Australia entered this year with genuine momentum. Gross domestic product grew at its fastest pace in nearly three years through late last year, the labour market held firm and there were early signs that the rate cycle was doing its job.

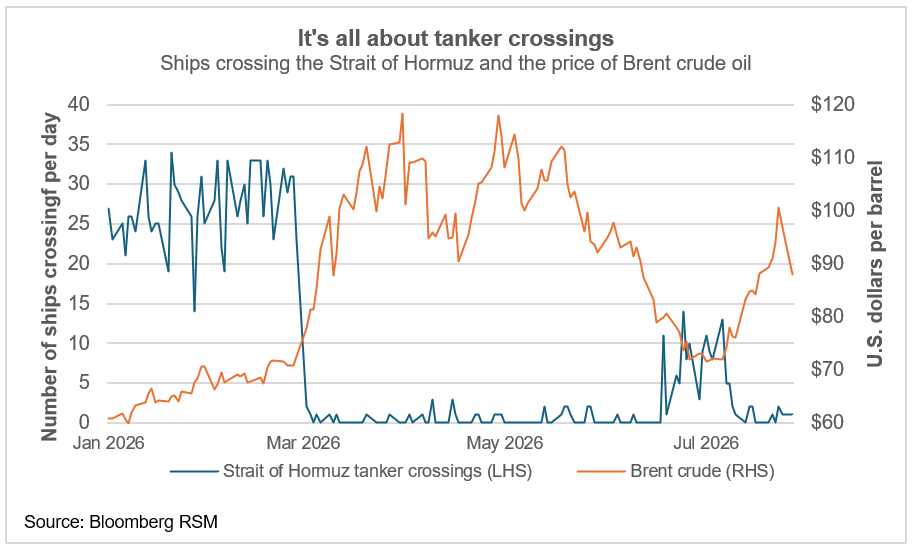

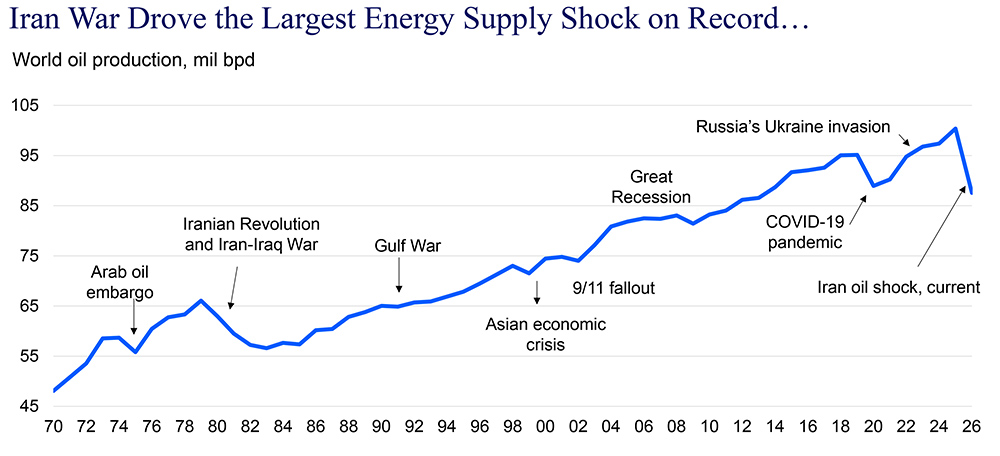

The outbreak of the war in Iran, though, exposed how tenuous that foundation was. For more than six weeks, Australia’s imports of energy and other commodities shriveled up, and the damage to the economy has been significant.

On Sunday, the Strait of Hormuz was again effectively shut after several days of contradictory statements and actions. Regardless of whether there is any lasting resolution, Australia still faces structural problems that will be stubbornly hard to fix.

The vulnerability to an energy shock was always there. The war just made it undeniable.

