The Russian economy is struggling and ‘currently below expectations’, according to President Vladimir Putin, who expressed his frustration in a meeting with top officials

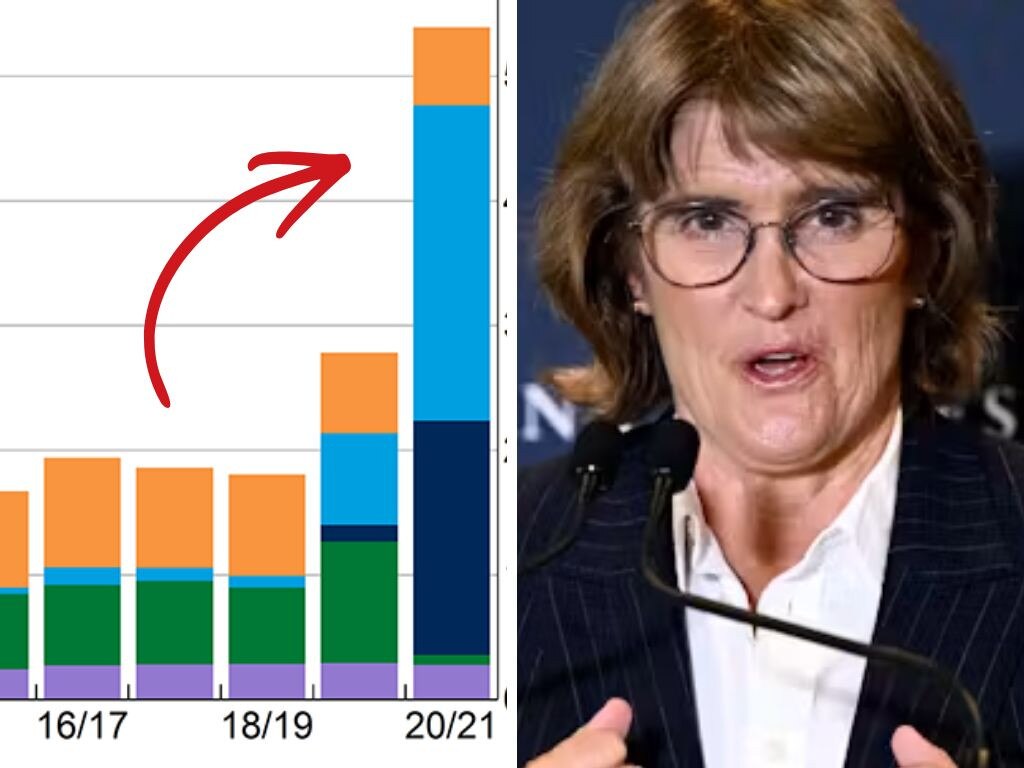

The Russian economy is performing below expectations, Putin said(Image: POOL/AFP via Getty Images)

Vladimir Putin has admitted Russia’s economy is struggling as he blasted officials for not coming up with a plan.

The Russian leader said in a televised meeting on Wednesday that Russia’s GDP had shrunk by a combined 1.8 percent over January and February.

“I expect to hear detailed reports today on the current economic situation and why the trajectory of macroeconomic indicators is currently below expectations,” Putin said during the broadcast attended by Prime Minister Mikhail Mishustin and other top officials.

“Moreover, below the expectations of not only experts and analysts, but also the forecasts of the government itself and the central bank of Russia.”

READ MORE: Hero Garda officer who hunted Daniel Kinahan dies before ‘crime boss’s’ Dubai arrestREAD MORE: Louisiana shooting horror with 8 kids dead is ‘unlike anything police have ever seen’

Also in attendance were the Kremlin’s deputy chief of staff Maxim Oreshkin, the central bank governor Elvira Nabiullina, first deputy PM Denis Manturov and deputy PM Alexander Novak. The CEO of Promsvyazbank, a state-owned bank, was also present. High inflation, thanks to Putin’s illegal war on Ukraine, has seen a slowdown in the Russian economy.

In 2023, Russia’s GPD expanded by 4.1 percent and 4.9 percent the following year despite Western sanctions following the full-scale invasion of Ukraine. But strategic Ukrainian atttacks on Russian energy have hurt a potentially large uplift due to the US-Israeli war on Iran.

