China’s Economic Transformation and Resource Market Implications

Global commodity markets stand at an inflection point as structural forces reshape demand patterns across traditional and emerging sectors. The intersection of technological advancement, demographic shifts, and policy realignments creates both unprecedented opportunities and significant risks for resource-dependent economies. Understanding how the China economy impact on ASX mining stocks unfolds becomes essential for navigating the complex landscape facing investors in commodity-exposed assets.

When big ASX news breaks, our subscribers know first

The Great Economic Realignment: China’s Structural Transformation

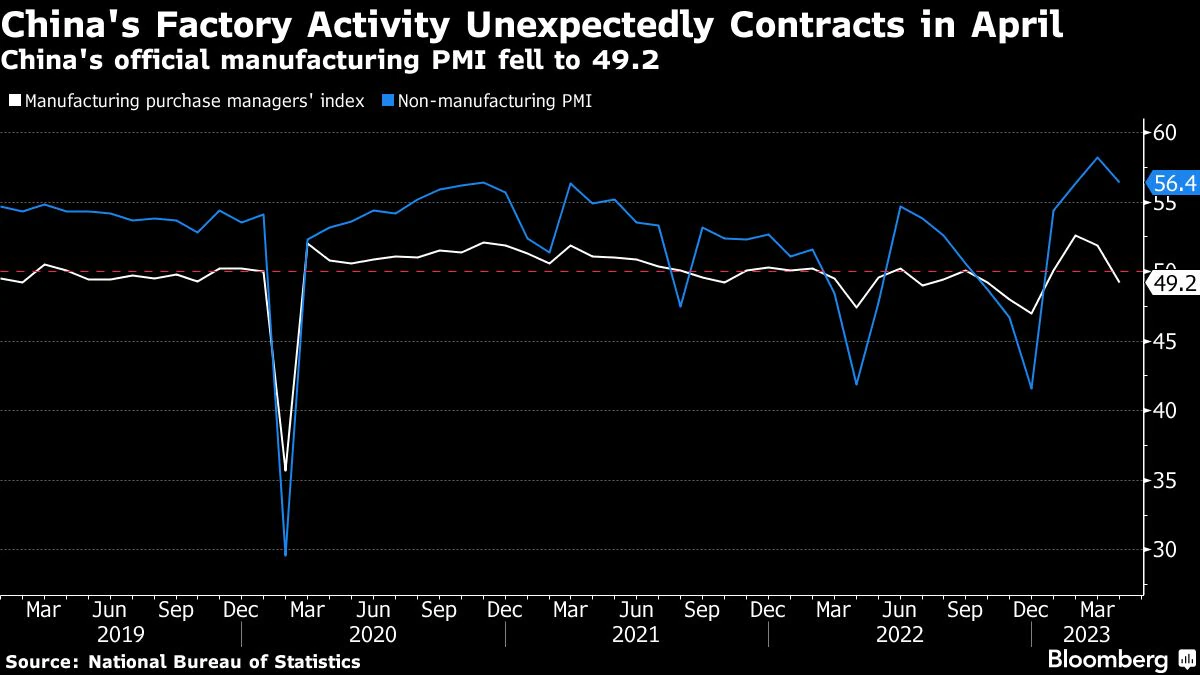

China’s announcement of its most conservative growth target in three decades represents far more than cyclical economic adjustment. The 4.5-5.0% GDP growth target for 2026 signals a fundamental pivot from quantity-driven expansion toward what Beijing terms “high-quality development.” This strategic realignment prioritises artificial intelligence, semiconductor manufacturing, and renewable energy infrastructure over traditional construction and heavy industry.