Get RSM’s Market Minute economic commentary every morning. Subscribe now.

Australia is among the world’s highest per-capita consumers of diesel, a direct consequence of its geography. Mining, trucking, agriculture and aviation all run on it. Yet the country holds an average of 30 days of diesel reserves, the lowest of any International Energy Agency member and well below the 90-day obligation.

Domestic refining capacity has been hollowed out over the past decade, leaving the economy dependent on imports for nearly 90% of its diesel. Most of that flows from Gulf crude refined through Singapore, Malaysia and South Korea—all routes that pass through or near the now-disrupted Strait of Hormuz.

When the strait was effectively closed following the start of the Iran war, the supply chain didn’t bend, it fractured. Wholesale diesel prices in the region more than doubled almost immediately. By early April, around 300 service stations had run dry.

The government has moved quickly to ease the damage, underwriting purchases through Export Finance Australia, launching a national conservation campaign and dispatching the prime minister on diplomatic missions across Singapore, Brunei and Malaysia.

These are the right steps. But they are crisis management, not a solution. The assurances coming back from regional partners are that conditional supply will continue as long as their own upstream sources hold. That is a fragile guarantee in a fragile environment.

Consumer and business confidence

The fuel shock didn’t arrive into a neutral economy. Households were already absorbing two rate rises this year, with the full effects of monetary tightening yet to be felt. Add surging pump prices to stretched mortgage repayments, and the pressure on discretionary spending becomes acute.

The Westpac–Melbourne Institute consumer sentiment index fell to 80.1 in April, falling to levels last seen during the pandemic. The NAB business survey recorded the second-largest confidence collapse in its history. Forward orders have been wiped out. Purchase cost growth among businesses more than doubled in the March quarter.

The property market is telling the same story. Auction clearance rates fell to 52.7% in late March—the lowest since 2022—and have remained below 60% for two consecutive weeks. Homebuyers backing away from auction are a reliable, real-time read on household confidence. Right now, that read is cautious.

What’s a central bank to do?

