A note on the “80/20” framework: China’s strategic emerging industries — AI, robotics, new energy, aerospace, biotech, and advanced materials — accounted for roughly 17% of GDP as of 2025, according to estimates from the NDRC and China’s National Information Center. The remaining ~83% is the traditional economy. I round this to 80/20 because it captures the essential structure: Beijing is concentrating the vast majority of its policy support, capital allocation, and political attention on this ~20%, while the other ~80% receives minimal incremental support and must recover on its own. The “80/20” describes the policy split, not a precise statistical breakdown.

1. The 80/20 Framework

-

~80% of China’s economy = traditional manufacturing and industry. No big stimulus — must recover on its own.

-

~20% = high-tech new economy (AI, robotics, aerospace, biotech). Getting all the government’s policy support. The 80/20 describes the policy split, based on NDRC data showing strategic emerging industries at ~17% of GDP.

2. The 80% Has Turned a Corner

After years of involution, two unexpected factors broke the cycle: geopolitical supply-demand rebalancing and imported inflation jolting China out of deflation.

3. Global Demand for Chinese Manufacturing Is Surging

-

Countries building independent manufacturing and defense systems now rely more heavily on Chinese intermediate goods.

-

Even with price increases, Chinese products remain competitive — baseline costs are lower.

4. Recovery Is Real but Gradual

-

“ICU to KTV” is not happening. Slow, self-driven, healthy recovery.

-

Critical data point: whether prices have stabilized.

5. The 20% — Just Give It Time

6. Consumption: Weak in Value, Not in Volume

-

Income data still soft, but prices extremely low — volume consumption is decent.

-

Household balance sheets repairing. Wages in some sectors have stopped falling.

-

Public services dramatically improved — reducing discontent without income growth.

7. Real Estate Mini-spring

8. The Big Takeaway

-

This recovery is self-generated, not stimulus-driven. Policy provided a floor, not a push. That makes it more durable.

