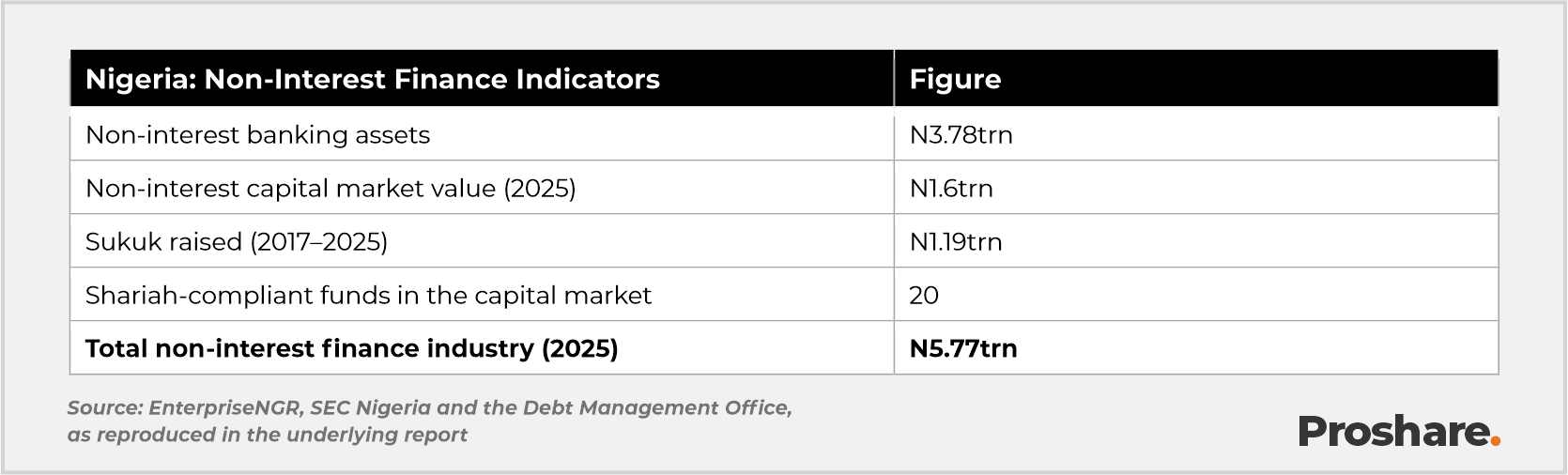

Nigeria’s non-interest finance industry closed 2025 at N5.77trn, according to EnterpriseNGR. Fifteen years after Jaiz Bank received the country’s first full non-interest banking licence, the industry comprises four banks, five takaful operators and twenty Shariah-compliant funds.

The headline figure, however, reflects a high degree of concentration. Non-interest banking assets stood at N3.78trn, representing 65.5% of total industry assets, while sovereign sukuk accounted for N1.19trn, or about 74%, of the N1.6trn non-interest capital market. Only three of Nigeria’s thirty-six states have issued sukuk since 2013, and takaful, despite its stated growth potential, still lacks a published baseline for gross written premium and market penetration.

The next phase of growth will depend on the expansion of investible instruments beyond Federal Government securities. EnterpriseNGR describes the corporate sukuk market as largely untapped, leaving non-interest banks with a narrow pool of Shariah-compliant assets for liquidity management, portfolio diversification and long-term investment.

