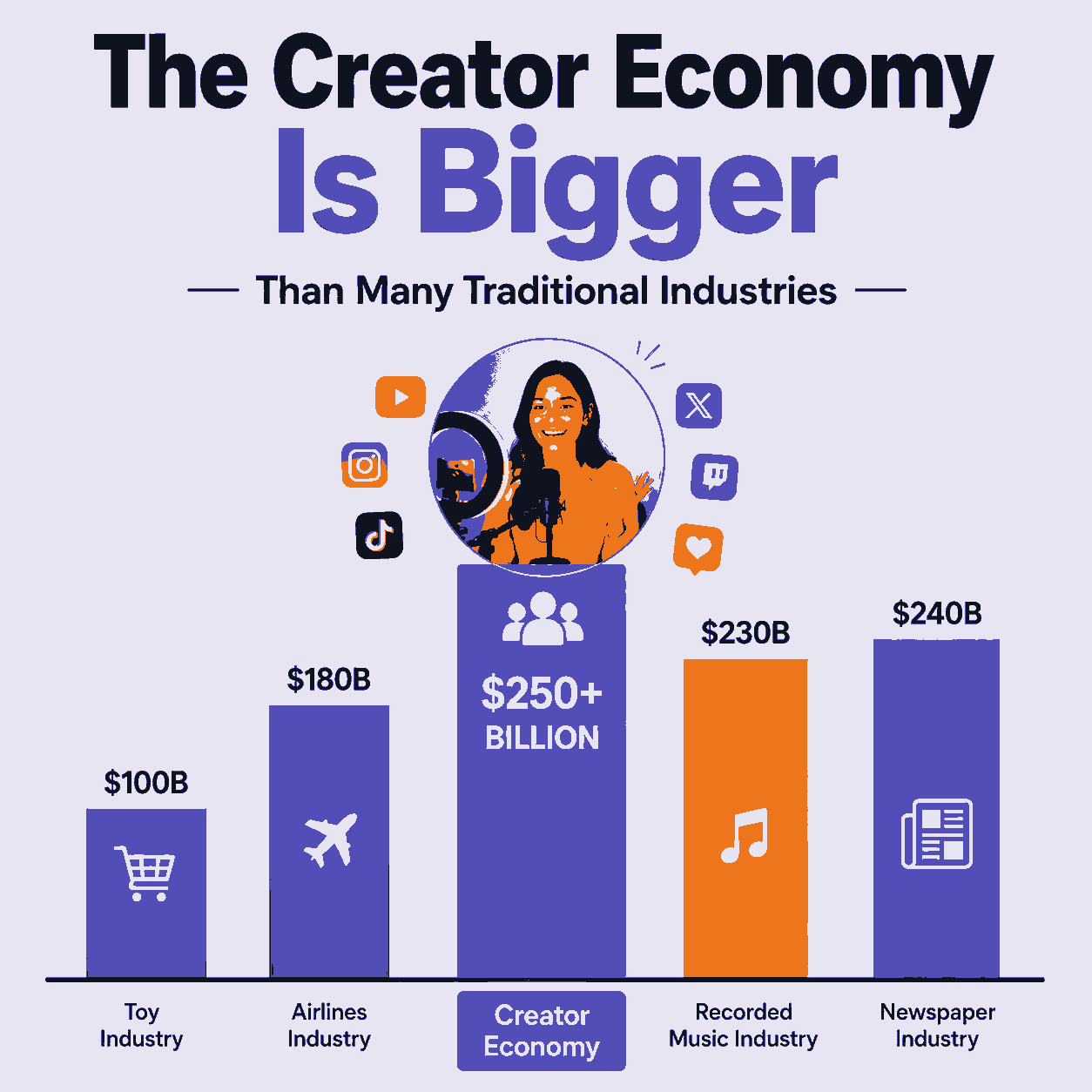

YouTube’s annual accounting of its economic footprint reached a new milestone this week: the platform’s creative ecosystem contributed more than $60 billion to US gross domestic product in 2025 and supported the equivalent of 540,000 full-time jobs, according to a commissioned study from Oxford Economics released July 16. That marks a 71% increase in measured GDP contribution since 2022, when the same research firm put the figure at $35 billion and roughly 390,000 jobs, according to the 2022 US Impact Report published via BusinessWire.

