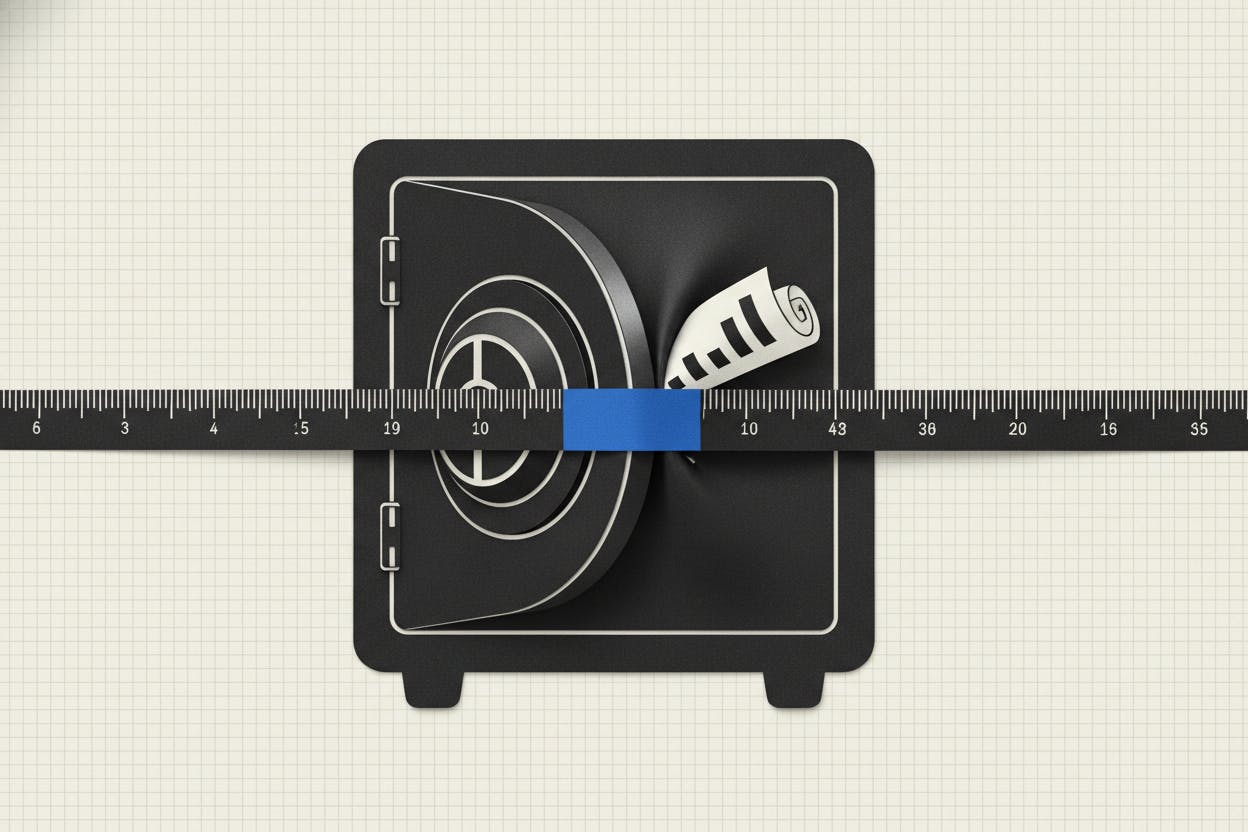

ve cheaper components. So CoreWeave executives have discussed hedges linked to memory-chip stocks, including put options, which rise in value when the stock price falls, according to a person familiar with the talks; Reuters says no trades have been placed and discussions are still early. The catch is that this is a proxy hedge: chipmakers’ shares often fall when the memory cycle turns down, but they also move with the broader stock market and company-specific news. And with chipmakers pointing to new manufacturing capacity being fully ramped in early 2028, the timing of the next price swing matters as much as the direction.

Why should I care?

For markets: CoreWeave’s hedge idea could route AI hardware risk through Micron-linked options.

If CoreWeave is locked into price-floor contracts and memory prices slide, it risks paying above-market input costs while competitors’ costs fall. Using puts on memory-chip stocks could offset some of that pain, because supplier shares tend to weaken when pricing rolls over. But the hedge won’t match CoreWeave’s actual invoices, so “basis risk” – the gap between what it needs protection on and what it can trade – could leave it under-hedged or over-hedged. If more AI infrastructure buyers follow suit, equity and options markets tied to firms like Micron and SK Hynix could become a practical venue for managing the hardware cycle, pulling chip pricing more tightly into broader market positioning.