Since October of last year, technology or new economy shares are down 5-10%, while old economy shares like energy, metals, and mining are up 30-50%.

We called this rotation out of the ‘new’ and into the ‘old’ the ‘revenge of the old economy’ when we first observed it in 2001/02 during the dotcom collapse. It is easy to draw similar parallels to the dotcom era where AI is Web 1.0 (Microsoft), hyperscalers building datacenters are telecoms (WorldCom) laying broadband and gas and power (Enron) were expected bottlenecks. In fact, today’s mantra “own the AI compute, own the value”, sounds eerily similar to “own the network, own the value,” as the common wisdom in 2001 was to own the telecoms.

This simple comparison, however, stops there and misses a very deep difference between 2001 and 2026. This time the winners of Web 1.0 – Microsoft, Google, and Amazon – are vertically integrating and going upstream by morphing into old economy, big capex companies to own datacenters. This suggests, as we have argued in the past (2025 and 2023), a better description of this rotation is not old versus new economy but rather asset-heavy versus asset-light. We don’t want to downplay the structural productivity shock that AI represents and the impact it has had on sectors such as SaaS. Our key point here is asset-heavy sectors of which the hyperscalers are now joining with current levels of physical capex are creating a new twist to an old story.

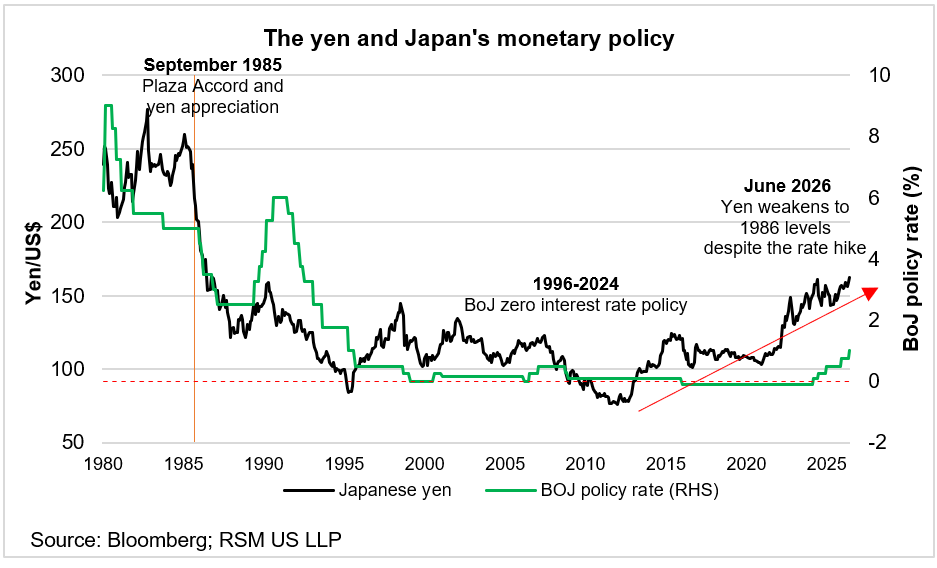

In fact, if we strip out the technology companies that are directly tied to AI, what we find is that this rotation started in late 2022 when interest rates first started to rise in response to rising commodity prices which historically was the normal catalyst for the ‘revenge of the old economy’ rotation (see Figure 1). ChatGPT’s introduction in November 2022 simply masked and delayed a process that was already underway. Now that the AI hype is fading, the rotation is just becoming more visible once again.

