Broader equity markets have shrugged off geopolitical upheavals in recent months as they continue to benefit from a strong global economic backdrop, fueled by robust growth, policy support, lower US interest rates, and a weakening dollar. Our researchers expect that those key supports will remain in place for the foreseeable future and drive equity returns higher.

At the same time, 2025 marked a pivotal shift for stocks. Since the GFC, US equities and technology stocks had consistently outperformed other sectors: Low inflation meant nominal GDP, wages, and returns on physical assets were very poor.

But last year, the sources of returns broadened as major markets outside the US performed better. Technology remained strong, while many old economy sectors performed just as well.

“The strong returns at the index level, and the wider geographical participation, conceal significant rotations unfolding within equity markets,” writes Peter Oppenheimer, chief global equity strategist, in the team’s report. “The most dramatic shifts reflect investors’ evolving assessment of AI’s potential winners and losers.”

Last year, “value stocks began to stage a recovery, particularly outside the US, highlighting the renewed benefits of diversification across geography, sector, and factor, a trend that has continued into the current year,” Oppenheimer writes in the team’s report.

Are hyperscalers overspending on AI?

Oppenheimer points out that the market’s reactions to AI developments mirror past technology revolutions. Rapid innovation attracts significant investor capital, driving up the valuations of any company deemed to be associated with the innovation. After this initial period of excitement, a combination of new competition and lower returns (or both) tend to deflate valuations and increase the gap between relative winners and losers.

In the case of AI, the surge in capital spending by hyperscalers—the group of tech companies with the size and resources to deploy AI infrastructure at scale—has “prompted investors to question their ability to collectively generate adequate returns on investment,” Oppenheimer writes.

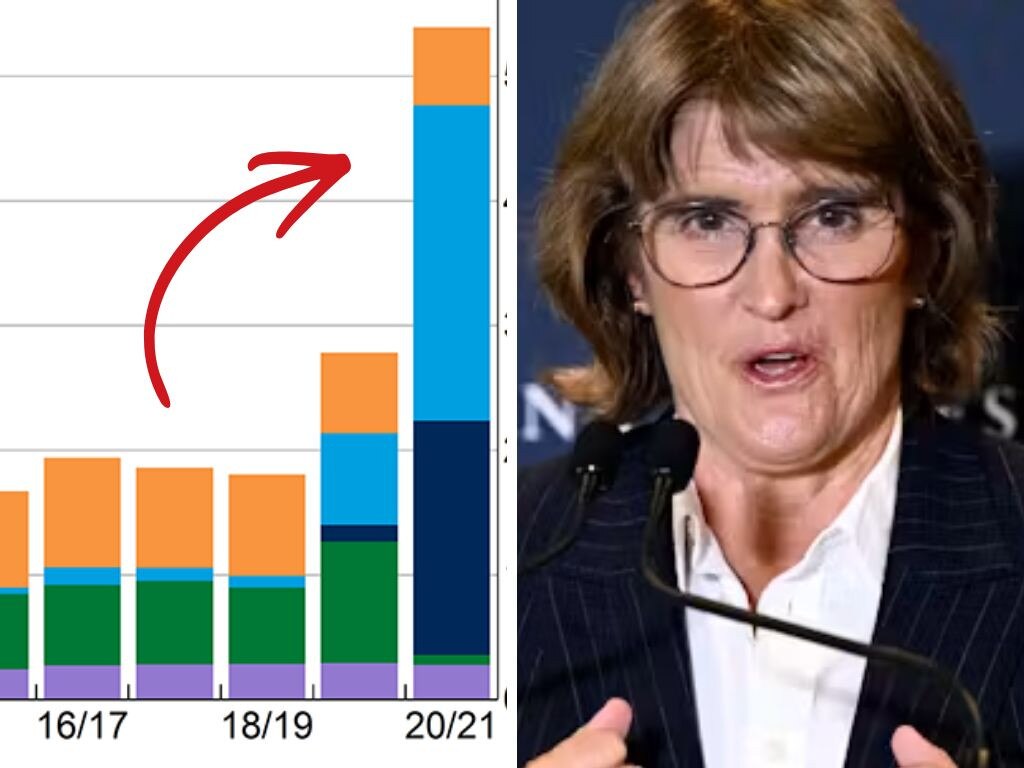

That reassessment of the group’s prospects has caused the pace of their performance to slow and the dispersion of returns within the technology sector to widen. Returns posted by the Magnificent 7 technology stocks jumped 75% in 2023 before moderating to around 50% in 2024 and less than 25% in 2025. The individual stocks within the group have since become less correlated to each other.

Are AI stocks still a good investment?

Much like the internet’s commercialization a quarter of a century ago, investors are focusing once again on the links between virtual and physical worlds. AI’s future growth prospects are increasingly dependent on physical assets like data centers and energy supplies.

“As hyperscaler capex has surged, it has spilled over into higher capex in other industries that are building the foundational infrastructure upon which the dominant tech giants’ future growth depends,” Oppenheimer writes.