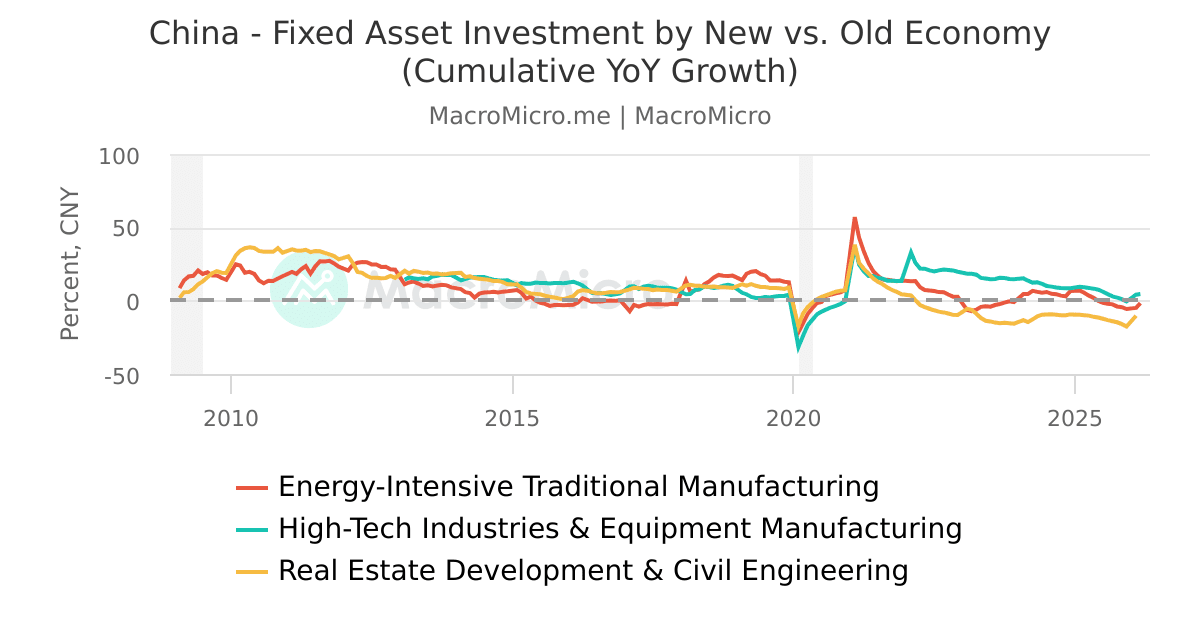

The magnitude of this transformation becomes apparent when examining recent economic data. Fixed asset investment contracted 3.8% in 2025, marking the first such decline in decades. Property investment collapsed by 17.2%, while retail sales growth slowed to just 0.9% in December 2025, approaching COVID-era lows. These figures reflect deliberate policy choices rather than temporary economic weakness.

Understanding China’s Policy-Driven Demand Destruction

Traditional economic analysis often frames commodity demand as cyclical, responding predictably to growth phases and monetary policy adjustments. However, China’s current trajectory represents something fundamentally different: policy-driven demand destruction that restructures entire commodity consumption patterns.

The implications extend far beyond short-term price volatility. When Beijing explicitly redirects investment flows from construction toward technology sectors, it effectively rewrites the demand equation for multiple commodity classes. Furthermore, understanding iron ore trends becomes crucial for assessing the broader market transformation.

Key Economic Transformation Indicators:

- Steel Production: Chinese crude steel output fell below 1 billion tonnes for the first time since 2019

- Construction Activity: Real estate investment declined 17.2% year-over-year

- Consumer Spending: Retail sales growth approached multi-year lows at 0.9%

- Industrial Activity: Manufacturing PMI readings suggest continued weakness in traditional sectors

Iron Ore Markets Face Structural Headwinds

The relationship between China’s property sector and global iron ore demand cannot be overstated. Chinese construction historically consumed approximately 40% of the nation’s steel production, creating direct linkage between property investment and iron ore imports. The current 17.2% decline in real estate investment represents more than cyclical adjustment; it indicates structural demand destruction.

This transformation particularly impacts China economy impact on ASX mining stocks exposed to iron ore production. Companies with heavy China revenue exposure face prolonged headwinds as Beijing’s commitment to reducing overcapacity in traditional industries while promoting technological advancement suggests iron ore demand weakness will persist beyond typical economic cycles.

Supply Chain Disruption and Operational Complexities

Recent restrictions affecting iron ore shipments demonstrate additional risk layers beyond fundamental demand weakness. These supply chain disruptions force cargo redirections and create operational complexities that compound existing market headwinds. Moreover, the geopolitical mining landscape adds volatility to already challenging market conditions.

Iron Ore Market Impact Assessment:

| Factor | Impact Level | Duration |

|---|---|---|

| Property Investment Decline | High | Long-term |

| Steel Production Cuts | High | Medium-term |

| Trade Relationship Tensions | Medium | Variable |

| Capacity Utilisation | Medium | Medium-term |

Critical Minerals: The New Commodity Supercycle

While traditional commodities face structural headwinds, China’s economic transformation creates substantial demand for critical minerals essential to high-technology manufacturing and renewable energy infrastructure. This represents fundamental commodity demand reallocation rather than simple reduction.

Copper markets exemplify this dynamic shift. Despite short-term volatility that saw prices decline to US$5.70 per pound, long-term demand drivers remain robust. Data centre construction, electric vehicle adoption, and grid modernisation projects require massive copper infrastructure investments that align directly with Beijing’s strategic priorities.

In addition, the broader critical minerals strategy demonstrates how government policies reshape commodity demand patterns across multiple sectors.