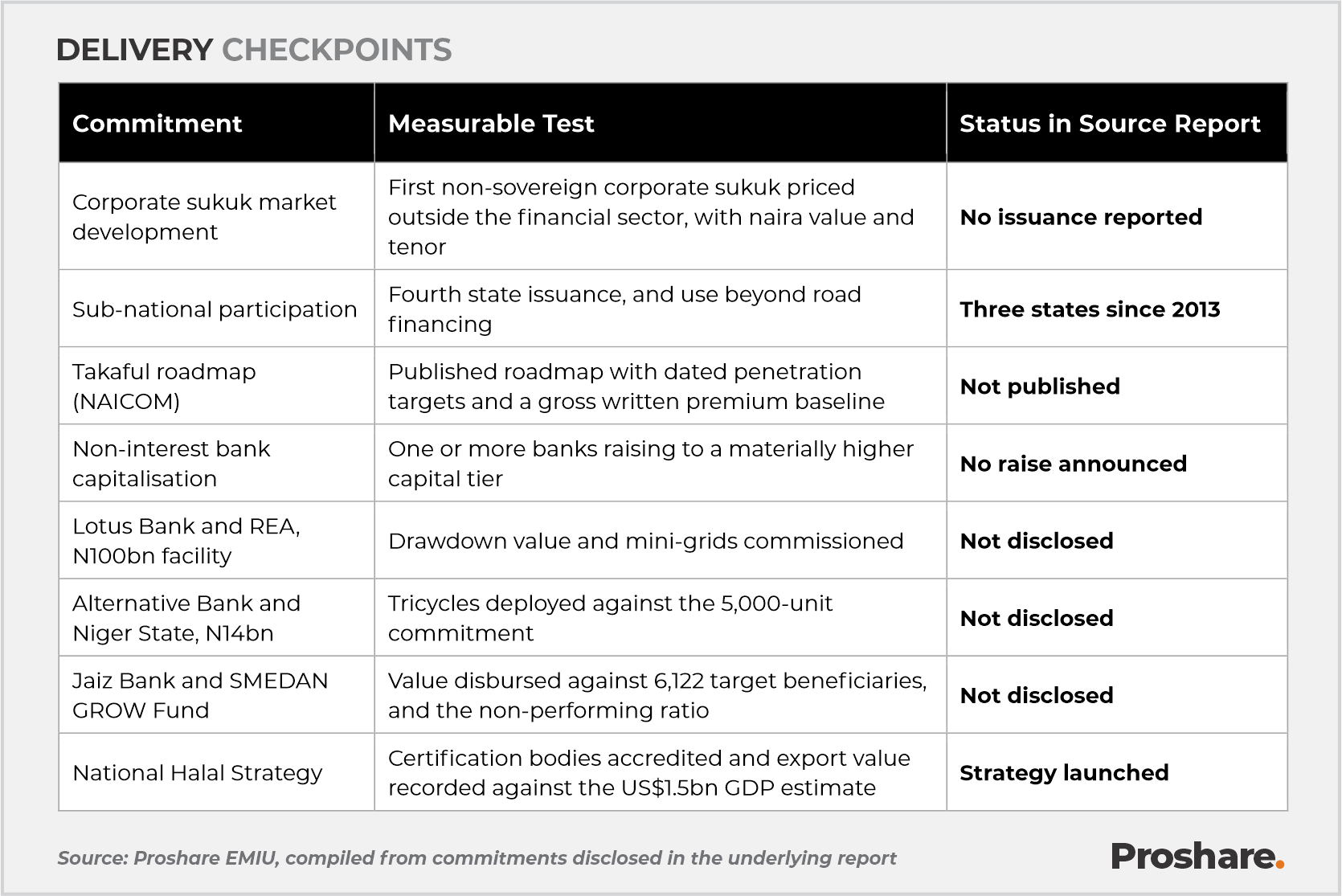

Four developments would provide clearer evidence of increasing market depth. These include the issuance of a corporate sukuk by a company outside the financial services sector, a fourth state sukuk extending beyond road financing, a NAICOM takaful roadmap with dated premium and penetration targets, and transparent reporting on the drawdown and deployment of the N100bn Lotus Bank facility with the Rural Electrification Agency and the N14bn Alternative Bank agreement with Niger State.