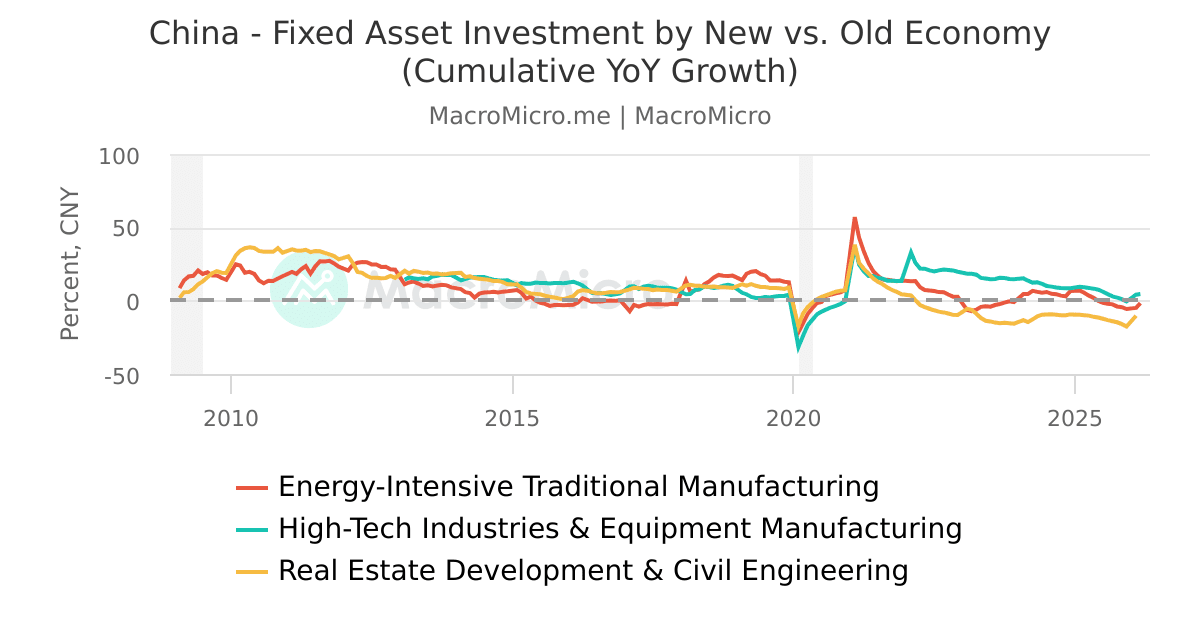

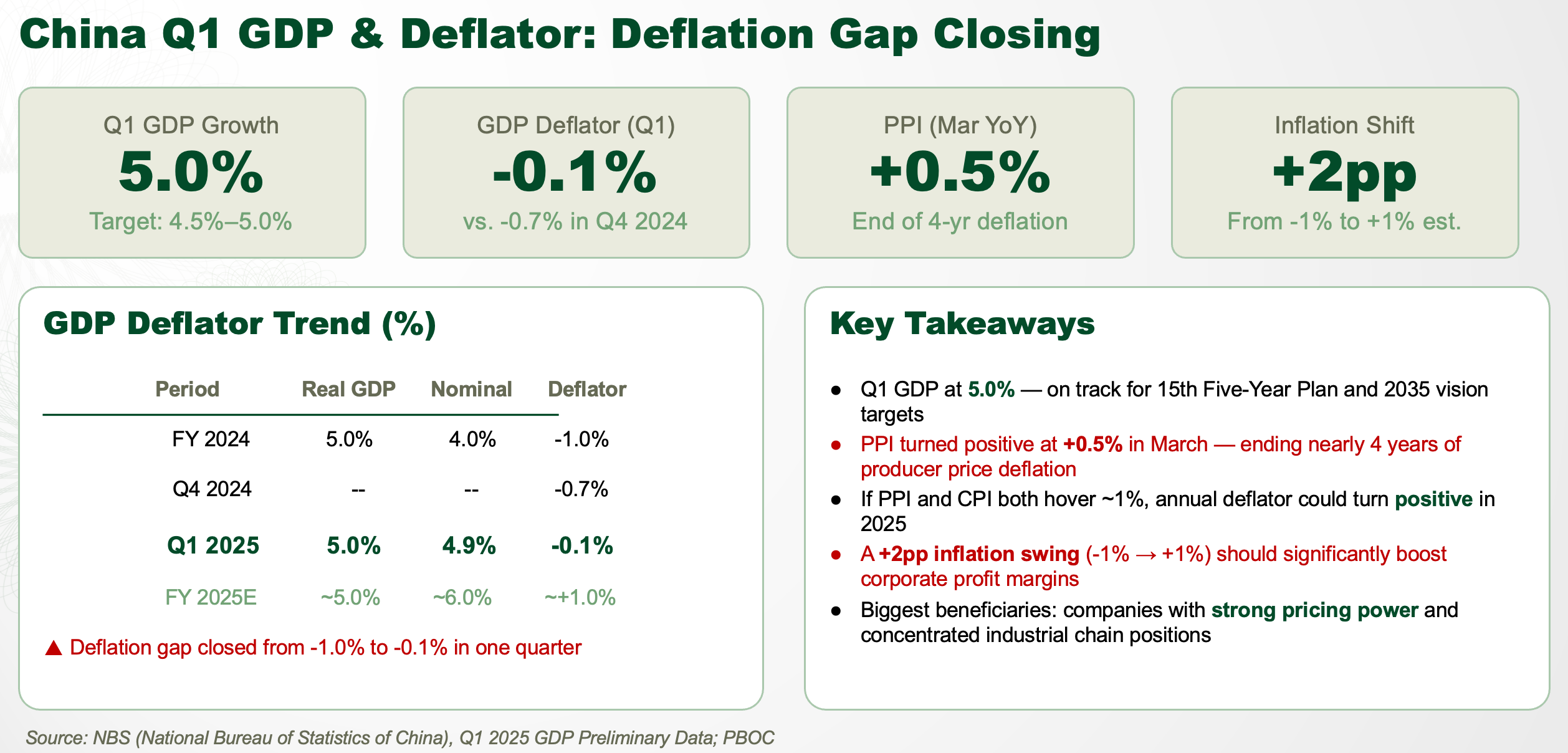

A warming narrative has emerged since the end of last year, that 2026 would become a critical turning point for the Chinese economy. Current data is beginning to confirm this. A key indicator is the Producer Price Index (PPI). The overall economic deterioration in China over the past few years — low income growth, stagnant demand — has been accompanied by a sustained downturn in manufacturing. Since manufacturing and industry are the pillars of the Chinese economy, we must watch whether the PPI turns positive. An improving PPI would signal a potential recovery in industrial profitability.