The Electrification Demand Revolution

The transition toward electrification creates unprecedented demand patterns for specific mineral categories. Electric vehicle production requires approximately 80 kilograms of copper per vehicle, compared to 25 kilograms for internal combustion engines. Data centres consume substantial copper quantities for power distribution and cooling systems, while renewable energy installations require extensive copper infrastructure for power transmission.

Critical Mineral Demand Drivers:

- Artificial Intelligence Infrastructure: Data centres driving copper and rare earth consumption

- Electric Vehicle Adoption: Battery materials including lithium, cobalt, and nickel

- Grid Modernisation: Copper-intensive smart grid installations

- Renewable Energy: Wind and solar installations requiring multiple mineral inputs

ASX Mining Stock Risk Assessment Framework

Understanding China economy impact on ASX mining stocks requires comprehensive risk assessment across multiple dimensions. Companies face varying exposure levels based on commodity focus, geographic diversification, and customer concentration patterns.

Furthermore, iron ore demand insights reveal how different market segments respond to China’s economic transformation.

High-Risk Iron Ore Exposure Companies

Fortescue Metals Group (FMG) represents the highest risk profile among major ASX miners. With approximately 85% of revenue derived from iron ore sales to China, the company lacks diversification buffers that might offset demand weakness. The pure-play iron ore focus creates direct exposure to China’s construction sector decline without meaningful revenue streams from growing commodity categories.

BHP Group (BHP) and Rio Tinto (RIO) carry significant iron ore exposure but benefit from operational diversification across copper, aluminium, and petroleum segments. This diversification provides partial protection against China-specific iron ore demand weakness while maintaining exposure to commodities benefiting from electrification trends.

Beneficiary Companies in Critical Minerals

Sandfire Resources (SFR) exemplifies pure-play copper exposure aligned with long-term electrification trends. The company’s focus on copper production positions it favourably for data centre expansion, electric vehicle adoption, and grid modernisation projects that drive structural demand growth.

South32 (S32) operates a diversified critical minerals portfolio including copper, aluminium, and manganese. This diversification provides exposure to multiple electrification themes while reducing dependence on any single commodity or geographic market.

Risk Assessment Matrix:

| Company | China Revenue % | Commodity Focus | Risk Level | Opportunity Level |

|---|---|---|---|---|

| Fortescue (FMG) | ~85% | Iron Ore | Extreme | Low |

| BHP Group (BHP) | ~65% | Diversified | Moderate-High | Medium |

| Rio Tinto (RIO) | ~70% | Iron Ore + Aluminium | High | Medium |

| Sandfire (SFR) | ~40% | Copper | Low | High |

| South32 (S32) | ~45% | Diversified Critical | Low-Medium | High |

Investment Strategy Framework for the New Commodity Cycle

Successful navigation of this commodity market transformation requires strategic framework thinking rather than tactical positioning. The fundamental shift in China’s economic priorities creates both immediate risks and long-term opportunities that demand differentiated investment approaches.

Sectoral Rotation Strategy Implementation

Recommended Portfolio Allocation Adjustments:

- Reduce Iron Ore Exposure: Underweight traditional steel-making commodity producers

- Increase Critical Minerals: Overweight copper, lithium, and rare earth producers

- Geographic Diversification: Favour companies with non-China revenue streams

- Technology Integration: Prefer miners investing in automation and sustainability

Timing Considerations and Market Entry Points

Short-term market volatility creates tactical opportunities for long-term positioned investors. Copper price weakness driven by broader China anxiety may create entry points for companies with strong electrification exposure. However, investment risk appetite requires careful evaluation given structural rather than cyclical demand headwinds affecting iron ore companies.

Investment Timeline Framework:

Short-term (6-12 months):

- Iron ore prices likely remain under pressure

- Copper volatility creates tactical opportunities

- Critical minerals supply constraints support pricing

- Market sentiment remains volatile around China exposure

Medium-term (1-3 years):

- Electrification demand acceleration becomes apparent

- Supply chain diversification efforts gain momentum

- China’s economic transformation effects fully materialised

- Clear winners and losers emerge among ASX miners

Long-term (3-5 years):

- Structural shift toward electrification commodities established

- Chinese demand composition permanently altered

- Australian critical mineral producers potentially outperforming

- New commodity supercycle characteristics become evident

The next major ASX story will hit our subscribers first

Monitoring China’s Economic Recovery Signals

Effective investment decision-making requires systematic monitoring of leading indicators that signal changes in China’s economic trajectory. Understanding which metrics provide early warning signals enables proactive portfolio adjustments before broad market recognition of trend changes.

What are the Primary Economic Indicators to Track?

Monthly Steel Production Data serves as the most direct indicator of iron ore demand trends. Changes in production patterns reflect both government policy implementation and actual construction activity levels. Consistent production increases would signal genuine demand recovery rather than temporary inventory adjustments.

