- June 21, 2026

- Olivia

- 0

That idea is not new. Many observers have long argued that New Zealand tends to move through the cycle ahead of Australia, sometimes by a year or two, because our economy is smaller, more interest-rate sensitive and more exposed to housing and confidence swings. In earlier periods, such as the years when John Key was Prime Minister, New Zealand often outperformed Australia, even if the comparison was not always straightforward.

Since Covid, however, the pattern has been less flattering for New Zealand, with weaker growth, a sharper housing correction and a more fragile consumer backdrop.

New Zealand now appears to be emerging from this slowdown first. Recent business and consumer confidence readings have started to improve from very depressed levels, even if they remain uneven month to month. Business surveys have shown firms becoming less pessimistic about the outlook, and consumer confidence has moved off the worst levels seen during the period of aggressive rate increases and recession-like conditions.

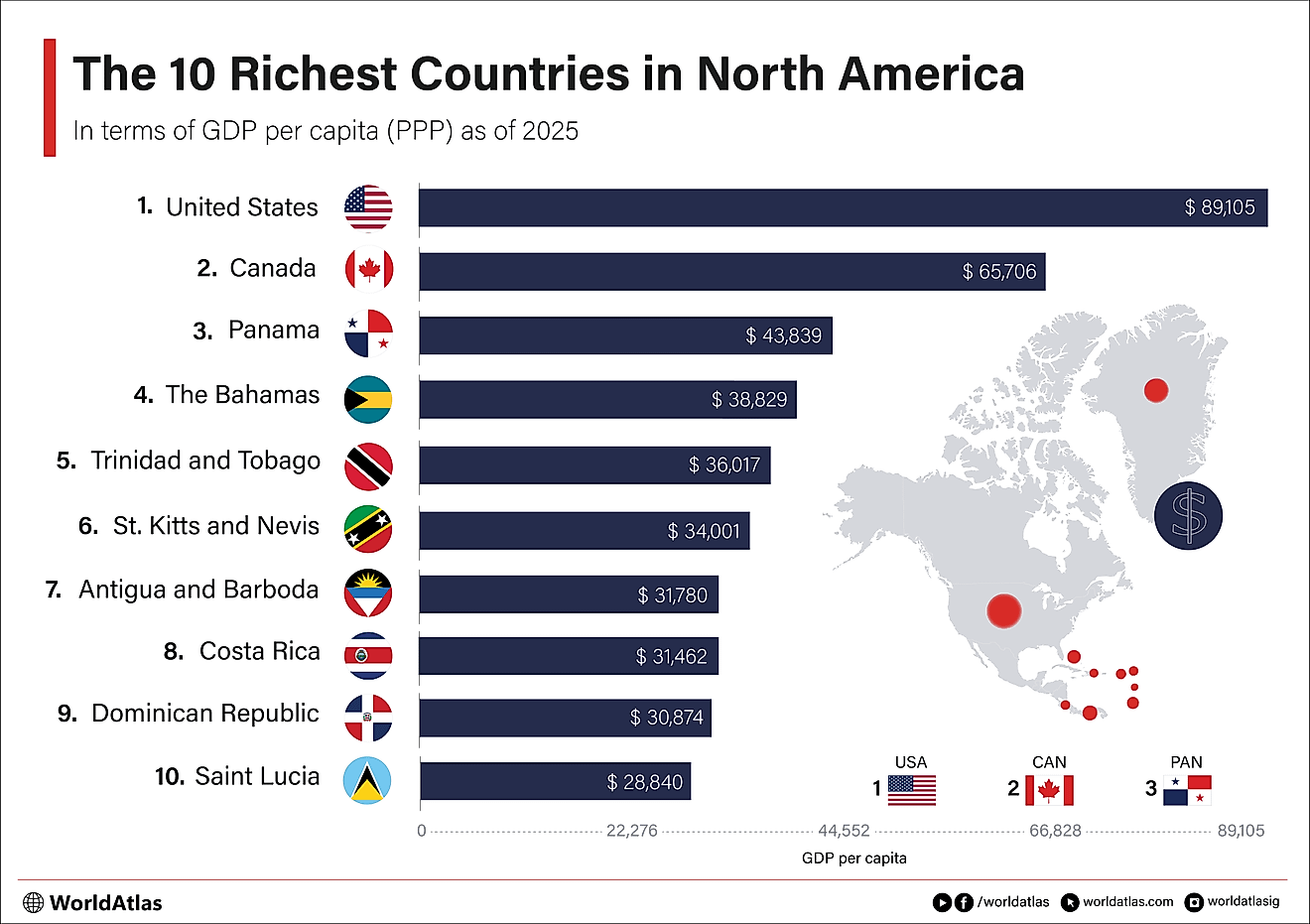

The ANZ Business Outlook for May 2026 highlighted that headline business confidence in New Zealand lifted from -10.6 in April (which means that more companies surveyed are pessimistic about the future than optimistic) to a reading of +10.0 in May. This is a meaningful improvement and was supported by a similar recovery in the Firm’s Own Activity outlook.

