(Oil & Gas 360) – By Greg Barnett, MBA – OPEC+ was once sold as a stabilizing force in global energy markets, a mechanism through which oil‑producing nations could smooth volatility, protect investment, and prevent destructive price collapses. That argument made sense when oil demand was rising rapidly, capital was scarce, and non‑OPEC supply was marginal.

OPEC+: Market stabilizer, or a structural drag on the global economy?- oil and gas 360

None of those conditions hold today.

Instead, OPEC+ increasingly functions as a system that distorts price signals, undermines diplomatic objectives, and locks weaker member states into economic underperformance—all while imposing real costs on the global economy.

The evidence suggests that OPEC+ is no longer stabilizing markets. It is resisting them.

At its core, OPEC+ rejects the central mechanism that makes markets efficient: prices determined by marginal cost and open competition. By coordinating supply cuts in a world where non‑OPEC production continues to expand, the group attempts to manage scarcity long after scarcity has ceased to be structural.

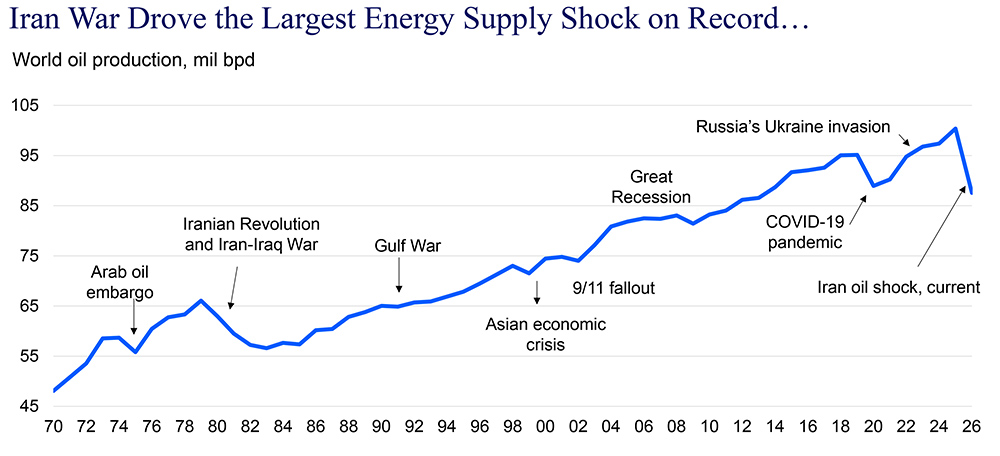

This is not theoretical. Global spare capacity today sits well above historical norms, even as OPEC+ curtails output. The result is not stability, but a persistent disconnect between physical supply conditions and price formation. Markets receive a signal of shortage when abundance exists, encouraging inflation, discouraging demand, and misallocating capital.

This outcome is precisely what classical economists warned against. When price discovery is replaced by centralized coordination, the system becomes brittle. It cannot adapt smoothly to shocks, and it overreacts when those shocks arrive.

The macroeconomic consequences are tangible. Elevated oil prices function as a global tax, one that is regressive by nature. Energy‑importing countries, particularly in the developing world, absorb higher transportation costs, higher food prices, and higher borrowing costs simultaneously. International financial institutions have repeatedly shown that sustained oil prices near the upper end of recent trading ranges materially reduce global growth, raise inflation, and increase the probability of recession.

This burden falls disproportionately on countries that neither produce oil nor benefit from OPEC+ revenues. The system redistributes income upward, from consumers to producers, while offering little in return in terms of genuine price stability.

Ironically, even many OPEC+ members struggle under this arrangement. Several require oil prices far above market‑clearing levels simply to balance public budgets. That fiscal dependence incentivizes supply restraint regardless of demand conditions and discourages domestic reform. Over time, it entrenches rent‑seeking behavior, weak institutions, and economic stagnation.

The contrast with the United States is instructive. America’s oil sector operates largely on market principles: capital discipline, technological innovation, and competition determine output. The result has been rising productivity, lower long‑term costs, and a higher quality of life, despite far less direct state control. Where OPEC+ uses coordination to defend prices, the U.S. uses efficiency to survive them.

The geopolitical implications are equally problematic.

By including Russia, OPEC+ has become an indirect financial stabilizer for a sanctioned state. Coordinated supply restraint has repeatedly lifted global prices at moments when Russian revenues would otherwise have fallen. Even when Russian barrels are discounted, higher benchmark prices offset those discounts, preserving cash flow and weakening the effectiveness of Western sanctions.

At the same time, OPEC+ has facilitated the emergence of a parallel energy trade system centered on China. Predictable, cartel‑managed supply allows Beijing to stockpile, negotiate discounts, and reduce exposure to market volatility, advantages that accrue precisely because the market is not free.

From a U.S. policy perspective, this is a perverse outcome. OPEC+ complicates efforts to isolate Russia, strengthens China’s energy security, and reduces the leverage that transparent, competitive markets would otherwise provide.

Defenders of OPEC+ often argue that the group merely reacts to market forces rather than shaping them. But this defense concedes the central point. If OPEC+ no longer controls the market—and non‑OPEC supply continues to grow, then coordinated restraint becomes less effective and more distortionary. The cartel bears the costs of lost volume while the rest of the world bears the costs of inflated prices.

Even sympathetic observers increasingly acknowledge that OPEC+ behaves reactively, cutting output after prices fall rather than preventing volatility in advance. In doing so, it amplifies cycles instead of smoothing them.

The deeper issue is structural. Cartels tend to be most dangerous not when they are strongest, but when their power begins to erode. As market share slips, incentives to defend prices intensify, even as the ability to do so diminishes. The result is over‑management, mispricing, and eventual loss of relevance.

There is also a human cost that rarely receives attention. Resource‑dependent economies consistently underperform diversified ones on measures of health, education, and income stability. By insulating weaker producers from market pressure, OPEC+ reduces the incentive to reform.

If those countries were forced to operate closer to economic reality, competing on cost, efficiency, and governance, capital would flow differently, institutions would evolve faster, and long‑term living standards would likely improve.

In that sense, OPEC+ may be doing its poorest members no favors.

A world with a more market‑driven oil system would not be chaos. It would likely feature lower average prices, clearer investment signals, faster technological adaptation, and greater alignment with global economic growth. Volatility would still exist, but it would reflect real conditions rather than coordinated intervention.

OPEC+ once served a purpose. That purpose is fading.

What remains is a system that raises prices without reliably delivering stability, subsidizes geopolitical rivals, weakens diplomatic leverage, and delays economic reform in the very countries it claims to protect.

Markets do not fail because they are free. They fail when they are prevented from working.

OPEC+ today looks less like a stabilizer of the global energy system, and more like a relic resisting its inevitable evolution.

The views expressed in this article are solely those of the author and do not necessarily reflect the opinions of Oil & Gas 360. Please consult with a professional before making any decisions based on the information provided here. Please conduct your own research before making any investment decisions.