Property Construction Starts provide forward-looking insight into future steel demand. While property investment data reflects current activity, construction start permits indicate future building activity that will drive commodity consumption in subsequent quarters.

Essential Monitoring Metrics:

- Industrial Electricity Consumption: Real-time indicator of manufacturing activity

- Manufacturing PMI Sub-components: Specific sectoral demand patterns

- Credit Growth in Infrastructure: Government spending commitment levels

- Port Inventory Levels: Supply-demand balance indicators

- Commodity Futures Positioning: Market sentiment and expectation changes

Policy Signal Analysis Framework

Chinese government communications require careful interpretation to distinguish between rhetorical positioning and actual policy implementation. Statements regarding infrastructure spending, property market support measures, and industrial policy priorities can rapidly alter commodity demand trajectories.

Key Policy Signal Categories:

- Central Bank Communications: Monetary policy direction and economic priorities

- State Council Announcements: Fiscal spending and infrastructure investment plans

- Industry Ministry Guidance: Sector-specific production targets and capacity constraints

- Regional Government Actions: Local implementation of national policy directives

Risk Management in Volatile Commodity Markets

The current commodity market environment demands sophisticated risk management approaches that account for both traditional market volatility and structural economic transformation. Standard portfolio construction methods may prove inadequate when fundamental demand patterns undergo permanent alteration.

Portfolio Protection Strategies

Geographic Diversification extends beyond simple non-China exposure. Successful diversification requires understanding end-market demand patterns across different economic development stages. Markets with growing infrastructure needs may offset China’s reduced construction activity, while developed markets drive electrification commodity demand.

Commodity Diversification involves strategic allocation across both declining and growing commodity categories. Maintaining some exposure to traditional commodities provides protection against potential China policy reversals while building positions in critical minerals captures long-term electrification trends.

Advanced Risk Management Techniques:

- Scenario Analysis: Stress testing portfolios against various China recovery scenarios

- Dynamic Hedging: Adjusting protection levels based on volatility regimes

- Correlation Monitoring: Understanding changing relationships between commodity prices

- Liquidity Management: Ensuring adequate cash positions for opportunity deployment

How Resilient is Your Portfolio Under Stress?

Base Case Scenario (40% probability): China’s transformation continues as planned, creating sustained weakness in iron ore while critical minerals benefit from electrification demand.

Bear Case Scenario (25% probability): Global economic slowdown reduces demand across all commodity categories, with critical minerals unable to offset traditional commodity weakness.

Bull Case Scenario (35% probability): China policy reversal toward infrastructure stimulus combined with accelerated global electrification creates broad-based commodity demand recovery.

According to recent analysis, China’s debt and growth challenges represent significant headwinds for ASX mining companies with heavy exposure to Chinese demand.

Understanding China’s economic transformation requires recognising this represents policy-driven structural change rather than cyclical adjustment. Investors who position for permanent demand pattern shifts rather than temporary weakness will likely achieve superior long-term returns in the evolving commodity landscape.

China’s deliberate economic restructuring creates a bifurcated commodity environment where traditional materials face sustained pressure while critical minerals benefit from electrification trends. China economy impact on ASX mining stocks will continue differentiating between companies positioned for the old economy versus those aligned with technological transformation.

The investment opportunity lies in recognising that China’s economy is not merely slowing but fundamentally changing its consumption patterns. Mining companies with exposure to artificial intelligence infrastructure, renewable energy systems, and electric vehicle supply chains align with China’s strategic priorities, while traditional iron ore producers face structural headwinds that may persist for years.

Successful navigation requires abandoning hope for a return to previous commodity demand patterns while embracing the opportunities created by economic transformation. However, as market analysis suggests, many ASX-listed miners appear overvalued given these structural changes. The next decade of commodity investing will reward those who understand that China’s pivot toward high-quality growth creates permanent winners and losers rather than temporary market dislocations.

Disclaimer: This analysis contains forward-looking statements and investment opinions that involve risks and uncertainties. Commodity markets are inherently volatile and past performance does not guarantee future results. Readers should conduct their own research and consider seeking professional financial advice before making investment decisions.

Could Your Portfolio Benefit from Real-Time Mining Discovery Alerts?

Discovery Alert’s proprietary Discovery IQ model delivers instant notifications when significant ASX mineral discoveries are announced, helping investors identify actionable opportunities in both traditional and critical minerals sectors ahead of broader market recognition. With China’s economic transformation reshaping commodity demand patterns, staying informed about new discoveries becomes crucial for positioning ahead of structural market shifts—start your 14-day free trial today to gain this competitive advantage.