Figure 1: The old economy revenge resumes as the AI hype fades

Early innings of a global capex cycle

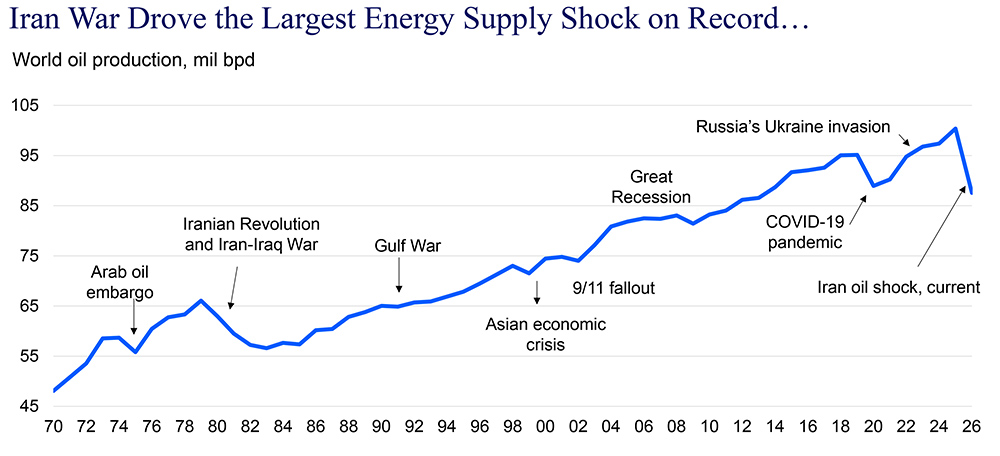

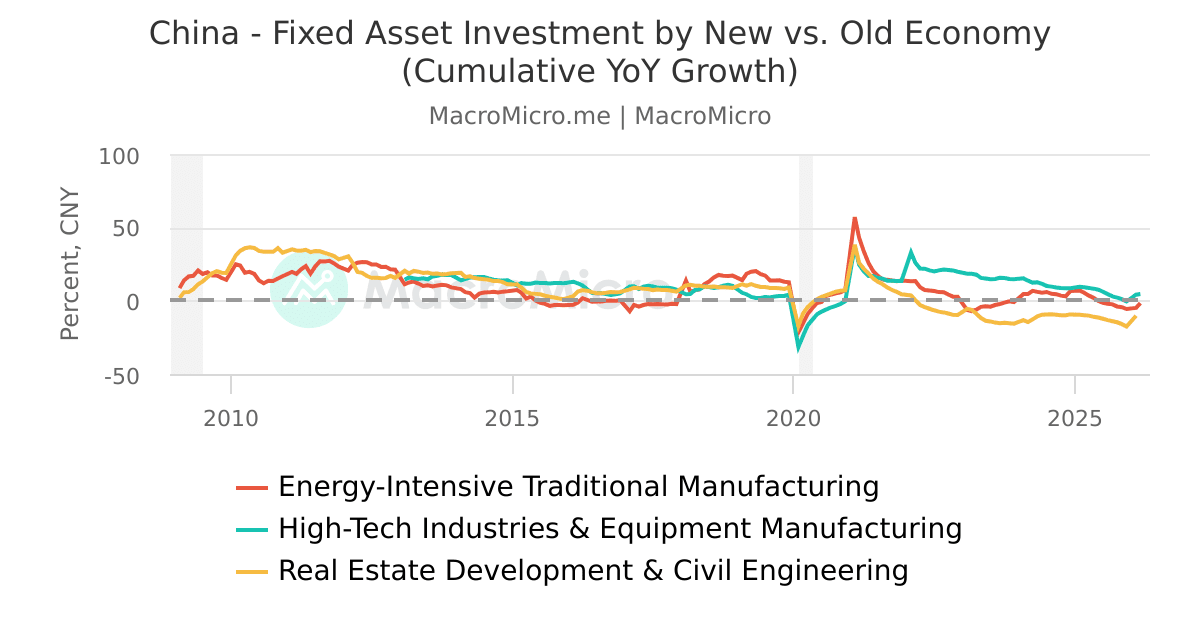

Whether you want to call it an ‘old economy’ or ‘asset-heavy’ boom or even a ‘commodity super-cycle’ in the end it is simply a capex cycle in which physical constraints on growth create physical pricing pressures (see Figure 2). It’s no coincidence that the last two commodity super-cycles corresponded nearly precisely to the two largest global capex cycles of the last 70 years. We continue to believe we are in the early stages of a decade long physical capex super-cycle driven by electrification, deglobalization requiring new and deeper supply chains, defense spending and replacing aging infrastructure. These were all the same drivers behind the commodity super-cycle call introduced in October 2020.

Figure 2: Physical capital and pricing pressures erode tech free cashflow

The only new factor is AI datacenter demand which simply offsets some of the lost decarbonization demand which is now called electrification demand instead of decarbonization. Nonetheless, regions like Europe and China are installing renewables and nuclear generation capacity at a record pace as the AI race is ultimately a power generation race. Decarbonization, security or an AI race, the motivation doesn’t matter, the fact is that this demand for physical capital continues to gain momentum. Further, the rest of the arguments from 2020 are substantially stronger today with European commitment on defense spending approaching 5% of GDP. Accordingly, copper topped $14,000/mt last month with the metals and mining sector up 50% since last autumn.

The inflation-duration trade-off

Given the capacity constraints many commodity markets face today, which are made worse by the “weaponization” of the periodic table, as the global economy grinds against physical constraints and prices rise, the need for physical capital over financial capital leads to higher interest rates, creating an inflation-duration trade-off. In other words, when physical capacity is plentiful, inflation is low and stable (1960s, 1990s, 2010s), which allows for the lower interest rates that create a pathway for long-term growth. As the cost of capital falls and investors expand their horizons, they become more focused on duration and longer-term growth opportunities.

