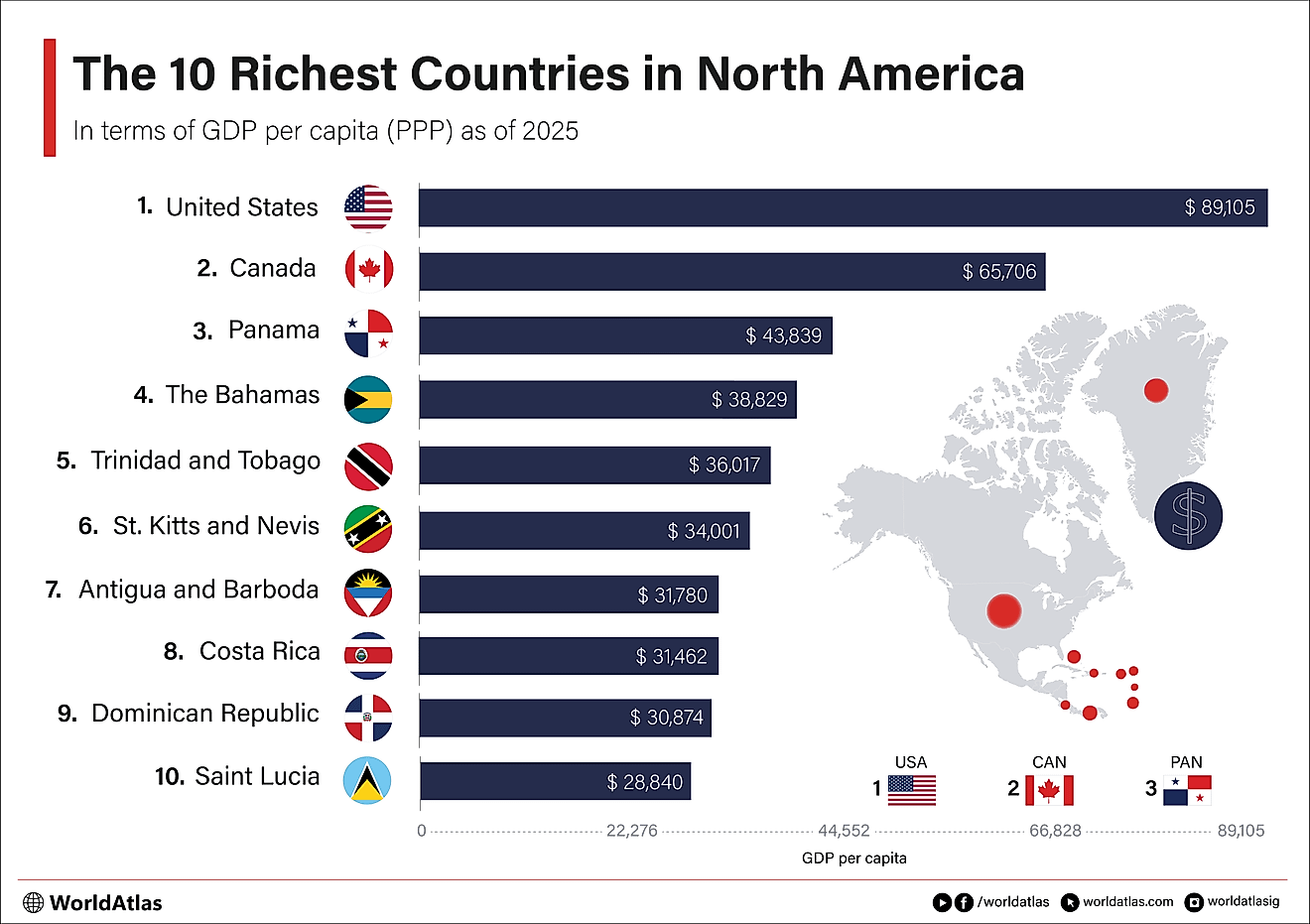

India’s core industrial sector shrank by 0.4% in March 2026, ending a period of moderate expansion in fiscal year 2025-26. This downturn highlights mixed economic momentum. The decline was driven by lower output in key energy and industrial input sectors, contrasting with continued strength in construction and infrastructure.