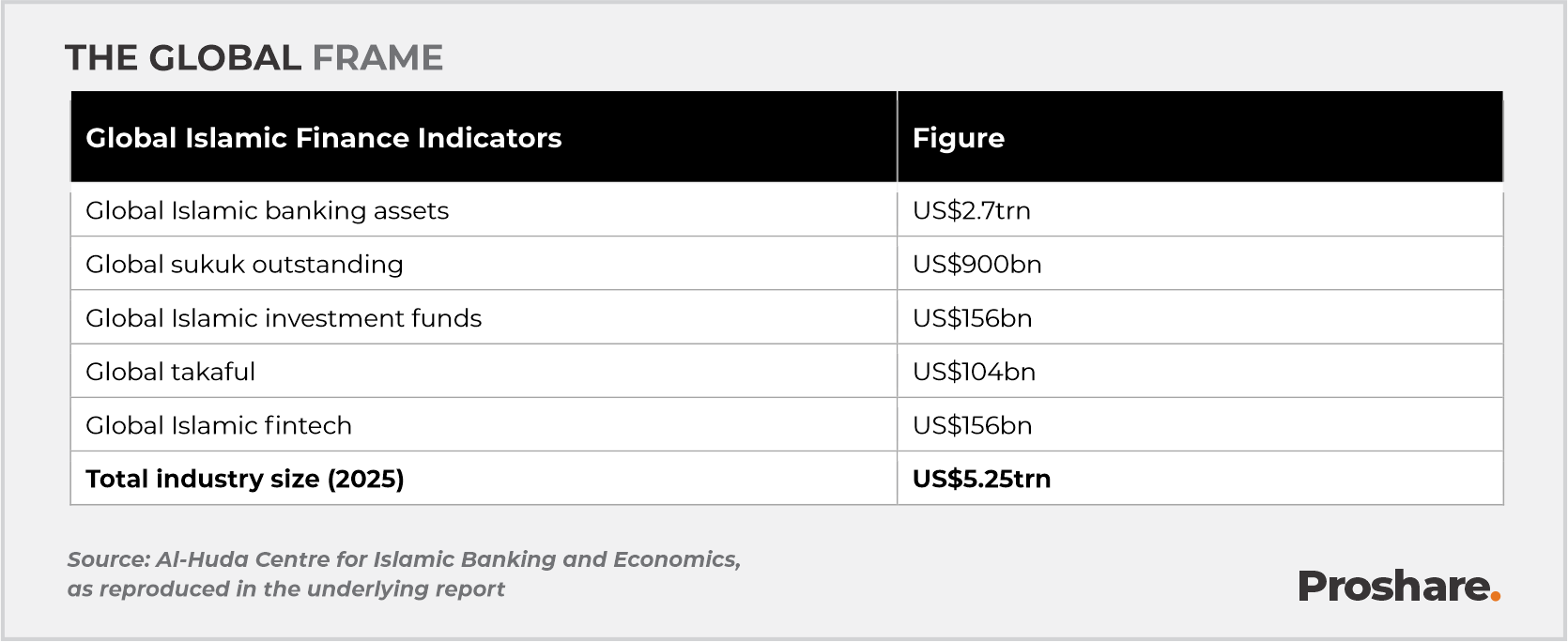

Nigeria’s non-interest finance industry operates within a global Islamic banking market estimated by the Al-Huda Centre at US$2.7trn, with Malaysia, Saudi Arabia, the United Arab Emirates, Qatar, Indonesia and Turkey providing the principal reference markets.

The sector has established a credible institutional base. Its transition from growth in headline assets to a deeper and more diversified market will depend on broader corporate issuance, increased state participation, stronger takaful data and clearer evidence that announced financing arrangements are being deployed into productive activity.

Two aggregate figures in the source data do not reconcile and have been identified at the relevant points in the report.

The Numbers on the Table

Nigeria’s non-interest finance industry closed 2025 with total assets of N5.77trn, on figures compiled by EnterpriseNGR. Non-interest banking accounts for N3.78trn of that total, or 65.5%. The non-interest capital market is valued at N1.6trn on Securities and Exchange Commission (SEC) figures. Twenty Shariah-compliant funds are listed in the capital market.

We note that banking assets of N3.78trn and the capital market value of N1.6trn total N5.38trn. The stated industry total is N5.77trn. The N390bn difference, equal to 6.8% of the reported total, is not attributed to the source data. Takaful and asset management balances would be the likely components. The source does not confirm this. The figures are carried out here as unreconciled, pending a segment-by-segment disclosure.

The Global Frame

Standard & Poor’s assesses the global Islamic finance industry as one of the fastest-growing segments of the international financial system. It projects asset growth of 5% to 10% in 2026, following expansion above 10% in 2025. The moderation is attributed to slower activity across several Gulf Cooperation Council economies, geopolitical tension in the Middle East and higher financing costs. Malaysia, Saudi Arabia, the United Arab Emirates, Qatar, Indonesia and Turkey remain the reference hubs.

What Has Been Built Since 2011

The Central Bank of Nigeria (CBN) issued the country’s first full non-interest banking licence to Jaiz Bank in 2011. The industry now comprises four non-interest banks: Jaiz, Taj, Lotus and Alternative. The source report states that each met the CBN’s 2024 to 2026 recapitalisation thresholds for its licence category. Five takaful operators are in the market: Noor Takaful, Jaiz Takaful, Hilal Takaful, Crown Takaful and Salam Takaful. Asset management is represented by Lotus Capital, Arthur Group and Marble Capital. The fintech layer includes Darrah, Zakahtech, Stecs, HalalVest, eTijar and ZamZam.