Current data supports this outlook, though the recovery will be gradual. I want to stress one major premise: the “symptoms” of the Chinese economy and its “treatment plan” are now very clear.

For the 80% of the economy made up of traditional industries, stabilization will not come from large-scale policy stimulus. This 80% must recover on its own strength, because the government’s policy firepower is now entirely directed toward the 20% representing the “new economy.”

Over the past few years, traditional sectors have been grinding through a state of hyper-competition — what the Chinese call involution. Without new support policies, businesses have been forced to compete one another into the ground, driving profits to razor-thin margins or outright losses. This has pushed many into “going global,” where, interestingly, profit margins are actually rising.

We are now seeing a phenomenon where, after years of painful self-correction, two unexpected factors in early 2026 may have broken this vicious cycle:

-

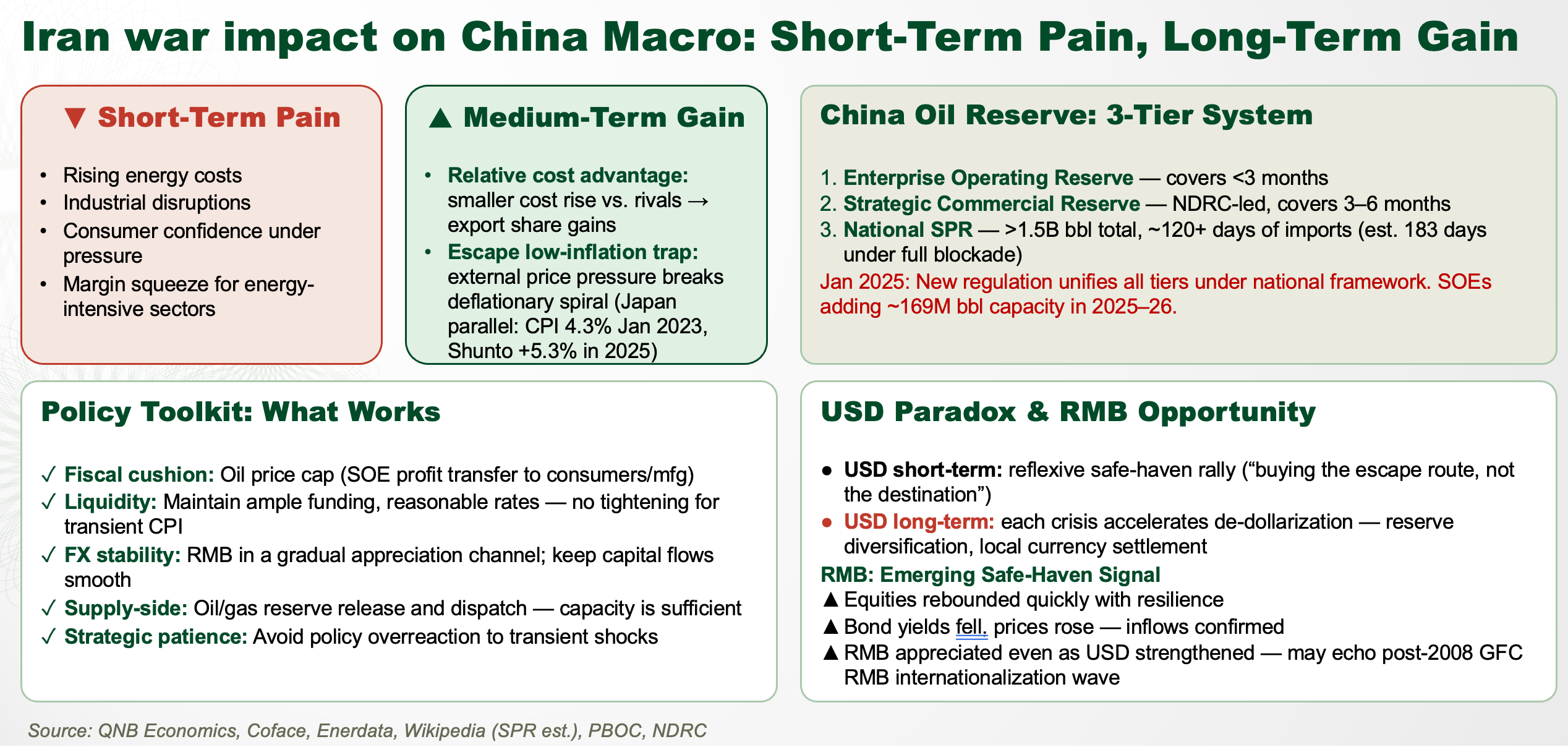

Geopolitical rebalancing of supply and demand. Conflicts such as the Iran-Israel situation have disrupted global supply chains, turning what was severe industrial oversupply into surging demand for Chinese manufacturing.

-

Imported inflation as a circuit breaker. Rising external prices and energy shortages have created a form of imported inflation that is jolting China out of its deflationary spiral.

This is strikingly similar to what happened in Japan during the Russia-Ukraine war: external inflationary pressure finally broke a 30-year deflationary trap and forced the economy into a positive cycle. That is the current state of the 80%.

There is a fascinating phenomenon unfolding within this 80%. We are seeing a comprehensive global expansion of Chinese industry at every level — from low-end to high-end manufacturing.

Demand for Chinese intermediate manufacturing goods is surging. Prices remain relatively low, but the demand structure is shifting. As countries around the world rush to build independent manufacturing and defense capabilities, their reliance on Chinese intermediate products has increased sharply.

Several factors suggest prices for these goods are set to rise:

-

Rising raw material costs

-

Energy shortages

-

Inflationary pressures in buyer countries

Even if Chinese prices increase, demand is unlikely to soften — because China’s baseline costs are lower, its products remain highly competitive after a price hike, especially when competitors are forced to raise their prices even more.

Looking at this industrial manufacturing base — the 80% that many critics claimed would collapse — I am fairly confident it has already turned a corner. We expect a “positive cycle” to emerge this year.