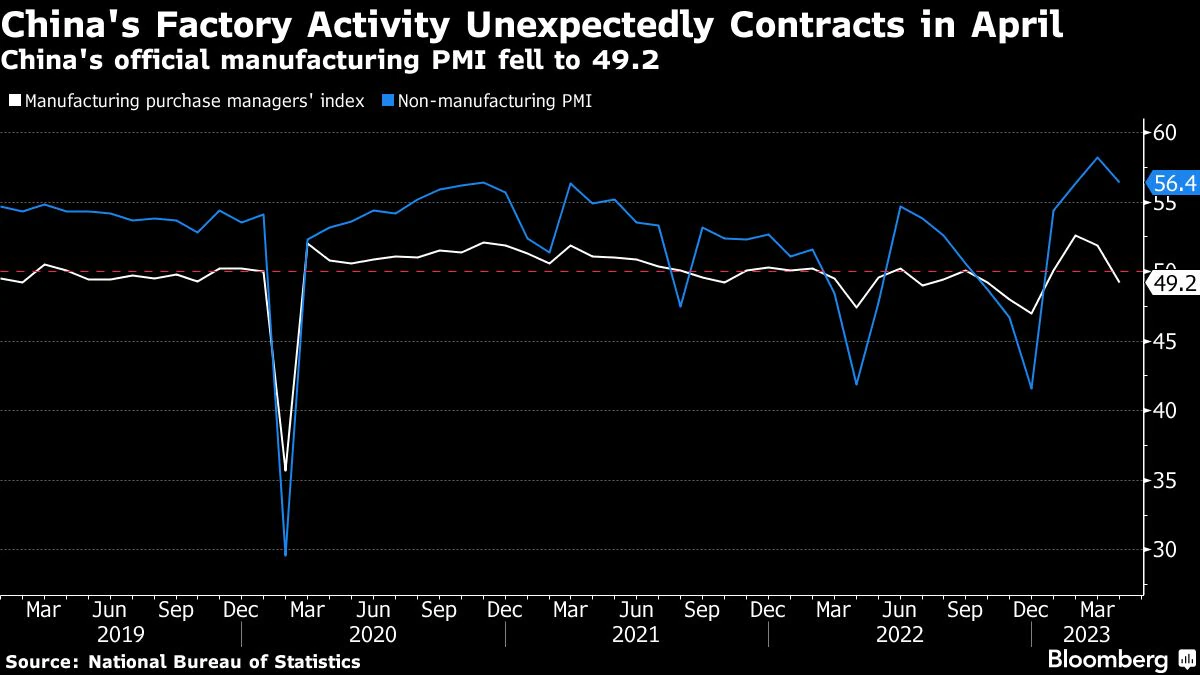

India’s Index of Eight Core Industries contracted by 0.4% in March 2026. This marked a reversal after positive growth in earlier months of the fiscal year. The downturn was largely due to sharp drops in crude oil (-5.7%), coal (-4%), and electricity generation (-0.5%). The fertiliser sector saw the steepest fall, down 24.6%. For comparison, the core sector grew by 3.7% in December 2025, 4.0% in January 2026, and 2.3% in February 2026. The full fiscal year 2025-26 closed with 2.6% growth.

Despite the broad weakness in energy, sectors linked to infrastructure and construction showed resilience. Steel output grew 2.2% and cement production rose 4.0% in March. Natural gas output also increased by 6.4%. This mixed performance shows strong demand for building materials and infrastructure projects, while energy and manufacturing inputs faced pressure.

India’s core sector contraction differs from China, which reported 5.7% industrial production growth in March 2026. Historically, India’s core sector growth has been volatile, including a dip to a 20-month low of 4% in June 2024. The recent performance suggests a return to more variable trends after steady positive growth through much of fiscal year 2026. The cumulative growth for April-March 2025-26 was 2.6%.

This uneven industrial performance comes at a key time for the Reserve Bank of India (RBI). In its April 2026 policy meeting, the central bank kept the repo rate at 5.25%, showing a cautious stance due to global uncertainties, including the West Asia conflict’s impact on oil prices and currency. The RBI raised its GDP growth forecast for FY2025/26 to 7.6% but warned of inflation risks from high energy costs and supply chain issues. The core sector contraction makes it harder for the RBI to support growth without increasing inflation.