Regulatory oversight sits across the CBN, the SEC, the National Insurance Commission (NAICOM), the National Pension Commission and the Financial Reporting Council of Nigeria. Shariah governance runs through the Financial Regulation Advisory Council of Experts (FRACE) at the CBN and Advisory Committees of Experts at institution level.

Sovereign sukuk is the anchor instrument. The Debt Management Office has raised N1.19trn across multiple issuances to fund road and bridge construction across the six geopolitical zones. That single instrument accounts for 74% of the N1.6trn non-interest capital market. The source report cites oversubscription above 700%. It does not break that figure down by issuance or by retail and institutional split, and the figure is carried here as unverified.

Where the Money Has Been Deployed

Infrastructure

The N1.19trn sovereign sukuk programme has financed roads, bridges and expressways across all six geopolitical zones. The source describes the kilometres delivered as thousands. It does not itemise them by project or by completion status.

Renewable energy

Lotus Bank has entered a N100bn financing facility with the Rural Electrification Agency. The facility extends credit to certified developers building mini-grids and off-grid capacity in underserved communities. Drawdown to date is not disclosed.

Credit to MSMEs

Jaiz Bank has partnered with the Small and Medium Enterprises Development Agency of Nigeria (SMEDAN) through the GROW Fund scheme. The scheme targets 6,122 entrepreneurs. Value disbursed and default experience are not disclosed.

Climate action and e-mobility

Alternative Bank’s Mata Zalla project supplies women’s cooperatives with fleets of electric tricycles and battery-swapping infrastructure. The bank has signed a N14bn agreement with the Niger State government to finance 5,000 electric tricycles. Units deployed against that commitment are not stated.

Instrument Supply Beyond the Sovereign

EnterpriseNGR describes Nigeria’s corporate sukuk market as largely untapped, with issuance concentrated almost entirely in sovereign entities. This leaves non-interest banks with a narrow pool of Shariah-compliant instruments for liquidity management and long-tenor investment. Private issuers continue to raise capital through conventional debt markets.

The report sets out three remedies. Regulators would widen the range of eligible corporate issuers. The SEC would streamline its sukuk approval process. Tax and stamp duty treatment of sukuk would be harmonised with that of conventional bonds. According to the report’s assessment, a deeper corporate sukuk market would broaden the investment options available to non-interest banks, open ethical financing channels for infrastructure and corporate expansion, and support Nigeria’s standing as a hub for Islamic capital markets in West Africa.

Sub-national participation remains thin. Osun, Kogi and Lagos are the only states to have accessed the market since 2013. That is three of thirty-six states, or 8.3%. The source report puts the figure at about 10%, and the difference is noted here without resolution. The report identifies healthcare, housing, renewable energy and climate-resilient infrastructure as use cases beyond road financing.

Takaful is the least developed segment of the ecosystem, with minimal market share. EnterpriseNGR attributes this to limited operator scale, low consumer awareness and weak distribution networks. The report recommends that NAICOM lead a structured takaful roadmap carrying clear penetration targets and industry-backed awareness campaigns, supported by investment in digital distribution. Gross written premium and penetration rate are not provided in the source report, leaving the segment’s stated turning point unquantified.

Identity, Penetration and Product Range

The report identifies naming and public perception as a commercial constraint. In a multi-religious market, the label “Islamic finance” complicates the communication of an ethical, asset-backed, and risk-sharing proposition. This has driven the industry’s preference for the term non-interest finance. The report notes that Nigerians of the Christian faith hold senior operating roles across non-interest banks, takaful companies and investment firms. It cites Abayomi Alawode, a Nigerian and practising Christian, as Head of Islamic Finance at the World Bank. Whatever that was for remains unclear.

Penetration is described as low. The report characterises awareness and publicity efforts as insufficiently dynamic. It provides no penetration percentage or customer-account figure, so the gap is stated without measurement. The product range is described as thin, with few tailored ethical instruments beyond the core deposit and sukuk offerings. The report also calls for strategic roadshows across regions with sizeable ethically minded populations, and points to media platforms including WebTV’s Nigerian Islamic Finance Weekly programme and IFIING Media as channels for industry visibility.