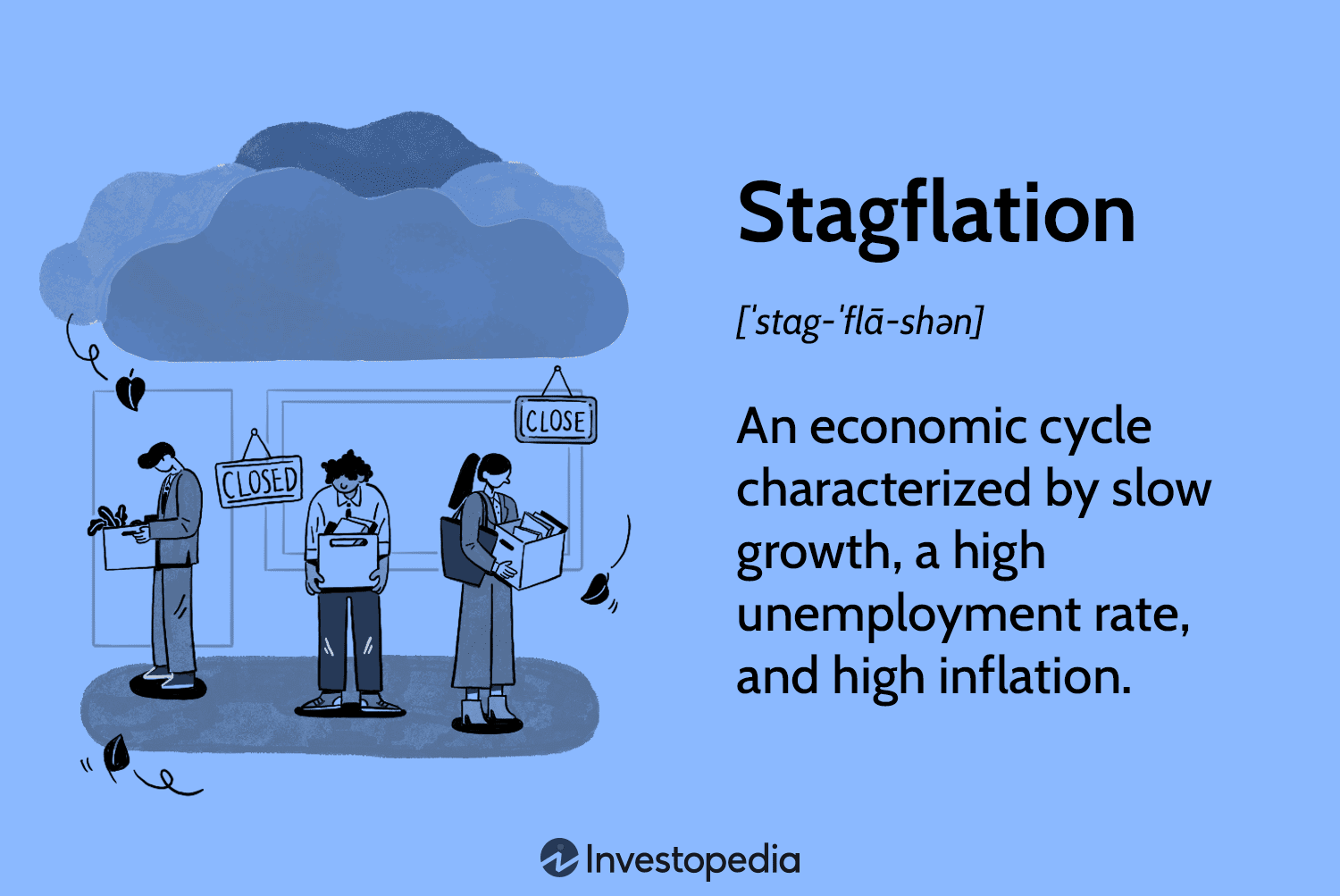

Stagflation, rising prices alongside weakening demand, is the central bank’s hardest scenario to manage because the standard tools work in opposite directions. Rate rises cool inflation but deepen the growth slowdown. Rate cuts support demand but risk entrenching inflationary expectations.

With a third consecutive hike now widely anticipated in May, the Reserve Bank of Australia is signaling that inflation control remains the priority. That is defensible. But the cost will be felt in household balance sheets and business investment pipelines that are already under strain.

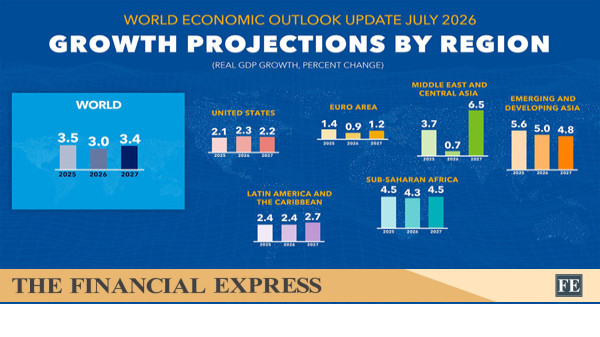

The International Monetary Fund’s most recent World Economic Outlook frames the global stakes plainly: in a severe conflict scenario, global growth could be reduced by 1.3 percentage points this year, a near-miss for a global recession by its own definition. For an open, trade-exposed economy like Australia, the external headwinds compound the domestic ones.

The takeaway

The bottom line is that Australia is not yet in recession, but the direction of travel is clear. Confidence is falling, real incomes are being squeezed and the policy room to respond is constrained.

What the fuel crisis has laid bare is a decade of underinvestment in energy sovereignty. Diplomatic missions to Southeast Asia are necessary and welcome. But the longer-term solutions—strategic fuel reserves, domestic refining capacity, supply chain diversification—require ambition that goes well beyond the current crisis response.