The numbers are real and the growth trajectory is striking. What the headline figure cannot show — by the design of the model that produced it — is whether a typical creator building a YouTube channel in 2026 can expect to earn a living wage from it. According to the most recent independent analysis of creator compensation, more than half of all creators earn under $15,000 annually, and the majority of full-time creators fall below the US living wage, per the 2025 Creator Earnings Report from Influencer Marketing Hub and NeoReach.

The platform’s GDP report and the independent earnings data tell different stories about the same ecosystem — and understanding why those stories diverge requires looking at how the $60 billion figure was built.

What the $60B Number Actually Measures

Oxford Economics produced the 2025 US Impact Report using the IMPLAN input-output model — the most widely used tool for regional economic impact analysis in the United States, based on the Nobel Prize-winning framework developed by economist Wassily Leontief in the 1940s. The Oxford Economics methodology page explains how IMPLAN works by mapping buy-sell relationships between industries: when a creator hires a video editor, rents studio space, or buys camera equipment, those transactions ripple through the broader economy as suppliers purchase their own inputs, and workers spend their paychecks locally. IMPLAN captures all three layers — direct, indirect, and induced — and sums them into a total economic footprint.

The methodology paper Oxford Economics published alongside the report is unusually transparent about one critical limitation: the results are presented on a “gross basis.” That phrase has a specific technical meaning that matters enormously for how readers should interpret the $60 billion headline. A gross-basis figure counts all the economic activity that YouTube creators generate without subtracting what those same people, hours, and resources might have produced in alternative work. A full-time creator who left a salaried position to build a YouTube channel appears in the IMPLAN model as an economic contribution of the full value she now generates through the platform — the foregone salary at her prior job does not reduce that figure. Oxford Economics explicitly states this, and it is not unique to this study; it is a standard feature of all IMPLAN-based economic impact analysis.

What the gross-basis approach means practically: the $60 billion figure is an accurate measure of how much economic activity flows through the YouTube creator ecosystem. It is not an answer to the harder question of whether YouTube creates more economic value than the same people and capital would generate elsewhere.

Oxford Economics surveyed more than 6,100 US creators and 5,700 US users between January and March 2026, with an additional 600 business respondents. The creator survey was distributed through YouTube to its own creator community — a standard approach that Oxford Economics then weighted by channel size, but one that cannot fully correct for the possibility that dissatisfied or low-earning creators are less engaged with YouTube’s outreach than successful ones.

Year-Over-Year Growth and Three-Year Trajectory

The growth in the measured figures has been consistent and substantial. YouTube’s 2024 US Impact Report, also produced by Oxford Economics, put the platform’s contribution at $55 billion and 490,000 full-time equivalent jobs. The 2022 report put those figures at $35 billion and approximately 390,000 jobs. Across three years, the measured GDP contribution grew by more than 70 percent.

The $100 billion cumulative payout figure YouTube highlighted alongside the US report is a rolling global total covering creators, artists, and media companies from 2021 through 2025, per the official YouTube Blog announcement. The same figure appeared in YouTube’s European impact report in October 2025, where Oxford Economics found the platform’s ecosystem contributed over €7 billion to EU GDP in 2024, per the European impact report. YouTube appears to be deploying this cumulative total across multiple regional reports as its most prominent evidence of commitment to creator livelihoods.

How YouTube’s Revenue Model Creates a Structural Monetization Advantage

Central to the report’s economic claims is YouTube’s revenue-sharing architecture, which differs structurally from most of its competitors. Through the YouTube Partner Program, creators whose channels meet the eligibility threshold — currently 1,000 subscribers and 4,000 hours of watch time — earn 55% of the advertising revenue generated alongside their long-form videos, as detailed in YouTube’s partner earnings documentation. YouTube retains the remaining 45%, which it says it reinvests in platform infrastructure.

For YouTube Shorts, the split is inverted: YouTube retains 55% of the revenue pool and distributes 45% among eligible creators based on their proportional share of total Shorts views, according to the YouTube Partner Program explainer published February 2025. That structural difference between long-form and short-form monetization is significant. Creators building audiences primarily through Shorts face a meaningfully lower revenue ceiling than those building watch-time on traditional long-form uploads.