The Stated Path to Scale

Speaking at the 7th Africa International Conference on Islamic Finance, the Emir of Kano, HH Muhammadu Sanusi II, tied the industry’s future to serving the bottom of the pyramid and to protecting rural households and businesses, particularly in northern Nigeria. He called for rural MSME targeting, for one or two non-interest banks to pursue substantially larger capitalisation, and for the removal of cultural barriers constraining women-owned businesses. The source document renders the name as Mohammed Sanusi II. It is corrected here to house style.

Dr Basheer Oshodi, President of the Non-Interest Financial Institutions Association of Nigeria (NIFIAN), points to deepening institutional capacity, improving engagement with regulators, expanding value to industry professionals and supporting responsible investing. He adds that stronger policy advocacy and collaboration across the financial services industry would support the sector’s growth. The report assigns NIFIAN a central role in capacity building and in developing the talent pipeline with universities offering Islamic finance courses.

On the halal economy, Nigeria’s National Halal Strategy was launched by Vice President Kashim Shettima. The Federal Government values the global halal market at US$7.7trn and estimates that the strategy will add US$1.5bn to Nigeria’s GDP by 2027. That GDP estimate is government-sourced and carries no published methodology in the material reviewed.

The report also points to the National Financial Inclusion Strategy, driven by the CBN, as a route for the industry to reach unbanked Nigerians, and calls for increased funding of Islamic fintech startups working in wealth management, credit, savings, payments and investments.

Delivery Checkpoints

The following checkpoints enable tracking of the stated scale ambition over the next four to six quarters. Status entries record what the source report discloses.

Concluding Thoughts

Nigeria has assembled the institutional structure of a non-interest finance industry over fifteen years. Four licensed banks have cleared their recapitalisation thresholds. A sovereign sukuk programme is running at N1.19trn. Shariah governance operates through FRACE and institutional advisory committees. A fintech perimeter is in place.

The concentration in that structure is visible in the numbers. 74 per cent of the non-interest capital market is held in sovereign paper. Three of thirty-six states have issued in thirteen years. Takaful operates without a published penetration baseline. The next phase of growth turns on corporate and sub-national issuance volume and the quality of the accompanying disclosure. Segment balances that reconcile, published penetration data, and drawdown reporting for announced facilities would allow the industry’s scale to be assessed by performance.

It is important to note that this report is a Proshare rendering of a source document titled Islamic Finance in Nigeria: Evolution, Impact, Gaps and Opportunities for Scale, dated 11 July 2026. All figures are attributed to the parties named in that document: Standard & Poor’s, the Al-Huda Centre for Islamic Banking and Economics, EnterpriseNGR, the Securities and Exchange Commission and the Debt Management Office. Proshare has not independently verified them.

DISCLAIMER

Proshare (EMIU) publishes this report for general information only. It is not investment, legal, tax or professional advice, takes no account of reader needs, and is not an offer or recommendation on any security. Institutions named are described, not endorsed or rated. Figures come from third-party sources named in the Editorial and Data Note, reproduced as published, unverified. Proshare gives no warranty. Items flagged, unreconciled or unverified should be treated as such; forward-looking statements may change without notice. Readers should do their own due diligence and take independent advice. To the fullest extent permitted by law, Proshare, its directors, officers, employees, agents and contributors, accept no liability for loss arising from reliance on this report. Proshare is not a licensed adviser, broker, fund manager or rating agency. Proshare and connected persons may hold positions in the named entities. Quoted views are the speakers. Errors are corrected on notification. See our Terms of Use. For more information, visit www.proshare.co or contact [email protected] and [email protected]

Proshare Nigeria Limited is an independent capital market intelligence and financial research platform.

Click on the links here for updates on Economy | Fiscal Policy, Nigeria Economy, Business | Frauds & Scandals, Oil & Gas, People, Products & Services, Market | Stock Picks, Opinions and Analysis, Finance | Personal Tax, Taxes & Tariffs, Personal Tax, Bonds & Fixed Income, Global Markets, Mergers & Acquisitions, Regulators | Regulators, Pensions n Retirement, Trade Investment, Reviews & Outlooks, Global Markets, and World Bank IMF and Dev Agencies.

Subscribe to be the first to receive our market intelligence newsletter and premium notes. Thank you.