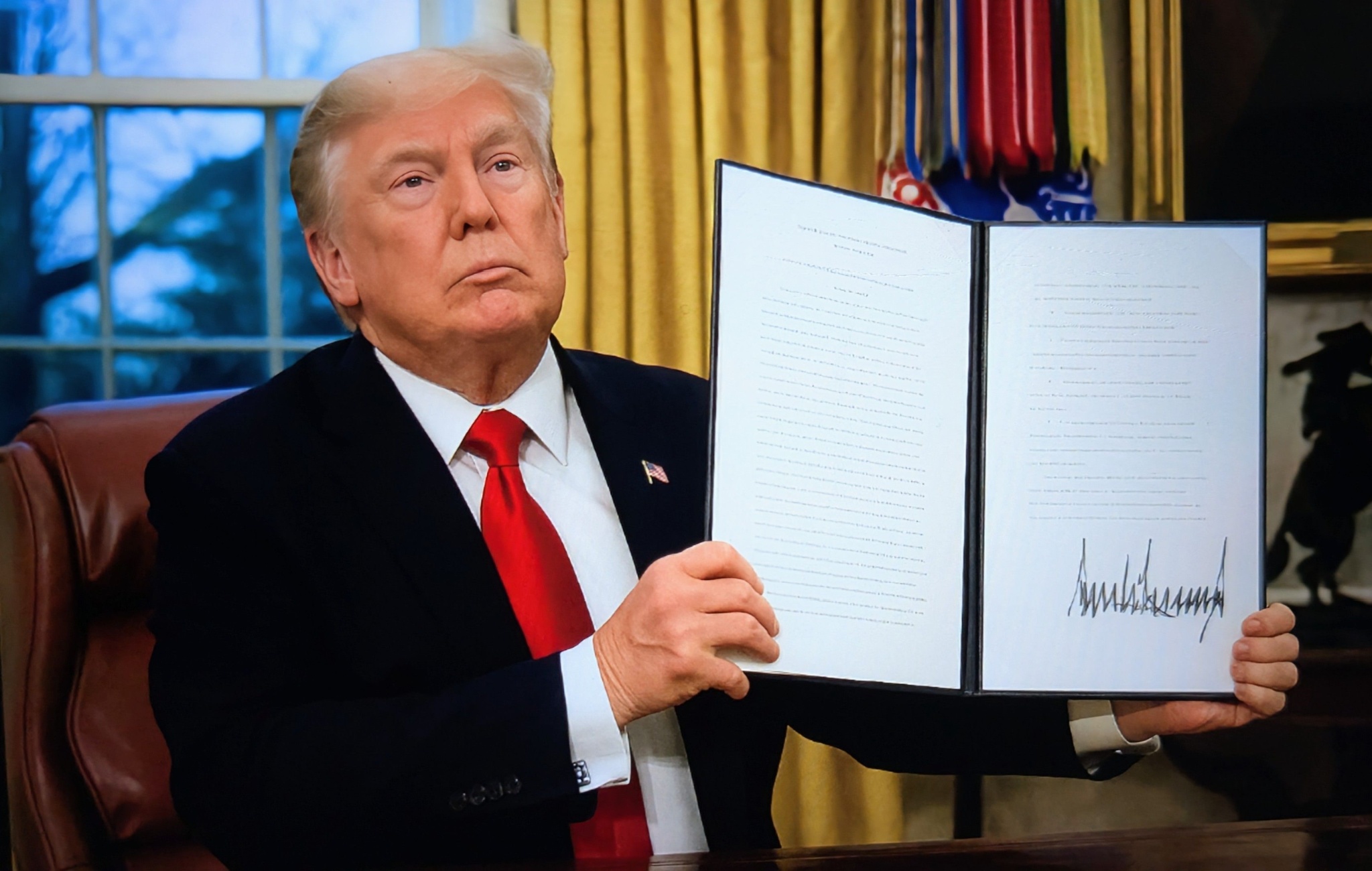

The war in Iran sent oil prices soaring, but reports suggest the Ukrainian strikes have hindered a large chunk of Russia’s potential windfall from exports after the crisis began. Some of the sanctions on Russian oil were also eased by US President Donald Trump in March, with the administration choosing to extend the pause on sanctioning Russian oil loaded onto tankers again this month.

Amid Putin’s further problems are a budget deficit that has widened to around £43billion, falling oil tax revenues and a lack of available labour. This is partly an impact of the war, which has seen unemployment drop to record lows.

“The peculiarity of the current situation is that for the first time in modern history, our economy has faced shortages or limits on labor,” central bank governor Elvira Nabiullina said. “This is a new reality for the government and for business alike. In the past, high-rate cycles were tied to temporary external shocks, and once things stabilised, we cut rates fairly quickly. Now, however, we are facing a persistent downturn in external conditions affecting both exports and imports.”

This has impacted inflation and kept interest rates high, although the latter has eased slightly recently following a decision by the central bank. Putin has already been warned by his own officials that a financial crisis could hit later this year, potentially as early as the summer, Fortune reported.

The high interest rates that have curbed inflation have hit the profits of Russian companies. Some workers have gone unpaid or had their hours cut, with some furloughed. In short, Russian consumers are finding it harder to pay their loans.

“A banking crisis is possible,” one Russian official told the Washington Post in December. “A nonpayments crisis is possible. I don’t want to think about a continuation of the war or an escalation.”