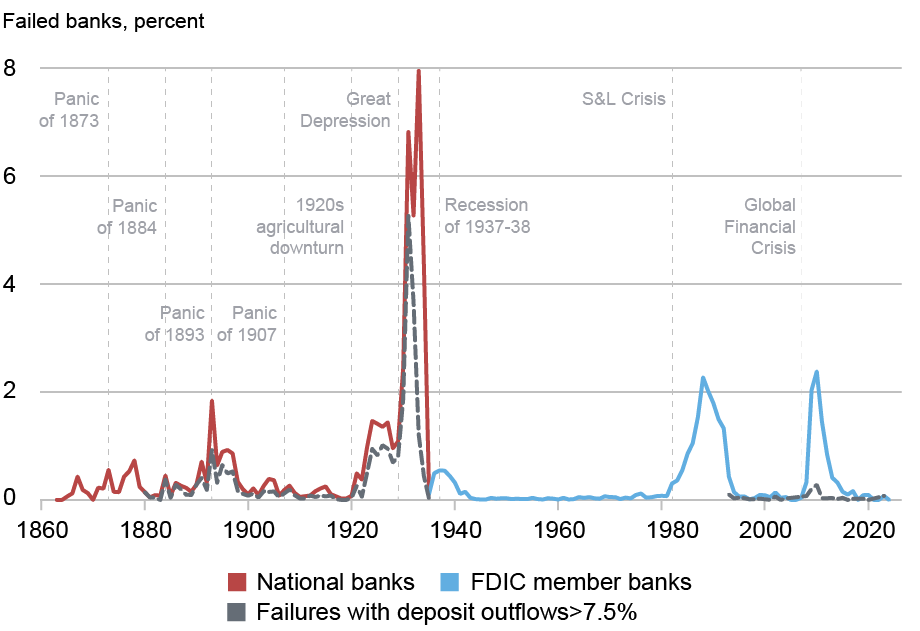

Bank Failures in the United States, 1863–2024

Bank Failures: The Theory

Bank failures can stem from two related but distinct sources. Under the liquidity view, a sudden wave of withdrawals forces a bank to liquidate assets at fire-sale discounts, rendering it insolvent. Runs can thus trigger the failure of otherwise healthy banks (Diamond and Dybvig, 1983) or of weak but still solvent banks (Goldstein and Pauzner, 2005).

Under the solvency view, losses on loans or investments erode a bank’s equity. Once bank assets are not worth enough to fully repay depositors, the bank is fundamentally insolvent. A run may then be the final trigger that forces closure. The run can determine when and how the bank fails, but it is not the root cause of the problem.

Bank Failures: The Evidence

Finding 1: Bank failures are always and everywhere related to weak bank fundamentals.

The debate over whether bank failures are caused by insolvency or illiquidity has a long history. In A Monetary History of the United States, Friedman and Schwartz (1963) argued that many bank failures during the Great Depression resulted from “self-justifying” runs on solvent banks. However, subsequent empirical work has placed more emphasis on poor economic and bank-level fundamentals. Studies using regional and bank-level data find that banks that failed during the Depression were more exposed to declining local economic conditions, were less well capitalized, held more illiquid assets, and relied more on wholesale funding than surviving banks (White 1984, Calomiris and Mason 2003).

The crucial role of poor bank fundamentals extends well beyond the Great Depression. In a recent paper, we extend these findings across 160 years of U.S. banking data, covering over 5,000 bank failures (Correia, Luck, and Verner, 2026b). Failing banks consistently exhibit declining income and capitalization, rising asset losses, and growing reliance on expensive funding in the years before failure. A common precursor to failure is rapid asset growth, usually from aggressive lending. These patterns hold for bank failures with and without runs. They also hold across institutional regimes with and without deposit insurance or a public lender of last resort. As a result, bank failures are substantially predictable based on weak bank fundamentals. More broadly, crises in which many banks fail are often a predictable consequence of deteriorating fundamentals.

Finding 2: Recovery rates suggest most, but not all, failed banks subject to runs were fundamentally insolvent.

Are most failures caused by runs on weak-but-solvent banks or on fundamentally insolvent bank? Recovery rates on failed bank assets provide new insights into this question. Before the introduction of federal deposit insurance in 1934, overall creditors recovered, on average, only 75 cents on the dollar, while unsecured depositors recovered only 66 cents on the dollar (Correia, Luck, and Verner 2026a, 2026b). This means that failed bank assets fell substantially short of covering debt claims, indicating that most failed banks were fundamentally insolvent. Runs on weak-but-solvent banks therefore accounted for only a modest share of national bank failures, unless one assumes that receivership itself destroyed substantial value. While runs were an important trigger of failure at insolvent banks, low recovery rates suggest they were less often the cause of failure for otherwise solvent banks.

