Breaking the old macro playbook

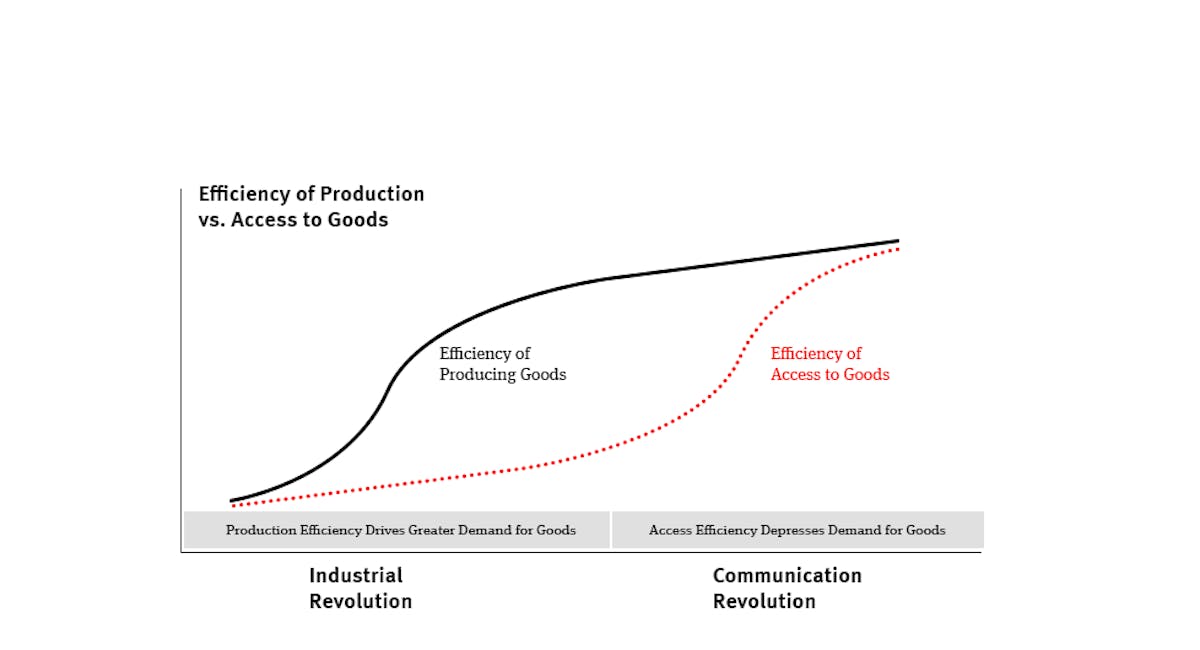

Wall Street still trades the global economy using a dashboard built for the industrial age. Every month, currency markets obsess over payrolls, wage growth, inflation prints, retail sales, and GDP revisions as though human labour remains the sole engine driving economic expansion. Traders still treat Non-Farm Payrolls like the heartbeat monitor of capitalism itself because for decades the equation was relatively straightforward: more workers produced more output, stronger consumption, faster growth, tighter labour markets, and ultimately higher interest rates. But the AI boom is beginning to challenge the very plumbing beneath that framework, and markets may soon need an entirely new macro operating system to understand what growth, productivity, inflation, and even employment actually mean in the age of machine intelligence.

The problem is that traditional economic indicators were designed for a world where labour scarcity constrained production capacity. AI potentially changes that relationship entirely. If businesses can generate rising output with fewer workers, stronger margins with flatter payrolls, and accelerating productivity without broad wage inflation, then many of the macro relationships traders have relied on since the postwar era begin to weaken simultaneously. A country could theoretically produce stronger GDP growth, rising corporate earnings, and appreciating financial assets even while payroll growth slows materially or labour participation deteriorates beneath the surface. That would have sounded almost impossible under the old industrial macro model. Yet it increasingly resembles the economic architecture markets may be drifting toward.

What makes this transition particularly dangerous for investors is that financial markets are still largely pricing AI through the narrow lens of earnings upgrades, semiconductor demand, hyperscaler capex, and valuation expansion. The market continues to treat AI like a gigantic digital gold rush, where every chipmaker, data center operator, networking firm, and cloud provider becomes another shovel manufacturer feeding an endless-frontier boom. But beneath the market euphoria, the far more important question is whether AI is actually becoming economically embedded deeply enough to alter national productivity curves, labour structures, inflation dynamics, and capital flows themselves.

That distinction is precisely why the Federal Reserve’s recent work on AI adoption matters far beyond technology research. The Fed is quietly beginning to study the economy through an entirely different lens, attempting to measure not simply AI enthusiasm but actual diffusion throughout the real economy. Its research shows that only about 18% of firms had adopted AI by late 2025, even after adoption accelerated sharply, while worker surveys show much higher rates of experimentation and enterprise exposure. The gap matters enormously because markets are increasingly pricing experimental exposure, casual usage, and genuine productivity transformation as though they are already interchangeable. They are not.

What the Fed’s data quietly reveal is that AI remains heavily concentrated in white-collar cognitive industries such as finance, consulting, software development, engineering, and professional services, rather than deeply penetrating the broader industrial economy. That helps explain why AI infrastructure assets continue to behave like momentum supercycles, while much of the broader economy still struggles to produce the explosive productivity surge that markets already assume is inevitable. Investors are effectively trading AI as though the future has fully arrived while policymakers appear far less convinced the real economy has even completed the onboarding process.