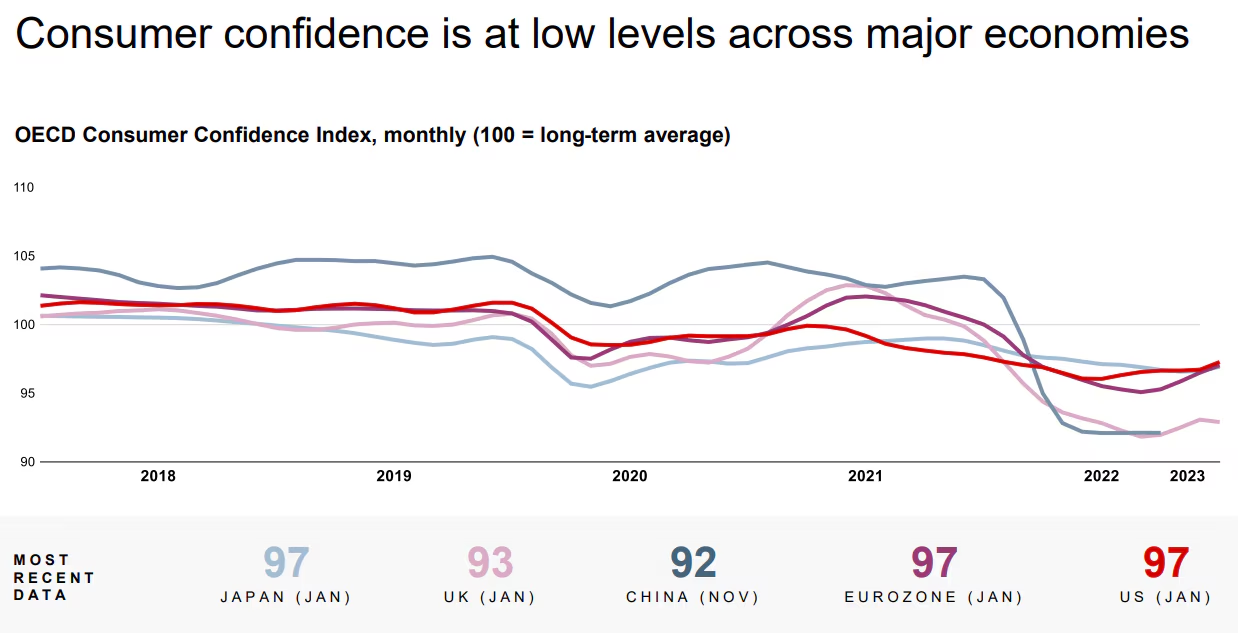

Analysts are divided. Some see India’s economy as resilient but acknowledge slowing momentum because higher commodity prices are affecting spending and company profits. They also note high valuations and less exposure to AI trends compared to China, leading to a cautious outlook on stocks. Others expect government support to boost earnings, with infrastructure growth set to continue due to public investment.

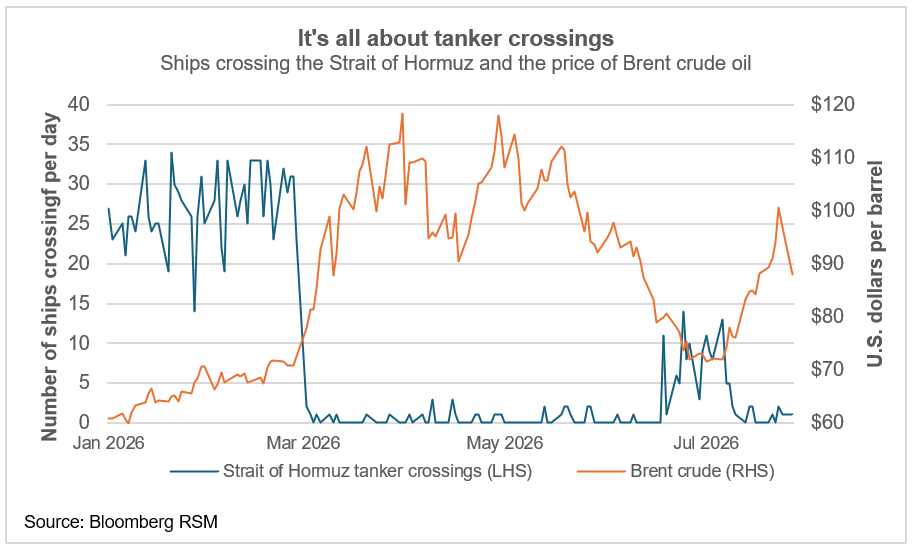

The March contraction, especially in energy sectors, reveals structural weaknesses. India’s 85% dependence on imported crude oil makes it very vulnerable to geopolitical events like the West Asia conflict. The sharp fall in fertiliser output also risks impacting the crucial agricultural sector. This uneven growth pattern makes policy decisions difficult for the RBI. The central bank must balance supporting economic activity without worsening inflation, particularly with volatile energy prices. Government actions like duty cuts on fuel ease short-term price pain but can reduce tax revenue. Analysts warn that while GDP growth is projected to remain strong, its pace is slowing. Higher commodity prices are expected to reduce consumer spending and company profits, potentially weakening overall momentum.

While India’s core sector contracted, China’s industrial production grew strongly. This suggests India might be losing competitiveness in global industry, especially in energy-intensive areas. Its reliance on imported energy, combined with supply chain issues and geopolitical tensions, fuels inflation. This can hurt consumer spending and company profits. The drop in fertiliser production could also affect crop yields and food prices, worsening inflation concerns.

Despite the March contraction, India’s industrial sector outlook is cautiously optimistic, depending on infrastructure development and policy support. FY2025-26 GDP growth is forecast around 7.6%, though momentum may slow. The infrastructure sector is expected to lead growth, backed by government spending and favorable policies. Analysts predict mid-teen earnings growth for Indian stocks in 2026, with domestic and consumer sectors likely to perform well. However, high stock valuations and global commodity price volatility remain concerns for corporate profits and consumer demand. The RBI’s balancing act between growth and inflation will be key. The path ahead involves recalibration, with infrastructure showing promise while energy sectors face scrutiny.

Disclaimer:This content is for educational and informational purposes only and does not constitute investment, financial, or trading advice, nor a recommendation to buy or sell any securities. Readers should consult a SEBI-registered advisor before making investment decisions, as markets involve risk and past performance does not guarantee future results. The publisher and authors accept no liability for any losses. Some content may be AI-generated and may contain errors; accuracy and completeness are not guaranteed. Views expressed do not reflect the publication’s editorial stance.