Finding 3: Bank examiners emphasize poor asset quality and rarely attribute failures to runs.

What do bank examiners say about the condition of failed banks and the causes of bank failure? In the pre-deposit-insurance U.S. banking system, OCC examiners’ assessments indicate that most failed banks held assets exposed to substantial losses. On average, examiners classified only 36 percent of failed bank assets as “good,” while 47 percent were considered “doubtful” and 18 percent “worthless.”

Furthermore, U.S. bank examiners historically classified the cause of death for banks. In the OCC’s bank-specific cause-of-failure reports, the most common causes were poor local economic conditions, asset losses, and fraud. Runs and liquidity issues were cited in fewer than 20 out of over 2,000 cases.

The Great Depression is a partial exception. Federal Reserve Board’s classifications of Depression-era suspensions suggest that liquidity issues played a larger role than in other periods (Richardson 2007). But even then, examiners’ assessments remained pessimistic about asset quality. As a 1936 Federal Reserve report put it, “In our long, failure-studded history of banking, most of the institutions which suspended business were subsequently proved to be insolvent.”

Finding 4: Strong banks usually survive runs through various mechanisms, including interbank cooperation, suspension, and examination.

Why don’t runs cause solvent banks to fail? Part of the answer is that runs are more common at weak banks. But strong banks do sometimes experience runs (Correia, Luck, and Verner 2026c). These runs rarely lead to failure because strong banks can employ several mechanisms to avoid costly failure.

First, in some cases, owners would provide cash to credibly signal confidence in their bank, much like how George Bailey stops the run in It’s a Wonderful Life. Second, interbank lending can provide needed liquidity, as banks are often better informed about a peer’s true condition (Blickle, Brunnermeier, and Luck 2024). Third, in the historical U.S. banking system, clearinghouses acted as quasi-central banks, issuing loan certificates to provide liquidity. Finally, during severe runs, banks would temporarily suspend convertibility, both to cool panics and to allow examiners to audit their financial statements and assess solvency. Together, these mechanisms reduce the scope for runs to force healthy banks into costly failure.

Policy Implications

The finding that most bank failures stem from solvency problems has important implications for financial stability policy.

Deposit insurance, introduced at the federal level with the creation of the FDIC in 1933, sharply reduced failures with runs. However, because pre-FDIC failures were rarely caused by runs on healthy banks, deposit insurance has not eradicated waves of bank failures altogether. What it did change was the way banks fail. In the absence of depositor discipline, bank failure is now more often the result of supervisory interventions (Correia, Luck, and Verner 2025). This framework reduces the occurrence of potentially costly runs, but it also reduces the ex post discipline that runs impose on insolvent banks. Without this discipline, there is more onus on supervisors to identify potential insolvent banks and then to mitigate the associated losses over time.

Lender-of-last-resort policy can also help solvent banks survive panics. A natural experiment from the Depression, comparing the Atlanta Fed’s generous lending with the St. Louis Fed’s more restrictive approach, shows that liquidity support can reduce failures (Richardson and Troost, 2009). But liquidity provision cannot fix insolvency. International evidence shows that even banking distress without bank runs can produce severe contractions in credit and output (Baron, Verner, and Xiong, 2021). Likewise, targeted liquidity interventions in the 21st century have never resolved bank distress on their own; balance-sheet restructuring was always required (Kelly et al., 2025).

If most bank failures are ultimately driven by insolvency, then higher equity capital plays a key role in making the banking system more resilient (Admati and Hellwig 2014). Better capitalization reduces both the likelihood of failure and the scope for runs to cause damage. Effective supervision also plays a central role by ensuring that banks recognize losses and by identifying when recapitalization is needed. In crises rooted in weak solvency, recapitalization is arguably the most effective way to restore confidence in the banking system.

Summing Up

The long-run evidence on bank failures points in one direction: Bank failures usually begin with bad assets, weak earnings, and deteriorating solvency. Runs can accelerate failure and worsen the damage, but by the time depositors head for the exit, the deeper problem is usually baked into bank balance sheets. History has shown that ensuring banks are funded with adequate capital and avoiding reckless lending booms are the most reliable ways to prevent failures from reaching that stage.

Sergio Correia is a senior economist at the Federal Reserve Bank of Richmond.

Stephan Luck is a financial research advisor in the Federal Reserve Bank of New York’s Research and Statistics Group.

Emil Verner is the Lemelson Professor of Management and Financial Economics and a professor of finance at MIT Sloan School of Management.