That is where the next evolution of macro analysis begins. Markets may increasingly need a parallel AI economic dashboard sitting beside the traditional macro framework. Instead of focusing exclusively on payrolls, CPI, GDP, and retail sales, investors may soon need to track AI infrastructure velocity, AI adoption diffusion, labour displacement intensity, productivity transmission, and even social stability risks emerging from automation itself.

The first layer would be an AI Infrastructure Velocity Index, effectively the industrial production gauge of the AI economy. This would track hyperscaler capex, GPU shipments, data center construction, power consumption, semiconductor utilization, networking demand, and AI-related credit issuance. Right now, this is the part of the cycle markets understand best because it feeds directly into earnings and visible revenue growth. But infrastructure alone does not guarantee productivity transformation, any more than fibre-optic overbuilding guaranteed sustainable profits during the telecom bubble.

The far more important variable may become what could be described as an AI Adoption Diffusion Index. This would function almost like a payroll report for the AI economy itself, measuring how deeply AI is integrating into actual enterprise workflows rather than merely existing as experimental software. Markets would need to monitor enterprise AI penetration, workflow integration, agentic deployment, AI-assisted coding intensity, and productivity usage rates across sectors and firm sizes. The Fed’s own work already hints at the importance of this distinction between casual experimentation and meaningful operational absorption.

JPMorgan’s recent analysis reaches a remarkably similar conclusion from a different angle. What the bank is quietly warning is that AI usage intensity among power users appears to be exploding while broad societal adoption remains surprisingly gradual relative to the narrative embedded into market valuations. That distinction could ultimately define the next phase of the AI trade. The original market assumption was that generative AI would rapidly become a mass-consumer-behaviour revolution, similar to smartphones or social media. Instead, the evidence increasingly suggests something more concentrated is emerging beneath the surface, where a relatively narrow class of enterprise developers, software engineers, researchers, and workflow-intensive users account for a disproportionate share of compute demand.

That dynamic creates both the bullish and uncomfortable side of the AI story simultaneously. The bullish interpretation is that AI may not require billions of daily users interacting with chatbots to justify the infrastructure supercycle. A smaller cohort of deeply embedded enterprise and industrial users consuming exponentially more compute may still sustain hyperscaler revenues and semiconductor demand for years. But the uncomfortable reality is that broader surveys still show surprisingly modest evidence that AI has yet to become a true mass behavioural transformation across the wider economy.

This is why markets may eventually need an entirely new category of labour indicators as well. Traditional macro models measure jobs created, wage growth, and labour participation. But in an AI economy, investors may increasingly need to measure jobs displaced, hours automated, productivity per remaining worker, wage compression by sector, and the elasticity of labour substitution with respect to AI deployment. The old Phillips Curve framework could gradually weaken if labour scarcity no longer constrains output generation in the same way. Economies may increasingly see rising productivity alongside softer employment dynamics, creating a world in which equity markets, GDP, and payrolls no longer move in lockstep.

The productivity transmission layer may ultimately become the most important variable of all. Markets currently assume AI productivity gains are inevitable, yet the Fed’s own research shows daily AI usage remains relatively limited despite widespread experimentation. JPMorgan’s work similarly shows that while compute consumption and token intensity are exploding among active users, overall productivity gains across the broader economy remain relatively modest compared with the apocalyptic and utopian narratives that dominate financial markets. Markets are effectively pricing AI as if electricity, railroads, and the internet were arriving simultaneously, while the real economy still looks more like a cautious software migration unfolding, workflow by workflow and department by department.

That divergence between narrative velocity and measurable economic absorption may ultimately become the defining macro tension of the next decade. If AI adoption accelerates rapidly enough, the productivity gains could help offset structural inflation pressures stemming from demographics, deglobalization, fiscal expansion, and energy transition costs. But if capital spending continues to scale at wartime-era industrial levels while adoption remains concentrated and uneven, markets may eventually confront the uncomfortable realization that parts of the AI boom were priced on future expectations rather than on confirmed economic gravity.

In many ways, this is no longer simply a technology story. It is the early construction phase of an entirely new macroeconomic architecture. Markets are gradually moving away from a purely labour-driven economic model toward a hybrid system built around labour, capital, compute infrastructure, energy capacity, and machine intelligence itself. Future currency markets may increasingly trade national productivity differentials, AI absorption rates, compute sovereignty, and workforce adaptability rather than relying exclusively on payrolls and consumption cycles. The countries that integrate AI most effectively may attract the largest long-term capital flows regardless of demographic constraints, while those that fail to adapt risk slower productivity growth, rising fiscal stress, and weakening competitiveness.

The old economic dashboard is not disappearing overnight. Payrolls, inflation, and GDP will still matter enormously. But the AI boom is quietly introducing an entirely new layer of macro analysis beneath the surface, one where compute becomes a productive asset class, token consumption resembles industrial demand, and intelligence infrastructure itself increasingly behaves like economic capital. Right now, markets are still trading AI like the future has already arrived. The real challenge for investors over the next decade will be determining whether the economy can absorb that future fast enough to justify the extraordinary expectations already embedded into global asset prices.