Compared to rival short-form platforms, YouTube’s long-form split is the industry-leading rate at scale. TikTok’s effective revenue share for creators is estimated at 10-20%, while Twitch pays most streamers approximately 50%. The non-negotiable, universal nature of the YouTube split — it is the same for a creator with 1,001 subscribers and one with 100 million — means MrBeast and an emerging educational channel receive identical percentage terms from the platform.

Geographic Spread Versus Income Concentration

YouTube emphasizes that creator activity is no longer concentrated in coastal media markets. The 2025 report found that all 50 US states now contain at least 10 channels with more than 1 million monthly views — a figure the platform uses to argue that the creator economy has become a genuinely national phenomenon, as stated in the official YouTube Blog announcement. The blog post accompanying the report was written by Alexandra Veitch, YouTube’s Head of Government Affairs and Public Policy for the Americas — a choice of author that makes the intended audience visible: the geographic argument is a policy argument, directed at regulators and legislators who might otherwise frame YouTube as a product of coastal tech culture.

That geographic spread does not reflect income spread. According to CreatorIQ’s State of Creator Compensation report published in January 2026, the top 10% of creators captured 62% of all ad payments in 2025 — up from 53% in 2023. The top 1% alone captured 21% of total payment volume, up from 15% in 2023. Average creator earnings per campaign rose to $11,400, but the median creator earned $3,000 per campaign — a divergence that reflects a power-law distribution, not a bell curve, per the same CreatorIQ research.

This income concentration is not a malfunction of the creator economy. It is theoretically predicted by what economists call superstar theory: in markets where talent differences are amplified by broadcast technology, small differences in popularity translate into enormous differences in income. The algorithmic recommendation systems that distribute viewer attention on YouTube function as exactly this kind of amplifier.

Who the 540,000 Jobs Figure Actually Includes

Oxford Economics’ methodology paper defines the creators included in the economic model as “creative entrepreneurs” — individuals or businesses with at least 10,000 subscribers, or smaller creators who either earn money directly from YouTube, earn money through their YouTube presence from other sources (brand deals, merchandise, live events), or permanently employ others to support their channel. Creators who spend less than eight hours per week on YouTube are excluded from the full-time equivalent calculation.

That threshold matters for interpreting the 540,000 figure. The model does not count every person who uploads a video. It counts the equivalent of full-time economic effort directed at YouTube activity across all qualifying creators and the businesses in their supply chains — editors, camera operators, studio managers, equipment suppliers, and the workers those suppliers employ. A full-time equivalent can represent one creator working 40 hours per week or four creators each working 10 hours. The 540,000 figure is a sum of those equivalents, not a headcount of distinct individuals.

The model also explicitly excludes the economic contribution of YouTube’s own corporate operations and the revenue gains that businesses receive from advertising on the platform. Those exclusions are reasonable for a study measuring the creator ecosystem specifically — but they mean the total economic footprint of YouTube as a platform is substantially larger than the $60 billion figure represents.

Surveys, Sample Sizes, and the Confidence Question

For a study of this scope, Oxford Economics fielded a substantial data collection effort. The US creator survey reached 6,100 respondents; the user survey reached 5,700; the business survey reached 600, as documented in the Oxford Economics methodology paper. These sample sizes are comparable to large academic surveys and generally sufficient for estimating population-level patterns.

The survey of teachers — 94% of whom reported incorporating YouTube content into lessons — and parents — 78% of whom said the platform provides quality content for their children’s learning or entertainment — relies on the user survey’s representative sampling methodology. Oxford Economics weighted user responses to reflect the characteristics of YouTube’s user base by age and gender, rather than the general US population.

The 77% of creators who said their media and entertainment career started on YouTube is drawn from the creator survey, which was distributed by YouTube to its own creator community. This is the portion of the methodology most exposed to non-response bias: a creator who feels YouTube has not supported their career is less likely to be engaged with the company’s survey outreach. Oxford Economics discloses this channel but does not quantify the potential effect on the figure.