Our Consumer Confidence reading also improved. These are not yet boom-time readings, but they do matter because confidence usually turns before spending and hiring do. In Australia, business confidence levels remain firmly negative, and after the recent significant tax changes proposed in the Australian federal government budget, consumer sentiment is now sitting almost 20% below its historical average.

Inflation and interest rates are lower in NZ, with our CPI at 3.1% versus Australia at 4.2%, while some economists are suggesting Australian inflation may peak above 5% on the back of loose government expenditure and oil prices. Unusually, NZ currently has lower interest rates than Australia, with our OCR at 2.25% versus 4.35%, and one-year mortgages at about 4.7% versus 6.7% in Australia. The property market adds to the narrative.

In Australia, housing has come under pressure from policy uncertainty, including the proposed tax changes that have unsettled parts of the market. Even where prices have not fallen sharply, the tone has become more cautious, and many participants are waiting to see how the policy environment settles.

New Zealand’s market, by contrast, looks as if it has largely moved through its correction and into a more stable phase. Prices remain well below the peaks in many areas, but the worst of the adjustment appears to have passed, and that matters for both sentiment and spending.

Relative property value is therefore shifting in an interesting way. Australia remains the richer market in aggregate, with higher incomes, deeper pools of capital and a larger and more liquid housing sector.

But New Zealand now offers better relative value on a cycle basis, particularly for buyers who believe that the next few years will be about recovery rather than correction. The numbers in support of this proposition are clear; from 2019 to 2026, the house price to median household income in Sydney has grown from a multiple of 8.2 times to more than 12 times, whereas in Auckland we have fallen from 8.7 times to 7.5 times.

In simple terms, Australia has become increasingly expensive, while New Zealand has become cheaper, less crowded, and closer to the point where sentiment can improve.

Immigration is an important part of that story. New Zealand’s weak labour market and high living costs have made it harder to retain people, and the flow of migrants to Australia has been one of the recurring drags on domestic demand. When people leave, it affects consumption, housing demand and labour supply, which in turn shapes growth expectations.

At the same time, New Zealand has also relied on migration to support parts of its economy, especially during periods when local labour shortages were more acute. The challenge is that immigration can boost growth in the short term, but if wages, housing and job opportunities do not keep up, it can also create pressure and dissatisfaction.

Australia’s immigration picture is different. A larger labour market and stronger population inflows have supported demand, housing construction, and the service economy, but they have also added to congestion and policy pressure. In political terms, this has become increasingly sensitive. Strong polling by One Nation, who have incredibly moved ahead of Labour as the preferred party and now have Pauline Hanson as the preferred Prime Minister, reflects a broader frustration among voters who feel that major parties have not adequately addressed cost-of-living pressures, migration settings, and housing affordability.

That political disruption matters economically because businesses dislike uncertainty, and when policy debate becomes more fragmented, investment decisions can slow. NZ now has a path back to fiscal surpluses, whereas Australia, under a high-spending Labour government, is forecasting deficits in perpetuity, despite the revenues earned from their resources sector.

New Zealand’s first-quarter GDP result points to a firmer start to the year, with the economy expanding by 0.8%. Growth was supported by stronger activity in manufacturing, agriculture and wholesale trade, although pockets of weakness remain in areas such as construction, media, and public services.

The effects of the Iran conflict are more likely to be felt in the second quarter, as higher fuel prices squeeze household disposable income and business margins. Even so, from next year New Zealand is expected to grow faster than Australia, albeit from a lower base.

That is why the current comparison should not be reduced to a simple “which economy is better?” question. Australia is still stronger today in absolute terms, especially on employment and household wealth. New Zealand, however, may now be better placed for the next phase of the cycle because its worst headwinds have already passed and its momentum is improving from a lower base.

That is often how recoveries begin: not with dramatic strength, but with the first signs that conditions are no longer getting worse.

The bigger picture is that New Zealand and Australia remain linked, but they do not always move in lockstep. When one is still absorbing the pain of a tightening cycle and the other is already beginning to recover, the difference can become visible in confidence, housing, corporate commentary and employment.

Right now, the evidence suggests New Zealand is beginning to edge ahead in terms of direction, even if Australia still looks stronger on the scorecard today.

Catch up on the debates that dominated the week by signing up to our Opinion newsletter – a weekly round-up of our best commentary.