But this recovery will not be an overnight transformation. As I like to put it: it’s not a move from the ICU straight to a KTV lounge. There won’t be dramatic policy support. This is a self-driven recovery, built on the slow correction of supply-demand imbalances. The growth will be gradual and healthy, following its own internal logic. The critical data point to keep watching: whether prices have finally stabilized.

Frankly, there is not yet sufficient evidence to show that incomes have stabilized, domestic demand has improved, or consumption has meaningfully increased. The data remains weak. However, we must remember this is against a backdrop of extremely low prices in China. If we look at consumption by volume rather than value, it is not actually very low.

We are starting to see signs of stabilization in household balance sheets. Previously, these were severely damaged by falling housing prices, but there are now signs of repair, supported by concrete evidence. We have also observed that wages in some industries have started to rise — or at least stopped falling — all indications of a gradual recovery.

Moreover, China’s current policy direction is clear: while high wages might not be the goal for everyone, basic guarantees must be in place. On a recent visit home, I accompanied my mother to the hospital and saw firsthand how much public hospital infrastructure has improved. She can now receive cancer treatment almost free of charge.

Previously, our city had only one oncology hospital, and every visit was miserable — overcrowded, understaffed. Now, it’s excellent. The conditions are comparable to private hospitals in Bangkok: plenty of medical staff, modern facilities and equipment, domestically developed drugs, and a social security and insurance system that keeps costs very low.

I have also seen significant investment in community infrastructure — community services, community canteens, public amenities. The net effect may be that while people’s incomes are not particularly high, their lives are increasingly worry-free. Public discontent domestically is at very low levels now, which is completely different from two years ago.

The prevailing consensus is that if housing does not recover, neither will the Chinese economy or domestic demand. However, the structure of the Chinese economy has clearly changed — it is no longer as heavily reliant on real estate as before.

Recent data shows that first-tier cities are experiencing a “mini-spring,” with both new home sales and second-hand transactions seemingly on the rise. This is a trend worth continuous monitoring.

Our overall situation is slowly improving. The most significant characteristic of this recovery is that it has not relied on stimulus — it is entirely self-generated. Policy has provided a floor, but has not actively intervened. The economy has genuinely pulled itself through this time.

And that is the most crucial point.