What Good Creator Earnings Actually Look Like

The report’s most prominent individual data point — $100 billion paid to creators globally since 2021 — sits alongside an independent picture of creator earnings that is considerably less uniform. Among all creators across platforms, more than half earn under $15,000 annually and the majority of full-time creators earn below the US living wage, according to the 2025 Creator Earnings Report from Influencer Marketing Hub and NeoReach. Among creators who treat content as a full-time professional business, the 2025 median reached $133,000 — but this group represents a small fraction of the overall creator population.

The gap between average and median earnings in the creator economy is not a statistical artifact. It is a signal of a K-shaped distribution: a thin tier of high-earning professional creators, and a broad base of part-time or hobbyist creators whose YouTube income does not approach a livable wage. The IMPLAN model’s FTE figures include both groups when their weekly time commitment crosses the eight-hour threshold — meaning the 540,000 jobs figure reflects economic effort from across the entire distribution, not just the professional tier.

For a creator deciding whether to build a YouTube channel in 2026, the most honest summary of the data is this: YouTube’s economic ecosystem is genuinely large and growing. The platform’s 55% long-form revenue share is the most favorable offered by any major distribution platform at scale. Geographic barriers to participation have genuinely declined. And at the same time, the majority of people inside this ecosystem earn substantially less than a living wage from YouTube alone, income concentration among the top tier has been accelerating, and median earnings per campaign have fallen even as total payments to creators have risen.

Frequently Asked Questions

How did Oxford Economics calculate YouTube’s $60 billion GDP contribution?

Oxford Economics used the IMPLAN input-output model — the standard tool for US regional economic impact analysis, based on Wassily Leontief’s Nobel Prize-winning framework. The model estimates direct economic activity (creator revenue), indirect activity (purchases from suppliers and vendors), and induced activity (spending by creators and their employees in local economies). Critically, the results are on a gross basis: they measure total economic activity flowing through the YouTube creator ecosystem without subtracting what those same resources might produce in alternative uses. The total payout from YouTube for 2025 was provided by YouTube itself; Oxford Economics then applied the IMPLAN model to estimate supply-chain and worker-spending ripple effects, as described in the Oxford Economics methodology paper.

Do most creators actually earn a living from YouTube?

No. More than half of all creators earn under $15,000 annually across platforms, and the majority of full-time creators earn below the US living wage, according to the 2025 Creator Earnings Report from Influencer Marketing Hub and NeoReach. The median creator earned $3,000 per brand campaign in 2025, while the average was $11,400 — a divergence that signals severe income concentration at the top, per the CreatorIQ State of Creator Compensation report. The 540,000 full-time equivalent jobs in Oxford Economics’ model include creators who work eight or more hours per week on YouTube, spanning the full income spectrum from six-figure earners to those earning well under minimum wage from their content alone.

Why does the report use “full-time equivalent jobs” instead of reporting actual headcounts?

Full-time equivalent is a standard economic measurement that converts total hours worked into the number of full-time positions those hours represent. One FTE could be a single creator working 40 hours per week on YouTube, or four creators each contributing 10 hours. Oxford Economics uses FTE because the creator workforce is overwhelmingly part-time: many people who earn some income from YouTube do not work on it full-time. Reporting a headcount would require an arbitrary decision about which part-time creators to include, producing a number that is harder to compare across studies. FTE allows consistent comparison across years and markets, but it also means the 540,000 figure tells you about the total volume of economic effort, not the number of distinct people earning income from YouTube, as the Oxford Economics methodology paper explains.

Can YouTube’s commissioned economic reports be independently verified?

The methodology is publicly available and uses a standard, independently developed model (IMPLAN), which makes the internal consistency of the figures checkable by any economist with access to the same inputs. Oxford Economics is a credible global advisory firm with a track record in economic impact analysis for public and private clients. What cannot be independently verified is the total YouTube payout figure for 2025, which the Oxford Economics methodology paper states “was provided by YouTube” as an input to the model — meaning the study’s headline figure rests on a number that only YouTube itself has audited. Independent verification would require access to YouTube’s internal revenue data, which is not publicly disclosed. Readers should treat the $60 billion figure as a reasonable methodological estimate whose accuracy depends on the accuracy of YouTube’s own payout disclosure.