As longer duration financial returns become more attractive than physical ones, capital is redirected into the financial economy, i.e. the Nifty Fifty, Dot-com Boom and FAANG/Mag Seven Boom. Note that these were all ‘asset-light’ booms. The Nifty Fifty was about brands like Coca-Cola or McDonalds that were asset-light scalable franchises in the same way that Microsoft software was in the 1990s or Google was in the 2010s. Eventually, however, demand catches up to physical capacity constraints, creating better returns in the physical economy than the financial economy, motivating the redirection of capital back into the physical economy, i.e. 1968-1980 and 2002-2014. The higher cost of capital simply reflects the better returns in the physical economy and the need to attract capex to expand production capacity, which is where we are today.

While this situation is not inherently inflationary, the system becomes vulnerable to demand shocks – LBJ’s Great Society in the 1960s, China’s admission to the WTO in the 2000s, or COVID stimulus in the 2020s. Note that 2026 is shaping up to be a global fiscal policy bonanza with the US, China, Germany and Japan all expected to significantly increase fiscal spending. Commodity prices rise, generating inflationary pressures, higher interest rates and higher old economy free cash flow – just as we are seeing today. These higher free cash flows and falling duration preference stimulate a new capex cycle as investors return to favor short-duration old economy, asset-heavy companies.

Yet this cycle is likely to be far more disorderly and prolonged as the rise of state capitalism and policy uncertainty around what the state will sponsor (like green versus brown energy) creates friction in the capital flows needed to stimulate the next round of investment at the same time energy-intensive AI investment will favor commodities over labor. While we have been warning of this coming shift, macroeconomic trends take time to emerge in the data and once established can last until an alternative catalyst – higher investment and demand debottlenecking – occurs. Therefore, this is likely just the bottom of the first inning in this repricing of real assets that are needed to expand physical production capacity in a fracturing global economy, suggesting a new duration cycle is likely a decade or more away.

Commodity super-cycles as sequential price spikes

At its core, the substantial rise in interest rates is the result of demand growth exceeding the economy’s ability to supply key goods, particularly commodities. Higher rates work to rectify this imbalance, increasing the returns associated with physical capital as opposed to financial capital. This pattern of global growth hitting commodity supply constraints, generating price spikes that rebalance markets until growth resurfaces is nothing new – this pattern played out in the 1970s and 2000s.

As we often say, commodity super-cycles are a sequence of price spikes, with each high and low higher than the previous spike. Unlike financial markets that average out the growth in forward earnings over time, commodity markets must balance supply and demand over a shorter horizon. Look at the outperformance of the energy equities over the oil price in 2025. When traditional buffers—inventories and spare capacity—are depleted, prices spike to generate demand destruction. But when prices fall again, as they did in precious metals last month, it doesn’t mean that the problem has been solved. It simply means that demand, due to the sharp rise in prices has temporarily fallen back away from the supply constraints. Once demand stabilizes and recovers, it just tees up the next price spike until investment finally solves the long-term supply issues.

The strategic advantage of being asset-heavy

If the ‘asset-heavy’ super-cycles of the 1970s and 2000s were all about physical assets from natural resources (call it ‘atoms’ as in the periodic table), and the ‘asset-light’ super-cycles of the 1990s and 2010s were all about technology assets from innovation (call it ‘bits’ as in memory bytes), then the 2020s are shaping up to be a decade where the bits converge with the atoms, creating new ‘bit-atom’ commodities like cryptocurrencies and AI compute. Ultimately, Bitcoin is ‘mined’ by burning vast amounts of electricity from coal, gas and other atoms to create a bit-atom commodity we call cryptocurrency. Nowhere else is this convergence between bits and atoms greater than with the hyperscalers that are trying to put steel and copper into the ground as if they were asset-heavy natural resource companies. While this would suggest that they should get rerated like a commodity producer as we argued last year, it turns out being an asset-heavy commodity producer is a good thing; they are up 30% in line with energy since October of last year (see Figure 3).

Figure 3: Bits (New Economy) are now linked to atoms (Old Economy) via AI compute

Economic and market views and forecasts reflect our judgment as of the date of this presentation and are subject to change without notice. In particular, forecasts are estimated, based on assumptions, and may change materially as economic and market conditions change. The Carlyle Group has no obligation to provide updates or changes to these forecasts. Certain information contained herein has been obtained from sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such information is believed to be reliable for the purpose used herein, The Carlyle Group and its affiliates assume no responsibility for the accuracy, completeness or fairness of such information. References to particular portfolio companies are not intended as, and should not be construed as, recommendations for any particular company, investment, or security. The investments described herein were not made by a single investment fund or other product and do not represent all of the investments purchased or sold by any fund or product. This material should not be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. We are not soliciting any action based on this material. It is for the general information of clients of The Carlyle Group. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors.

Insights & Trends>Macroeconomic InsightsPeople, Platform & Purpose>Firm DifferentiatorsPeople, Platform & Purpose>Internal Leadership, Talent & Expertise