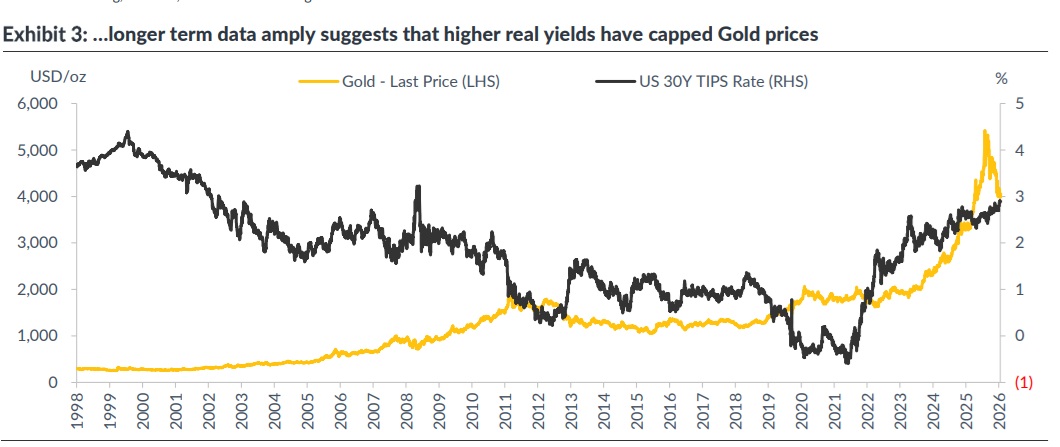

Synthetic futures trading on the Hyperliquid platform are pointing to a first-day surge of 16% to 20% for SpaceX shares when they begin trading on the Nasdaq under the ticker SPCX Thursday. With contracts changing hands between $157 and $162 — well above the $135 IPO price — the derivatives market is betting on a strong debut despite mounting criticism from Capitol Hill and Wall Street’s short-sellers.

The offering itself has already made history. SpaceX plans to raise roughly $75 billion by selling shares at $135 apiece, the largest initial public offering ever. Demand smashed through expectations, with the order book swelling to more than $250 billion — roughly four times the available supply. In a rare move, the company reserved 30% of the shares, or about $22.5 billion, for individual investors, a far cry from the 5% to 10% typical in mega-IPOs. Retail investors can place orders through Fidelity, Charles Schwab, Robinhood, SoFi, or E-Trade.

The Revenue Picture and the Red Ink

SpaceX reported total revenue of $18.7 billion for 2025, with its Starlink segment contributing $11.4 billion and xAI adding $3.2 billion. Starlink now counts 10.3 million subscribers and generated an operating profit of $4.4 billion. Yet the company remains deep in the red. Its net loss for the full year stood at just under $5 billion, and the bleeding accelerated in the first quarter of 2026, when the loss hit $4.28 billion. The primary culprit is xAI, which lost $6.36 billion in 2025 on $3.2 billion in revenue; the artificial-intelligence unit consumed 61% of all capital expenditure in the most recent quarter.

The IPO valuation of roughly $1.75 trillion reflects the February 2026 merger with Elon Musk’s xAI. That price tag implies a price-to-sales ratio of about 90 times trailing revenue — a number that has drawn fire from skeptics.

Should investors sell immediately? Or is it worth buying SpaceX?

Bulls See Room to Run

Optimists on the Street are making bold calls. Oppenheimer initiated coverage Wednesday with a 12-month price target of $190, a 40% premium to the offering price, citing SpaceX’s structural dominance in space infrastructure. New Street Research’s Pierre Ferragu set a target of $165, underpinned by a projection of $195 billion in revenue and $65 billion in EBIT by 2030. In a bull-case scenario involving orbital AI data centers and Mars colonization, Ferragu sees the stock reaching $330.

The company also secured investment-grade credit ratings from Moody’s, S&P, and Fitch just ahead of the listing. That should ease refinancing: CreditSights analysts expect SpaceX to issue bonds after the IPO to replace roughly $20 billion in bridge loans due in September 2027.

The Bear Case Grows Louder

Not everyone is buying the hype. Senator Elizabeth Warren this week sent a 12-page letter to SEC Chair Paul Atkins demanding a delay of the IPO, alleging opaque accounting related to the xAI acquisition and an extraordinary concentration of voting power in Elon Musk’s hands — the CEO controls 80% to 85% of the voting rights. Short-seller Jim Chanos also took aim at the company during an investor conference in New York, calling the valuation fundamentally unjustified given the $5 billion loss.

Morningstar struck a similarly cautious tone, assigning a fair-value estimate of $63 per share — less than half the IPO price. The research firm argued that the current price embeds “a significant speculative premium” for Starship Mars missions and an AI unit that has yet to prove its profitability.

Index Hurdles and Leveraged Plays

Inclusion in major indices is not imminent. SpaceX could qualify for the Nasdaq-100 through a fast-track process after 15 trading days, but the S&P 500 requires four consecutive quarters of GAAP profit — a milestone analysts do not expect before late 2027 or 2028.

SpaceX at a turning point? This analysis reveals what investors need to know now.

Meanwhile, leveraged products are already in the pipeline. Defiance ETFs plans to launch a 2x long ETF under the ticker SPCU as early as June 15. In the UK, two leveraged products branded “ELON” and “MUSK” are slated to begin trading on the first day of the listing.

Whether the derivatives’ implied pop materializes — and whether the stock can sustain its altitude — will depend on the quarterly reports ahead, most notably how quickly xAI can pivot from cash incinerator to profit center.

Ad

SpaceX Stock: New Analysis – 11 June

Fresh SpaceX information released. What’s the impact for investors? Our latest independent report examines recent figures and market trends.